|

Junking junk-bond funds

|

|

August 11, 1999: 7:42 a.m. ET

Investors are dumping shares at a rate not seen since Long-Term Capital crisis

By Staff Writer Martine Costello

|

NEW YORK (CNNfn) - High-yield bond fund managers can't exactly sing that old song about summertime and easy living.

Investors in recent weeks have been dumping junk- bond fund shares at a rate not seen since the crisis with Long-Term Capital Management last summer. And some big bond funds have been hit hard in the last week, spoiling what had been a nice recovery in 1999.

The worst part is there's no clear-cut explanation for the exodus, and no one is sure if the trend will continue. It could be caused by investors turning bearish, stock market volatility, concerns about rising interest rates, or a combination of many factors, junk bond analysts said.

"For us, it's personally frustrating, because earlier in the year we had a fantastic year going," said Nathan Grant, manager of the Value Line Aggressive Income Trust Fund. "With the drop down in the market and the indiscriminate selling, we've really given up a little ground."

A bad start to August

Junk-bond funds have weathered an estimated $1.5 billion in redemptions between July 30 and Aug. 6, according to Trim Tabs.com, a California researcher that tracks mutual-fund redemptions and other statistics. That figure is about 1.25 percent of total assets of high-yield funds, said Charles Biederman, president of the group.

Net asset values (NAVs) of high-yield funds have plunged 2.6 percent in the last 12 sessions, Trim Tabs.com said.

"High-yield fund investors are a lot more aggressive than traditional fund investors," Biederman said. "They're taking action."

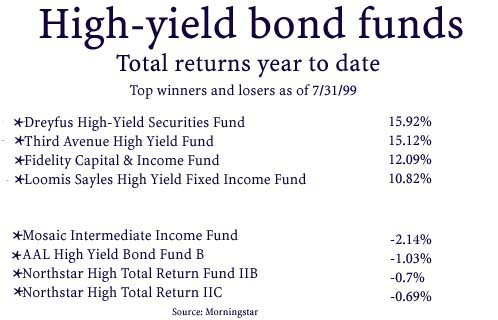

And while junk-bond funds are up an average of 3 percent year to date as of July 31, the recent week hasn't been so kind, said Sarah Bush, an analyst with Chicago fund researcher Morningstar.

For example, Pimco High Yield Fund lost 1 percent in the trailing week ending Tuesday, Bush said. Putnam High Yield Fund also lost a little more than 1 percent in that time.

"Last week was a bad one for high-yield funds," Bush said.

Grant declined to say how much his fund has lost recently, or the level of outflows. But he said the fund is still up about 3 percent year to date.

"We've definitely got redemptions, just like everybody else," Grant said. "All of the numbers have been negative."

High-yield funds are more sensitive to outflows than equity funds because they are less liquid, Grant said.

"A lot of (falling NAVs) has to do with fund flows," Grant said.

Some possible causes

What's happening? One problem may be that historically when the stock market is volatile, the risky high-yield market gets singed, Grant said.

"First and foremost, the flows in the high-yield bond market are tightly correlated with the equity market," Grant said. "When the equity market is weak and is very volatile, people take their money out of high-yield bond funds."

The problem is when investors sell their shares, money managers have to sell securities. But after the fall of Long-Term Capital Management, high-yield bond buyers are skittish when money managers start selling, he said. That in turn depresses prices.

Long-Term Capital is the high-flying hedge fund that nearly collapsed last summer, triggering a $3.6 billion bailout. Long-Term Capital was hit with big margin calls and was forced to liquidate holdings, which included junk bonds. Prices crashed.

"One reason may be investors fear we'll return to what happened last summer with prices," said Biederman, of Trim Tab.com.

Another source of investor angst may be wondering what the Federal Reserve will do, analysts said. Fed Chairman Alan Greenspan told the Senate Banking Committee recently that the Fed may raise rates to keep inflation at bay.

Investors already have accounted for a tightening when the Fed meets next on Aug. 24, Grant said. The redemptions may signal a fear that there will be several more adjustments before the year ends.

A slew of economic data last week also has kept investors guessing, said Morningstar's Bush, including second-quarter productivity, jobless claimsand factory orders.

"Last week's economic data could give you concerns about the economy," Bush said.

Looking ahead

But experts said the crystal ball looks murky.

For one, high-yield bond funds have been keeping their heads above water as the sector takes a beating.

"In general, high yield has been one of the brighter lights in the domestic bond fund world," Bush said.

And Grant said the outflows have taken place only in the last two weeks, so it's hard to predict what will happen. The market may be getting ready for a nice rally. Or, fears about interest rates and other problems, like the arrival of the new millennium, may throw cold water on investors.

"It's a very sensitive market," Grant said.

|

|

|

|

|

|

|