|

Budget: not a 4-letter word

|

|

July 6, 1999: 10:56 a.m. ET

Experts say spending plans are the best way to plan for the future

By Staff Writer Shelly K. Schwartz

|

NEW YORK (CNNfn) - You work hard. You pay your bills. And you're not especially interested in establishing a budget that crimps your style.

Sound familiar?

Experts say it's that laissez-faire attitude that can get you into trouble.

"Often times we want the easy way out," said Dee Lee, a certified financial planner in Harvard, Mass. and author of "Let's Talk Money." "We don't want to have to shop the specials or use coupons or cook pork chops this week rather than chicken because it's cheaper. We think because we are disciplined in our job we deserve [to spend freely]."

When you can't come up with the down payment on your dream house, however, and you can't afford to retire with your colleagues, you might begin looking at budgets a little differently.

"Nobody wants to be a scrooge, but at the same time if we are not, we are going to be far worse off," Lee said.

Four-letter words

Contrary to popular belief, financial pros say budgets aren't just for the frugally challenged. The financial planning tools, they say, can and should be used by everyone.

If you've never budgeted before, Lee said it's best to start out by tracking your spending patterns over the course of the next few months. After all, she said, you can't manage your money until you know where it's going.

"Before you can get into things like investing and saving for the future, you've got to figure out how you are spending it," Lee said.

Most people are surprised by how often they stop by the bank machine, and how much they spend on restaurants and takeout.

"ATMs are the black hole of finance," Lee said, adding that restaurant expenditures rank right up there on the list of budget-busters.

You may also want to eliminate the word budget from your vocabulary, she suggested. It's not a prison sentence.

"The term 'budget' has almost become equivalent to a four-letter word," Lee said. " I like people to look at it as a spending plan."

Software help

When tracking your spending, the many easy-to-use personal finance software programs out there, to which new features are being added every year, simplify the process enormously.

Before buying, you'd be well advised to research the programs, compare their functions and decide which one is right for you. (It doesn't hurt to read a few consumer reviews either.) Some of the leading programs out there include Intuit's Quicken 99, Microsoft Money 99, CashGraf Checks Plus 3.0 and Managing Your Money.

(Intuit partners with CNNfn.com's personal finance section.)

M. Eileen Dorsey, a certified financial planner in St. Louis, Mo., however, said the software programs alone won't bring you budgetary success.

"These programs do great in number crunching, but they are not so great in analyzing," she said. "A lot of people use them to keep track of their numbers, but they don't understand how to look at them and make judgments."

Getting help

Dorsey said one of the best (and cheapest) ways to educate yourself on how to interpret spending patterns is to pick up one or more of the workbooks that line the shelves at the local bookstore or library.

Spend some time getting acquainted with basic financing concepts before you create your own budget. Doing so will help you reach your financial goals faster without giving up all the goodies you enjoy.

"The best way is to just read a few books," Dorsey said. "Office Depot usually has them for $5 or $10 and they can help you through the difficult steps."

You can also check with the local banking institutions, which often distribute free pamphlets on managing your money, or stop by your regional consumer credit counseling service, which can put you in touch with finance professionals. (Use the office locator provided by the National Foundation for Consumer Credit.)

Lastly, Dorsey said you can sign up for a personal finance class at your nearby community college. A two-hour, two-night basics class can cost as little as $10.

Finally, if you don't feel comfortable crunching your own numbers, you can always hire a professional financial planner. It'll cost you, Dorsey warns, but you'll also get the benefit of a professional who can answer your questions and help get you started.

The most important thing is to do something.

"If you don't have some type of a budget, you tend to overspend because you don't know where your money is going, especially the miscellaneous items," Dorsey said. "You forget about buying chips and a drink at the 7-11, or picking up that magazine while you are waiting to pay for groceries."

Net worth and cash flow

One good way to begin your quest for fiscal control is to calculate your net worth on an annual basis, a helpful tool that gives you the clearest long-term picture of how well you control your spending, Dorsey said.

