|

Guarding against disasters

|

|

September 15, 1999: 11:23 a.m. ET

Don't let tornadoes, hurricanes and earthquakes leave you in fiscal ruins

By Staff Writer Nicole Jacoby

|

NEW YORK (CNNfn) - For the millions fleeing the Atlantic Coast as Hurricane Floyd draws near, protecting their families may be at the forefront of most minds.

But securing funds should be another important consideration, as natural disasters such as hurricanes and tropical storms can wreak havoc on individuals' financial security.

People think "'it can't happen to me' or… 'if it does hit me, it probably won't be that bad,'" said Brent Neiser, director of collaborative programs at the National Endowment for Financial Education.

The frequency of natural disasters in the past decade belies this type of self-reassurance. Prior to 1987, the United States had never experienced a natural disaster with insured losses greater than $1 billion, according to the Insurance Information Institute. Since that time, there have been 8 such events.

And natural disasters can have much broader consequences than damage to your home or property. Storms can force you to temporarily live somewhere else, cut your flow of wages and ruin valuable financial records.

Taking inventory

Floyd is expected to come ashore Wednesday night in the vicinity of Charleston, S.C., and local authorities have ordered mandatory evacuations in much of the coastal region.

If you have not already done so, you should conduct a household inventory noting your possessions.

This type of list can help prove the value of what you owned in the event of destruction and increase the likelihood you will receive fast, fair payment from your insurance company. It also provides documentation for tax deductions when you claim your losses.

An inventory can be approached several ways.

"You can borrow a camcorder or a still camera and take pictures of everything. Or you can walk from room to room with a tape recorder and note everything you see," said Neiser.

Your descriptions should include cost, condition and age of each item. And don't skimp on the basics, such as towels and clothes. Their cost can add up if you have to replace them.

If possible, you should also note the model and serial numbers of more valuable items and photocopy receipts and canceled checks to prove their worth.

Computer software available at many retailers can help simplify the inventory process. Once you have compiled your list, it should be stored in a secure place away from your home, in a safe deposit box, or with friends and relatives who live in a different area.

Get ready to evacuate

Staying financially solvent during and after a disaster can be difficult, as the same storm or quake that leaves many families homeless also shuts down local banks and ATMs.

Consequently, putting some cash aside for this type of an emergency is a good idea.

"We always suggest that you keep the amount of money handy that you might need for a weekend away because you never know what will happen," said Leslie Credit, spokeswoman for the American Red Cross.

The Red Cross and the Federal Emergency Management Administration recommend preparing an "evacuation" kit that can be readily accessed if you need to leave your home abruptly.

The kit -- which can be as simple as a cardboard box -- should be large enough to include a small amount of travelers checks or easy-to-use denominations of cash; a list of important phone numbers, such as family members, reputable contractors and doctors; copies of medical and other insurance information; and a list of credit card, bank account and investment information.

You may also want to include negatives for irreplaceable personal photographs and the key to your safe deposit box.

Be sure to put important papers in sealed water-proof bags and store the box where you can get to it easily.

In addition to your evacuation kit, consider keeping some funds outside the local area, since the disaster that affects you could also affect your local financial institutions. A mutual fund money market account in another city or state is one option to consider.

While it may be tempting to store important documents in a home safe or fire box, they might not survive the intense damage sometimes wrought by hurricanes, floods and tornadoes. A safe deposit box may be a better alternative.

Preparing for the worst

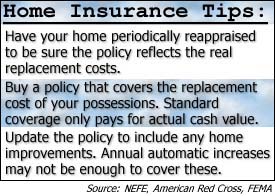

Homeowners' or renters' insurance can minimize the financial fallout that can result from a natural disaster. Unfortunately, many people fail to get insurance or don't get the extent of coverage they need.

"You have to buy the right kind of property insurance for the type of danger you're likely to face," said Neiser.

Most policies do not cover flood damage, for instance. Separate flood policies can usually be purchased for about $300 a year.

Earthquakes also usually require additional -- and expensive -- coverage. A $200,000 home may require as much as a $5,000 premium, with deductibles running between 5 percent and 10 percent. Earthquake coverage for the contents of a home may be not be included, as well as coverage for masonry and plate glass. So inquire closely about the extent of each policy.

Building codes, which theoretically have homeowners' best interests at heart, can become a financial burden after a disaster as families get weighed down by the costs of abiding by newer, stricter construction requirements. You may want to consider additional insurance to cover the expense of meeting these codes.

Another potential insurance gap is the home office. If you find out work-related property is not insured, consider additional business coverage that can usually be obtained at a modest fee. A small business policy, whose coverage is usually more broad, is another possibility.

After disaster strikes

The costs of rebuilding your home and replacing lost property can be great, especially if your insurance coverage is inadequate.

Luckily, the federal government offers low-interest loans to those who qualify in the aftermath of a natural disaster.

Both the Small Business Administration and Farm Service Agency offer loans to eligible low- and very low-income applicants to buy, build or repair housing in certain areas. Cash grants are also sometimes offered to those who don't qualify for loans.

However, depending on federal assistance is not always the best idea.

"The perception is that it is more generous than it is," said Neiser. "Grants are generally only for those that are completely wiped out or uninsured."

The rebuilding process will go much faster -- and much more smoothly -- if you lock down the proper insurance in advance, says Neiser.

Other post-disaster tips:

Be extremely cautious about contractors you hire to repair or rebuild damaged property. Unfortunately, a few dishonest contractors take advantage of people caught in the wake of a disaster. Be extremely cautious about contractors you hire to repair or rebuild damaged property. Unfortunately, a few dishonest contractors take advantage of people caught in the wake of a disaster. |  Work with a certified financial planner or tax accountant to figure out if you are entitled to any tax breaks. Although the tax code is complex, generally-speaking, you may take a deduction if the total amount of losses in one year is more than $100 and more than 10 percent of your adjusted gross income. Work with a certified financial planner or tax accountant to figure out if you are entitled to any tax breaks. Although the tax code is complex, generally-speaking, you may take a deduction if the total amount of losses in one year is more than $100 and more than 10 percent of your adjusted gross income. | | Notify creditors as soon as possible about lost bills or difficulties in paying bills. Explain the situation and try to negotiate an agreement to reduce payments or spread them out over a longer period. | |

|

|

|

|

|

|

|

|