All the Times that's fit to sell

The New York Times Co. has lots of history, but its future isn't promising. Now might be time to succumb to the publishing industry's urge to merge.

NEW YORK (CNNMoney.com) - The Gray Lady needs to get hitched soon, or else she might wind up an old maid. That's right, the venerable New York Times Co., which also owns the Boston Globe and International Herald Tribune, would be wise to succumb to the urge to merge in the rapidly consolidating newspaper business.

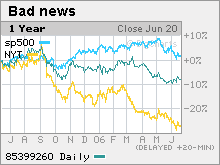

Let's face it, Wall Street is not overly confident about the company's growth prospects. Sure, the entire newspaper industry has taken a tumble due to concerns about how more and more readers (and advertisers) are shunning ink for online publications. But shares of the New York Times (Charts) have underperformed its peers, falling 11.5 percent this year and 27 percent in the past 12 months, compared to a 3.5 percent drop in 2006 for the S&P Publishing index and 8 percent decline during the past 12 months. Yes, the company has been touting its online offerings such as its premium tier TimesSelect service and Web guide About.com as successes that are driving growth. During a presentation Tuesday at the Newspaper Association of America's 2006 Mid-Year Media Review Conference, New York Times chief executive officer Janet Robinson stressed that digital revenue now accounts for 7.5 percent of the company's total sales, and that Internet ad revenue increased 24 percent through May. Robinson was particularly proud of the fact that TimesSelect, which requires readers to pay to view certain stories from top Times columnists, was doing well. "Conventional wisdom in the industry was that consumers would not pay for content that previously they got for free," she said. Still, Times Select has generated just $6 million in sales so far, a rounding error for a company expected to post $3.5 billion in annual revenue this year. Online is just not big enough to significantly move the needle for the New York Times. This year, analysts expect the New York Times to report an overall sales increase of only 3 percent and earnings drop of 3 percent. That's weaker than the industry average. And in 2007, Wall Street is forecasting just a 2 percent increase in sales and 3 percent rise in profits. And the Times, with a $3.5 billion market value, has to be viewed as a more likely seller than buyer. That's because competitors such as the Washington Post (Charts), Gannett (Charts) and even the troubled Tribune (Charts), which is being pressured by its second-largest shareholder to spin off its TV station business from its newspaper publishing operations, have larger market capitalizations. All in the family

But there is one big obstacle to a New York Times sale. The Ochs Sulzberger family owns 88 percent of the company's class B shares, which have super-voting power and give the family the right to elect 9 of the company's 13 board seats. So barring a change in the Times' stock structure, it's virtually impossible to imagine the company agreeing to a sale unless the family wants to sell out, which it has shown no indication of doing. In fact, Robinson said Tuesday that the Times remained focused on more acquisitions or strategic investments, particularly in online media. In addition to the company's purchase of About.com last year, the Times has also purchased stakes in privately held online job search site Indeed and blog network Federated Media Publishing. "We are building online what we have successfully created in print, that is, the community of shared interests," Robinson said. "These properties provide us a window to identify and benefit from trends as they develop." But just because the Times is continuing to scour for more Net purchases doesn't mean that a future sale of the company can be ruled out. After all, Wall Street is stepping up its pressure on the company to make changes. Follow the lead of Pulitzer and Knight-Ridder?

In April, Morgan Stanley Investment Management, which owns more than 5 percent of the Class A shares, withheld its votes for the company's board of directors in order to protest the company's dual class stock structure. And Goldman Sachs downgraded the stock earlier this month, citing the dual class stock structure as a negative since it likely limited the chance of a takeover or other meaningful restructuring. Investors can hold out the faint hope that the Times might eventually decide to cave to shareholder pressure as other family-controlled, publicly traded newspaper companies have recently done. Pulitzer sold out to Lee Enterprises (Charts) last year. And earlier this year, Knight-Ridder agreed to sell itself to McClatchy & Co. (Charts) The Times wouldn't necessarily have to sell to a rival either. Private equity firms The Blackstone Group, Providence Equity Partners Inc. and Kohlberg Kravis Roberts & Co. were considering a bid for Knight-Ridder. And despite all the newspaper industry's woes, publishing is still a relatively stable business that generates a decent amount of cash...just the very thing that private equity firms are looking for. But it's becoming increasingly clear that as the publishing business becomes more challenging over the next few years, only a handful of traditional publishers are likely to survive. Some day, hopefully sooner rather than later for New York Times investors, the controlling shareholders will figure out that it would be better off swallowing family pride and selling out. _____________________ Related: News Corp. buys stake in online jobs site Related: Value investors nibble on newspaper stocks

Related: The Iron Chef stock: Scripps is more than a sleepy publisher |

| |||||||||||||||||