|

Strong dollar not all bad

|

|

August 15, 2001: 6:21 a.m. ET

While the currency's strength has eroded profits, it's also provided benefits

By Staff Writer Mark Gongloff

|

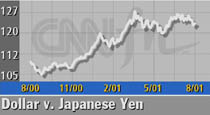

NEW YORK (CNNfn) - Throughout the long, grim, second-quarter 2001 earnings season, Wall Street heard the same sad story over and over again: The strong dollar is killing corporate profits.

Though the dollar has weakened a bit in recent weeks, it's likely to hold its strength relative to other major currencies. That's bad news for U.S. companies like Procter & Gamble Co. (PG: down $0.07 to $72.43, Research, Estimates), the nation's biggest consumer products maker, which reported its first quarterly loss in eight years last week, due in part to unfavorable exchange rates.

"A strong dollar takes away companies' pricing power because imported goods come in a lot cheaper, and it impacts earnings because they can't raise prices," said Maureen Allyn, chief economist with Scudder Kemper Investments.

The greenback's strength is also bad news for the sluggish U.S. economy, at least in the short term.

"It's probably going to subtract 0.8 percent from [gross domestic product] growth this year," said Anthony Chan, chief economist with Banc One Investment Advisors.

In a strong economy � which the U.S. enjoyed until the middle of 2000 � such a drag on growth was hardly noticeable. In the current economy, with companies slashing production and cutting hundreds of thousands of jobs in an effort to remain profitable, it could sink gross domestic product (GDP) into negative territory.

And if labor costs rise while corporate profits stay low, then companies may have to cut more jobs to keep those profits afloat, which could be the killing blow that sinks the U.S. economy into a recession.

"So far, layoffs have been bad, but the job market has held up pretty darn well," Allyn said. "If companies really get the axe out more than they have, that sets a bad dynamic in motion. That's what's got to give [Federal Reserve Chairman] Alan Greenspan nightmares."

Click here for more on the Fed and rates

The Fed has slashed its target for short-term interest rates six times this year in an effort to keep consumers spending despite hundreds of thousands of job cuts.

Though a weaker dollar could help save jobs and keep consumers spending, it could also increase the likelihood of inflation, which could make the Fed reverse course and start raising rates again.

A stronger dollar, by contrast, keeps prices down and has a higher purchasing power � benefits not to be overlooked.

"For every 10-percent appreciation in the dollar, it cuts inflation by one full percentage point, assuming the strength of the dollar is sustained," said Sung Won Sohn, chief economist for Wells Fargo & Co.

And there are other, longer-term benefits of a strong dollar that could outweigh the short-term cost to corporate profits and GDP growth. A strong dollar that keeps interest rates and inflation low also encourages capital investment from overseas; all these factors fuel economic growth. It also forces manufacturers to build better products in order to compete with overseas goods.

"Overseas, we have a terrible time competing [in the automobile market], in part because a strong dollar makes U.S. cars more expensive," Sohn said. "Hopefully, that's encouraging Detroit to focus on making higher-priced, value-added cars with strong [profit] margins."

Another benefit of a strong dollar is that other countries are encouraged to use the dollar as their official currency, paying the United States for the privilege.

"Panama has a dollarized economy," Sohn said. "We provided them with currency, and they had to give us something for it. It's like a free loan from Panama. At a 5 percent interest rate, we're [saving] $20 billion a year. That's not peanuts."

Click here to track currency rates

The long-term benefits of a strong dollar may outweigh the short-term costs, but that doesn't satisfy Wall Street investors, who usually want immediate profit improvement at any cost. Possibly hoping to mollify them by keeping the dollar from flying too high, the Bush administration has at times seemed less than enthusiastic in its support for the currency.

Since George W. Bush took office, he and Treasury Secretary Paul O'Neill have walked a fine line, at times making comments about the dollar that briefly dulled its shine before making other comments that reaffirmed their support.

Wednesday, O'Neill reaffirmed his support for the dollar after the International Monetary Fund warned that the lack of sustainability of the yawning U.S. current account deficit raised the risk of a sharp depreciation in the dollar.

So far, O'Neill and Bush have averted a dollar free-fall that could cause overseas investors to pull out of U.S. financial markets, though concerns about the health of the U.S. economy have pushed the dollar down more than 5 percent from 15-year peaks reached in early July.

"In the short run, it's a no-win situation for the administration," Anthony Chan said. "But longer term, it's a win-win situation because you keep financial flows going, and economic growth will become a lot firmer."

Of course, the idea of having a "policy" on the strength of the dollar is something of a myth, since there's not much a president or a Treasury secretary can do to support the dollar if investors decide to dump it.

"I have never thought that what a government wants its currency to do makes a hill of difference," Allyn said. "What's holding the dollar up is a desire to put money here and a faith in Greenspan and Corporate America. That's all psychology, and it can turn on a dime."

Bush will likely do whatever he can to keep that psychology in favor of a strong dollar, especially since the continuing economic slowdown and slump in corporate profitability could erode investors' faith in U.S. investments.

And if the European Central Bank finally gets around to cutting interest rates, as some expect it might soon, that would also be unfavorable to the dollar.

But many observers expect the ECB to cut rates by only 25 percentage points, to 4.25 percent, while the U.S. Federal Reserve has already cut its target for short-term rates this year by 2.75 percent, to 3.75 percent.

"My suspicion is that the dollar will remain relatively strong because, even if the ECB starts lowering rates, they've got a lot of catching up to do," Chan said. "The prognosis for the dollar remains cautiously optimistic."

|

|

|

|

|

|

|