|

Talking banks out of money

|

|

August 4, 1998: 3:30 p.m. ET

Obtaining a small business loan isn't hard, if you prepare before applying

|

NEW YORK (CNNfn) - When Internet entrepreneur Aliza Sherman first went to the bank for a business loan, everything was going well until they asked her about her personal credit.

At that point, Sherman, the president of Cybergrrl, said she thought it was all over. (99KB WAV or 99KB AIFF)

Despite their intimidating reputation, bankers want to make loans to new businesses. In fact, lending is increasing by double-digits annually.

But what does it actually take to get a loan?

1. A good personal credit history

John McWeeney, executive vice-president at Fleet Bank, says a good personal credit history reflects strongly on the future of your business.

"We view the entrepreneur and the business as one," he said. "When we look at the credit requests for a small business, we look at the finance of the owners of that business."

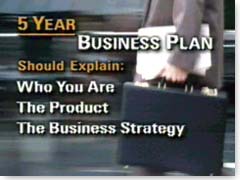

2. A detailed 5-year business plan

Your business plan should explain who you are, the product, the business strategy, marketing plan, competition, and financial projections.

Sandy Maltby, vice-chairman of Key Bank, says you shouldn't overlook the basics. "The three C's that should be included in their business plan should be character, their cash flow and their collateral," she said.

3. Know your needs

To improve cash flow you may only need a line of credit. For purchases of equipment or to expand inventory, a loan with a longer payment schedule may be better.

Make sure you've figured out ahead of time what it is you're going to need, and be prepared to explain yourself thoroughly to your loan officer.

4. Demonstrate knowledge of the business

This is very important. No bank will loan you money if don't appear educated about your own company. Use your knowledge to the fullest, and if you don't know everything you think you should, ask someone else.

For example, dress designer Naim Marizaeh needed a loan to move to a new location. He used his ace in the hole when talking to the bank. "I used the experiences of my mother," he said. "She knows everything about the business."

5. Share the risk

The bank will want you to share the risk. That means you should raise at least 20% of what you actually need before you walk into the bank.

Or, if you're like Internet entrepreneur Aliza Sherman, have a business like Cybergrrl up and running, and the bank will likely work with you.

--by staff writer Kim Kennedy

|

|

|

|

|

|

|