|

Stocks vs. mutual funds

|

|

September 16, 1999: 9:56 a.m. ET

Experts debate the pros and cons, but say there are no easy answers

By Staff Writer Martine Costello

|

NEW YORK (CNNfn) - Your mutual-fund portfolio earns a measly 20 percent a year while the hottest stocks on Wall Street quadruple in a few months.

To make matters worse, you get stuck with a fat tax bill while your friends get rich on Microsoft and Yahoo!.

Meanwhile, five million people are buying stocks online, and even the most traditional brokerage houses like Merrill Lynch are getting into the electronic trading business.

Paper or plastic? Aisle or window seat? Stocks or mutual funds?

"We get that question all the time," said Mark Balasa, a certified financial planner with Balasa & Hoffman in Schaumberg, Ill. "They see 10 stocks in the S&P 500 doing so well, and they ask, 'Why don't I own them?' "

One of the great financial debates at the close of the 20th century is whether investors should own stocks or funds. But don't hold your breath for an easy answer.

"No one strategy is right for all investors," said Deborah Frazier, vice president and senior financial consultant at Merrill Lynch.

Frazier said people first need to set their investing goals and decide how much risk they can tolerate. They also need to examine their "temperament," or the patience to allow their portfolios to grow over time. You need at least 18 months for stocks and three years for funds, she said.

Frazier said mutual funds are great because they allow people with less money easy diversification. Funds also allow people to reap huge gains from dollar-cost averaging, or small, regular contributions over time.

"Mutual funds are one of the best inventions of this century," Frazier said. "They were designed for individuals to invest in the market the way millionaires do."

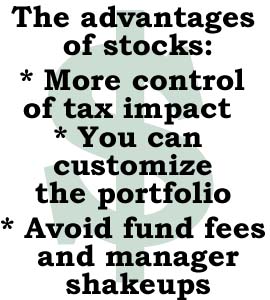

But perhaps the biggest disadvantage of funds is you have no control over your tax bill, experts said. If you own mutual funds in a taxable investment portfolio, you'll get a bill every year.

So if your manager makes a lot of trades in a year -- or if he sells a stock that has appreciated in value -- it could mean a big capital gains bill, as much as 20 percent on assets held longer than a year.

"The tax implication is the Achilles heel," Balasa said. As a result, Balasa recommends index funds that are more tax-efficient. He would recommend mutual funds -- even for somebody with $2 million to invest.

"You could have a multi-million-dollar portfolio and still have a strong argument to have some funds," Balasa said. Besides offering diversification, mutual funds free people from a lot of paperwork and offer the expertise of a professional money manager.

For those lucky people with many millions to invest, they can hire managers to run private accounts in the major asset classes such as large caps and international stocks, Balasa said.

Hugh Johnson, chief investment officer at the brokerage First Albany Corp., said a private account manager will pick stocks that not only deliver the best returns but limit the tax pinch. He has a $1 million minimum on such accounts and manages a total of $550 million in assets.

"They come to me because they want special treatment," Johnson said. "There is nothing that irritates substantial investors more than paying taxes."

Johnson said even though diversification in funds will protect you in a downturn, it will also give you what he calls "dispersion" that will keep you from big gains. That's why he owns only 38 names.

"That's why I think it's a better idea to have your own portfolio," Johnson said.

Rich Stevens, a principal at fund giant Vanguard Group, acknowledged most of the industry has made performance the top priority regardless of the tax implications. Vanguard has made cost control a priority.

"The problem is a lot of mutual funds totally disregard the tax consequences," Stevens said.

But Stevens argued that a private account isn't necessarily a better alternative than a tax-efficient, cost-sensitive fund. He doesn't see any reason why a person couldn't put as much as $1 million in a single Vanguard stock fund.

Vanguard's fees are about 0.28 percent a year, compared with about 1 percent for a private account, Stevens said.

Adriane Berg, editor of the investing newsletter Wealthbuilder, said people with $100,000 or less might want to look at mutual funds instead of stocks to make sure they get enough diversification in their portfolios. But if they have more than that, she thinks stocks make the most sense.

Trading costs have come down so much that it isn't nearly as expensive as it used to be, Berg said. And picking winning stocks isn't a mystery, either.

Wealthbuilder has a recommended stock portfolio that began in 1996 with $250,000 that is now worth $506,719, an increase of 102.7 percent. The portfolio includes 44 names, such as Microsoft (MSFT), Coca-Cola (KO), Starbucks (SBUX), and American Express (AXP).

"We're very bullish with the average investor being able to handle their own stock portfolio," Berg said. "You don't have to be a genius."

|

|

|

|

|

|

|