|

New homes get old quickly

|

|

July 27, 2001: 9:52 a.m. ET

Fans' love of new stadiums can be short lived, turning winning teams to losers

A Weekly Column by Staff Writer Chris Isidore

|

NEW YORK (CNNfn) - In terms of money invested in over-valued, money-losing ventures, only dot.com companies in their heyday could compete with new stadiums and sports arenas.

But unlike the dot.coms, there's still a long line of people eager to sink more money into new stadiums.

New York is on the verge of announcing plans for new baseball stadiums for both the Yankees and the Mets, while across the river New Jersey is working out details of a deal for a new arena for the NBA's Nets and the NHL's Devils, which both are part of the same holding company that owns the Yanks.

|

|

|

Chris Isidore covers the business of sports for CNNfn.com | |

Up in Boston, the Red Sox are negotiating plans to spend an (initial) estimate of $350 million of the team's next owner's money on a new Fenway Park, which would make it the largest private investment in sports history.

These would be just the latest stadium deals that have cost fans, team owners and -- much more often than not -- taxpayers $10 billion during the last decade, as about two-thirds of the major sports teams in North America either got new homes or started construction.

Despite generous tax dollars involved in most of the stadiums and arenas, none of the teams got a completely free ride into their new homes. And while it often is argued that tax dollars could be better spent on schools, roads and other public services than on playgrounds for millionaires and their well-healed friends, what is less well known is that the new venues aren't always the best deals for the teams that play in them.

"The bottom line is no, it's not worth it," said Roger Noll, professor of public policy and business at Stanford University School of Business, and an expert on the business of professional sports. "It'd be worth it if you could hold down cost. But even if you get the stadium for free, you can't sustain the revenue without improving the quality of the team. You have to get more high-paid players to sustain that revenue."

| |

|

|

Artist's rendering of the new Fenway Park, which the Boston Red Sox propose spending $350 million to build, making it the largest private investment in any new stadium. | |

Still, owners, sports writers and fans look at the regular sellouts and winning seasons that have accompanied new parks such as Jacobs Field in Cleveland, Safeco Field in Seattle, PacBell Park in San Francisco and the one that helped start the current building boom � Camden Yards in Baltimore -- and they want the same for their own teams.

But the truth is that after a relatively brief honeymoon, generally about six or seven years if not sooner, fan interest starts to wane. Then it takes a winning team, not just a new facility with all the bells and whistles and improved concession stands, to keep fans in the seats.

"For a private enterprise to build a baseball stadium, particularly a single-purpose stadium, that's a tough call. It's very much a tough nut to cover," said Norman Seagram.

Seagram should know. He's the president of Sportsco International Ltd., which bought Toronto's Skydome for a fraction of its construction price in 1999, after the group that owned it filed for bankruptcy protection.

While Seagram won't reveal the exact price Sportsco paid for the half-billion dollar stadium, he admits estimates of $80 million are in the ballpark.

Honeymoon, attendance gains don't last

Skydome is a perfect example of the honeymoon-doesn't-last-forever syndrome.

Opened in 1989 as the Blue Jays baseball team stormed to their second division title in three years, the then state-of-the-art stadium soon was filling to capacity every night.

In 1991 the Blue Jays became the first team to top 4 million fans in a season, a feat they repeated as they won back-to-back World Series in 1992 and 1993.

This season about 10 percent of its 50,516 seats are covered with tarps each night to help avert the effect of seeing so many empty seats on television. The team has averaged only 22,292 fans a game so far this year, less than half of the reduced capacity and only about two-thirds of what they averaged their last fives years in woefully inadequate Exhibition Stadium, a venue never designed to host baseball games.

And the Blue Jays still are competitive, even if no longer a championship team. For losing teams, the fall can be much faster.

|

|

|

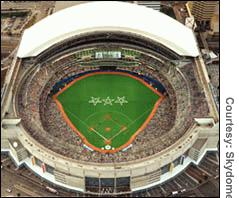

Skydome was selling out regularly in 1991, when it hosted baseball's All-Star game. Today 10 percent of its seats are covered with tarps and fewer than half the remaining seats are sold on an average night. | |

Last year Comerica Park, the new home of the Detroit Tigers, saw attendance jump by two-thirds over the average of the last five years in Tiger Stadium, but that still was only a modest 30,106 per game, or about three-quarters of capacity. This year attendance has fallen by 23 percent from last year to 23,041.

"The issue is durability," Noll said. "As an economist, all my instincts tell me just as the dot.com bubble had to burst, the small-market, new-stadium phenomenon had to burst."

The Red Sox probably have more to gain from a new park than any other team. The current Fenway holds only 33,871 fans, by far the smallest in the league. More importantly for revenue, it has so little concession space that Noll estimates that two-thirds of what fans spend on things other than tickets doesn't go to the team. The new stadium would not only allow it to capture much of those lost concession dollars, but it would raise seating capacity by a third and double the number of luxury boxes.

But Noll says that even if the new Fenway doesn't have any empty seats, he doubts it will be worth it for the team from a financial point of view. And if any of the potential buyers of the team have any doubts, they should look at what happened in Montreal, where hockey's Canadiens closed the equally beloved Forum in 1996 and moved to the new Molson Center, built for $230 million by Molson Breweries, which purchased the team in 1978 after years of ownership by Molson family members.

Attendance hasn't slipped -- more than 90 percent of the seats still are sold every night. Molson found the revenue stream from the new arena was not enough to support the cost of the building.

This week it sold the arena and 80 percent of the team itself -- for only $180 million.

|

|

|

|

|

|

|