|

Deregulation a success?

|

|

December 18, 2001: 7:00 a.m. ET

Energy privatization leads to turmoil in California but not Enron collapse.

|

NEW YORK (CNN/Money) - Deregulation may have pushed the state of California into turmoil but it can't take the credit for the collapse of Enron Corp., the once powerful energy trader.

Allowing California consumers to choose their power providers seemed like a great idea in the late 1990s. The initial goal of the program was to dethrone monopolies and give consumers a choice when they buy power. The free market theory hoped to drive down energy prices while improving services.

But power deregulation has come slowly and many states are still in the early stages of privatization. Only about 20 percent of U.S. states have fully deregulated while gas privatization is about 90 percent complete, analysts said.

California, which began privatizing in 1996, sold off its power plants to companies such as Dynegy Inc., El Paso Corp. and Williams Cos. (WMB: down $1.36 to $22.95, Research, Estimates).

But state officials required the companies to sell their electricity to a single state-run power exchange. Such efforts caused energy prices to soar while consumers suffered through eight rolling blackouts in the past year.

In 1999, the state of California at its peak paid $7.4 billion for 45,000 megawatts (MW) of power. By the next year, the state used only 43,000 MW but the price tag more than quadrupled to $33.5 billion. This year, California is now on track to use 41.1K MW at peak use and is expected to spend $50 billion, according to data from the San Francisco-based Public Utilities Commission.

But some believe that the attempt at privatization failed because it didn't go far enough and allowed states to regulate rates.

"The case in California wasn't full fledged deregulation," said analyst Mike Barbis, of Fulcrum Global Partners.

Free market proponents point to Pennsylvania, the must successful example of privatization, which, along with Delaware, Maryland and New Jersey, is part of a wholesale market.

California's experience is on par with Montana's, where state official's decision to sell all of its generators to a single company which initially produced a surge in industrial wholesale prices.�

"We've had some hiccups but [deregulation] has been successful in a lot of places," Barbis said. "It's still too early to pass judgment."

Free market proponents claim that energy deregulation can succeed if given time. Commercialization has led to an increase in services and low prices for the telecommunications and airlines sectors, as well as railroad and trucking.

"The marketplace will take care of energy and provide more services and cheap prices if allowed to work," one analyst said, who declined to speak for the record.

But some disagree. "Deregulation doesn't work for a fundamental economic necessity which you must have and that can't be stored," said Commissioner Loretta Lynch of the San Francisco-based Public Utilities Commission.

Rise of energy merchants

Deregulation has given birth to a new breed of energy merchants such as Duke Energy Corp. (DKE: up $0.19 to $24.24, Research, Estimates), Dynegy Inc., El Paso Corp. (EPG: down $1.63 to $38.60, Research, Estimates) and Mirant Corp (MIR: down $2.35 to $13.35, Research, Estimates) who have all benefited.

In the last four years, the revenue base of these top energy traders has jumped to $350 billion from $70 billion, analysts said.

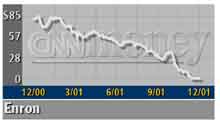

While some companies have surged, others have failed. One of the most notable, Pacific Gas & Electric Co., California's largest utility, filed last April for bankruptcy protection. Earlier this month, Enron Corp., once one of the biggest and most influential companies in the United States, filed the largest bankruptcy in United States history.

But some pegged PG&E's bankruptcy as more of a strategic move. PG&E opted for bankruptcy protection so that it could finish the experiment of deregulation in California, Lynch said.

"PG&E was sitting on over $2 billion in cash when it filed," PUC's she said. "They had plenty of money."

"PG&E did have assets they could've used to subsidize," added Fulcrum's Barbis.

Enron's collapse is also not the result of deregulation, analysts and industry sources said. Led by CEO Kenneth Lay, the once powerful energy trader was a major proponent of deregulation and profited from the experiment.

Enron's woes began after regulators began investigating company transactions with a partnership created by its former chief financial officer, Andrew Fastow, that resulted in a $1.2 billion reduction in the value of investors' holdings.

Enron's questionable accounting eventually led to the failure of its $9 billion merger with Dynegy Inc. The troubles caused Enron's stock to plunge to roughly 50 cents from $37 on Oct. 16.

"Enron got in trouble with too much debt," said Fulcrum's Barbis. "Investors and analysts didn't realize how much debt they had because it was hidden."

With Enron out, rival traders will be vying for the $200 billion in revenue that it was expected to produce in trading this year, said analyst John Olsen, of Sanders Morris Harris.

"Enron is a one-time occurrence," Olsen said. "Trading didn't put it down but rogue financing. They improperly financed a lot of overseas hard assets and didn't disclose the impact to earnings and balance sheets."

But one competitor, Calpine Corp., appears to be suffering from the Enron fallout. Moody's Investor Service recently cut Calpine's debt to "junk" status on concern over the company's liquidity and financial flexibility. The downgrade of Enron's debt triggered debt covenants and forced accelerated payments. The downgrade also caused Dynegy to pull out of its $9 billion takeover of Enron.

Calpine needs about $7 to $8 billion for the 17,000 MW of gas-fire generating capacity it has in development, said analyst John Olsen, of Sanders Morris Harris.

The San Jose, Calif.-based power company has a generating base of about 7,000 MW currently and wants grow to 70,000 MW by 2005.

"That's looking increasingly remote now," Olsen said. "Calpine has a ton of debt and the concern is they don't have enough money to meet their obligations."

Lehman analyst Dan Ford also lowered his rating on Calpine stock to market perform from strong buy. Shares of Calpine (CPN: down $0.30 to $12.90, Research, Estimates) dropped to an $10 low last week and shed nearly 5 percent on Monday.

|

|

|

|

|

|

|