|

NEW YORK (CNNMoney.com) -

While today's most popular TV and computer screens are flat, shares of Corning, which makes the glass for these products, are anything but.

The Corning, N.Y.-based maker of glass, optical fiber and cable is one of the best performing stocks in the S&P 500 this year: its shares are up nearly 75 percent.

Thanks to the ultra-hot market for flat-panel TVs and computer monitors, earnings for 2005 are expected to nearly double, with analysts forecasting a profit of 85 cents a share, up from 45 cents last year.

That's a far cry from 2002, when the company's shares were trading at about a buck and change.

At the height of the tech and telecom boom, Corning's (Research) shares zoomed north of $100 from about $15 at the start of 1999 thanks to a rip-roaring boom in the company's fiber-optic cable business. But after the tech bust, profits plunged some 70 percent in 2001 and the company lost money in 2002.

Corning's turnaround has been nothing short of remarkable. But can it last? And even if it does, has the time to buy already passed?

Consumers down with LCD

Corning says it's just at the beginning of a new growth phase.

Vice chairman and CFO James Flaws noted that much of the growth in the company's display technologies business, which makes liquid crystal displays, or LCDs, the flat screens that go into computer monitors, handheld devices and some televisions, has been from computer monitors, not flat-screen TVs.

The business accounted for more than 40 percent of Corning's sales in the third quarter, and Flaws said the LCD TV market has plenty of room to grow.

Analysts agree that despite some jitters about the economy, consumers still want to plunk down money for high-end TVs.

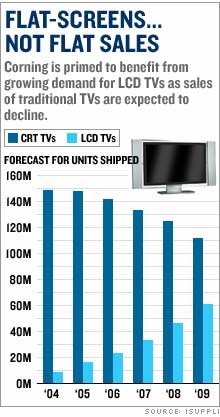

Shipments of LCD TVs are expected to hit 17 million in 2005 and then double by the end of 2007, according to market research firm iSuppli, which tracks the semiconductor market. LCD TVs are also expected to be hot items during the holiday shopping season and should get another pop early next year leading up to the Super Bowl.

"We are not going to see a slowdown in demand for LCD TVs," said Nikos Theodosopoulos, a UBS analyst. "Oil hit $60 and there was no slowdown. We are still in the early phase of flat panel TVs."

But demand for flat-screen products isn't the company's only advantage. Analysts say new regulations in Europe, North America and Japan restricting diesel fuel emissions will boost Corning's unit that makes filters to control emissions from diesel engines, among other things.

That business, while perhaps not as sexy as flat-screen electronics, is expected to give Corning some oomph in 2007, not to mention diversifying the company's revenue stream. The division accounted for about 12 percent of total sales in the third quarter.

Corning also gets some juice from its 50 percent ownership of Dow Corning, which makes silicones and silicon-based products and technologies.

C.J. Muse, a Lehman Brothers analyst, calls this stake a "hidden gem," because Dow Corning owns two-thirds of Hemlock Semiconductor, which makes polycrystalline silicon, used to make computer and cell phone chips as well as solar panels.

Too much riding on one business?

One area of concern is whether Corning has staked too much on one line of business. If the company simply rides the LCD wave the same way it rode the telecommunications wave in the 1990s, it could take another nasty fall.

But Flaws, who joined Corning in 1973 and has lived through its ups and downs, said the company learned an important lesson since the telecom bust.

"We over-invested in telecom at the same time it was growing," he said, adding that while the company is not going to limit LCD production to prevent the business from becoming too large, the company's primary research and development dollars are going toward its environmental unit, which includes the diesel fuel filters, as well as life sciences, where Corning makes vials, petri dishes and other products for labs.

As for the company's fiber-optic business, Flaws said sales have stabilized the past two years, but heavy investments have kept the business from producing profits.

Investors and analysts are also paying close attention to a report in Barron's noting that since the beginning of November, Corning insiders have sold 1.9 million shares of Corning stock worth $37 million.

But Lehman's Muse said he does not see that as a concern, noting Corning executives who were paid with stock options and little cash when the stock was near its lows are now diversifying their portfolios.

Another potential risk is the competition.

While Corning's the leader in the LCD market, it faces competition from two companies in Japan, Asahi Glass and Nippon Electric Glass, number two and three in the market.

Corning is making the latest generation of glass but Asahi is currently recognized as the price leader. If Asahi and other competitors catch up to Corning's technology, they could undercut prices, which would pressure Corning's profit margins.

"We feel confident that Corning has no incentive here to try and seek further market share through lower prices but that's not to say that its competition won't try and do that," said Matthew Smith, an analyst for CIBC World Markets.

The glass is half-full

So what should investors do? Corning now trades at roughly 20 times expected 2006 earnings, a 25 percent premium to the S&P 500's multiple of 15.7. Given that the stock has doubled in the last year, is it too expensive?

Muse at Lehman doesn't think so. "The valuation to me is pretty damn cheap," he said, noting that many other leading tech stocks trade at price-to-earnings ratios above 30.

"Should Corning trade at that level? Not necessarily, but given the growth prospects they definitely deserve a premium to the current multiple," he said. Analysts expect earnings to grow about 18 percent in 2006, more than twice the projected growth rate of 7 percent for the S&P 500.

CIBC's Smith said the company is well positioned for 2007 as well. "When you start to look at 2007 estimates, that could be the driver for share price appreciation, particularly if Corning is demonstrating continued growth in LCD glass plus the developments in the diesel business." he said.

While investors can't expect smooth returns -- after all, Corning is a tech company -- Americans' lust for the latest slick gadgets should secure solid earnings growth for Corning for years to come.

----------------------------------

For more about personal technology, click here.

LCD TVs and other high-tech gadgets are hot items for the holidays. Click here.

CIBC's Smith does not own shares of Corning and his firm has no banking ties to the company. Lehman's Muse does not own shares of Corning, nor does his firm have banking ties to the company.

UBS' Theodosopoulos does not own shares of Corning, but a member of the UBS research team, or one of their household members, has an ownership position in Corning.

|