Christopher Ortega and Alicia McDonald have shaken their debt by buying only what they can afford.

NEW YORK (CNN/Money) - At the end of the evening, when it's time to settle the check or close the bar tab and most people reach for the plastic, Christopher Ortega just says no.

It's not like Ortega is trying to stiff anyone. It's just that after years laboring under consumer debt, he and his long time girlfriend Alicia McDonald have used a cash-based strategy to finally emerge into the land of checkbook surpluses.

And they're emerging with the tenacity of a well-seasoned debt collector.

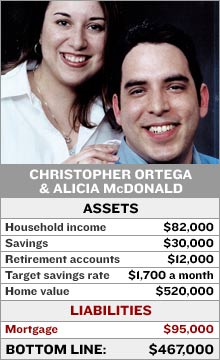

The 28-year old independent financial planner and 27-year old McDonald, a title officer, are just a few payments away from wiping out nearly $35,000 in commercial debt. At that point they plan on socking away an additional $800 a month on top of the $900 a month they are currently saving. Combine that with the $420,000 the couple has in home equity and they'll be millionaires by the time they're 45.

"All of a sudden we're talking about saving $1,700 a month,' said Ortega. "The benefits of being on a cash system really pay off."

Like many people, the couple got into debt during college when there were lots of expenses and little time for work.

To dig themselves out they have had to scale back on some things and put off others, including marriage.

"We could have brand new cars and make sure the wedding is completely funded and do a bunch of landscaping in the back, but we'd have to make all these payments to these financial institutions that don't really benefit us," said Ortega. "Sometimes we just have to wait a little longer."

Before taxes the couple makes about $82,000 a year, or $6,800 a month. Their monthly budget looks like this:

$1,700 in taxes$500 for insurance (health, car, mortgage, life)$1,700 for the mortgage, a second mortgage and the remaining consumer debt$2,000 spending money$900 for saving

The extra $800 in savings, which will bring the couple up to $1,700 a month, will come when the remaining consumer debt is paid off in the next few months and from diverting some tax money to invest now and relying on a mortgage tax refund to make up the difference later.

Ortega plans on adding the extra money to a simplified employee pension (SEP), a kind of 401(k) for the self employed. That will complement the $500 a month they are already stashing into their IRA and $400 a month they put into an emergency savings fund.

Granted, much of their wealth is based on the paper value of their home, which they purchased in 1998 for $114,000. The three bedroom house, to which they recently added a 700 square foot addition to for Ortega's parents, is now worth around $520,000.

Located in Modesto, Calif., 90 miles south of Sacramento, Ortega says real estate prices in the area have benefited from people moving from the San Francisco area to places inland, as prices on the shore have grown even more.

He says they were extremely lucky to buy when they did, and credits his mother, a real estate agent, for spurring their decision.

"She said 'This area is going to be another San Jose, buy,'" he said.

Ortega says his main motivation for saving is to avert any financial troubles further down the road. He said his parents had a hard time making ends meet and he wants to make sure he and Alicia, who have been sweethearts since high school, don't end up in similar circumstances.

"It's very important for me to know that she won't have to struggle with money," he said.