To calculate your net worth, add up all your assets. They include, but are not limited to, your car, home, antiques and collectibles, equity in investments and pension funds.

Be careful not to overestimate the value of your assets, which can throw off the chart.

"People tend to really over estimate the value of their car, for example," Dorsey said. "I would use the Kelley Blue Book value and even adjust it downward a bit."

Then, subtract from that your liabilities, such as your mortgage and car loan payments, taxes due, revolving lines of credit and credit card debt. The resulting number is your net worth.

"The number should be positive and it should be increasing from year to year," Dorsey said.

If it's not, you've got some cost-cutting to do.

Cash flow

Lee said another good way to keep track of your spending on a short-term basis is to complete a cash flow worksheet regularly.

Keep in mind that accuracy is important here too.

"If you're off by $100 a month on what you really spend, that oversight then is $1,200 every year," Lee writes in her book. "Think about this. If you can invest $100 a month over 20 years, and assuming an after-tax return of 8 percent, it could amount to as much as $60,000."

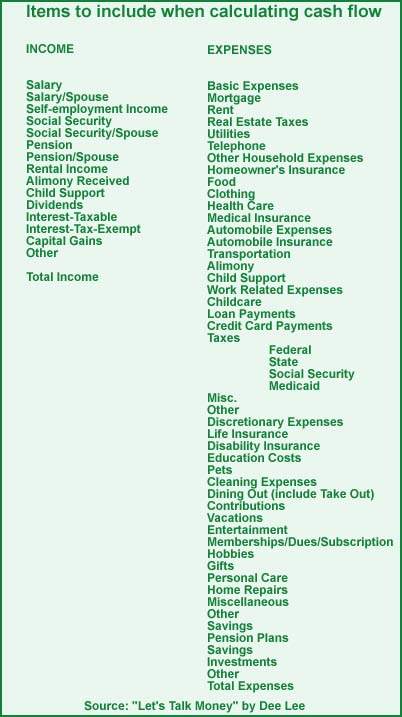

Your cash flow starts with the total amount of money you have coming in regularly, such as your paycheck, child support, dividends and interest payments, she said.

From this, subtract your expenses, which should include vacations, holidays, birthdays, home and auto repairs, real estate taxes and insurance premiums among other things. Tax payments you owed or returns you received after filing your latest returns also count, she said.

(Click here for a list of what to include when calculating cash flow.)

As with your net worth calculation, if you end up with a positive number, you're spending less than you earn. That's good. It also suggests you should begin looking into investments for the future.

If you're breaking even, Lee said you should strongly consider creating a budget to help you cut back on discretionary spending and put money away for a rainy day.

If cash flow is negative, that means you are using credit cards to supplement your income. That's bad. You have no choice but to set a budget and live by it.

Lee said it's not as big a sacrifice as it sounds.

"Sure, you still have to eat, but you can decide how much you spend on your food," she said. "Instead of stopping after work and picking up dinner, plan to cook at home more often. The same is true for entertainment, clothes, contributions, gifts and toys (the kids' or yours)."

One final word of advice: when you save money on groceries or any other purchase, put that money away. Don't run out and spend it on something else.

"I am amazed by people who tell me they saved $20 on their groceries," Lee said. "I say, 'great, what did you do with it?'"

Most often, she said, they don't remember. And invariably, it doesn't end up in their bank account.

"If you save money, put it in your piggy bank or put it in your savings account, but put it somewhere," Lee said. "I don't care where you put it. But make it tangible."

Budgets

The bottom line, experts say, is that we all need to budget. Whether your goal is to save enough for a new house or pay down your debt, you should establish a monthly spending plan that keeps spending in check. It may take some discipline, but Lee said you won't regret it.

"Budgeting just means making choices," she said.

|

|

|

Track your stocks

|

Note: Pages will open in a new browser window

External sites are not endorsed by CNNmoney

|

|

|

|

|

|

{kind=link}