|

NEW YORK (MONEY Magazine) -

Mark and Lori Gorney are well on their way to the millionaire's club, and they're not real estate flippers or lottery winners.

The autoworker and the sales associate have hammered out a financial success story that looks a lot like the American dream.

"You have to make rules and plan ahead," said Lori, 42, who works part time in a jewelry store in Saginaw, Michigan, the small city the Gorneys call home.

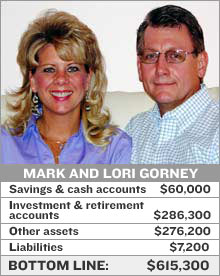

Over the course of a 20-year marriage, their discipline and planning have allowed them to put two sons through college, rack up a net worth of more than $600,000 on an annual combined income of $115,000 and plan on an early retirement.

Bank on rainy days

A lifetime job at a corporation like General Motors was once considered a surefire way to financial security. But in a post-Enron age more of the nation's workers feel this is no longer the case.

Mark Gorney, however, has made a longtime career at the automaker and feels fairly positive that seniority and a great work record will keep him at the job.

Moreover, a willingness to accept uncertainty as a fact of life has put the couple on financially sound footing.

"Mark always worked overtime when it was offered to him, but we always lived on his 40-hour-a-week salary," said Lori.

"You never know what can happen and you never know if jobs will always be there," added Mark, 52.

The couple used overtime pay as an opportunity to put away extra cash for emergencies and rainy days. And over the long-term the couple has socked away about $290,000 in retirement savings.

The Gorneys' primary savings strategy is to build equity in their home and to save 10 percent of their gross income in their GM retirement personal savings plan.

All of this is being done with the goal to retire within the next three to six years. To make early retirement possible they are also in the process of building a sizeable cash reserve to bridge the years until their personal savings plan and IRAs are accessible.

"We also keep about $6,000 in cash as a cushion for emergencies," Mark said.

Their main investments are mutual funds, with a proportionally small share in GM stock, the company where Mark works as a skilled laborer in the power train division.

Little things mean a lot

The Gorneys' tremendous sense of fiscal responsibility ensures that every cent helps.

Based on experiences during his previous marriage, Mark, 52, established that he needed to manage his finances well and keep track of his spending.

In his new marriage, the couple said they never had a problem agreeing on financial goals and had similar attitudes toward money management.

"We set a $50 rule. If one of us wanted to spend more than $50, we had to check with the other person," said Lori.

"While things have changed and the rule is $100, it's still the same thing," she added. "We don't impulse buy because you have to wait to tell the other person about what you want and decide together. It makes a system of checks and balances."

In addition, the couple gives themselves weekly allowances and keeps track of that cash.

"If you don't know where it goes, it can slip away," said Mark.

The couple has amassed a lot of small ways to save and eliminate hidden expenses that add up, like never paying bills late and getting hit with subsequent fees and never carrying a credit card balance.

They are also careful to do their financial detective work, and do not carry interest that isn't tax deductible.

Lori, who works about 19 to 29 hours a week at a jewelry store, has the time to do a lot of the planning that helps she and her husband save. She makes meals at home, packs lunches, makes trips to the bank to avoid ATM fees and stays on the lookout for hidden charges.

While their fiscal discipline may seem strict to some, it has afforded them the ability to help put Mark's two sons from his previous marriage through college, buy a great home and have the financial freedom and security to enjoy their lives.

Click here to read about Millionaires in the making Amy Chan Hilton and Edgar Hilton.

Click here to read about Millionaires in the making Dave and Annie Hall.

To see how other people are on track to wealth, click here.

Think you're a millionaire in the making? If you would like to be featured, click here.

|