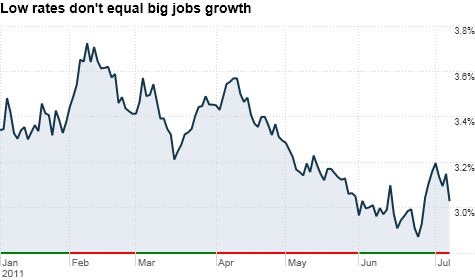

Rates were already low but the yield on the 10 Year Treasury dipped further following Friday's weak jobs report. Click the chart for more on bonds.

NEW YORK (CNNMoney) -- Some readers have criticized me for being a little too negative lately. So in the spirit of Monty Python's "Life of Brian," I am going to do my best to always look on the bright side of life. Here goes.

Want the good news from Friday's jobs report? Interest rates are low! Time to refi now! Hot diggity!

The yield on the U.S. 10 Year Treasury dropped to 3% in late morning trading Friday. It was 3.15% on Thursday.

Yes, even though stocks are down sharply today, investors are again flocking to Treasury bonds. It may seem a bit like perverse logic -- the U.S. economy stinks so buy debt issued by the U.S. government -- but this is what the bond market always does.

Investors scoop up Treasuries at times when the economy seems weak. That pushes their yields -- which move in the opposite direction of bond prices -- lower.

And bond geeks are doing this because today's jobs report proves once and for all that inflation is not a threat and that the Federal Reserve is going to keep short-term rates low (they've been near zero since December 2008) for an even longer time.

"This puts the Fed on hold clearly into 2012," said John Norris, managing director with Oakworth Capital in Birmingham, Ala.

But what today's jobs numbers may not do is give the Fed an excuse to launch another round of bond buying. As I wrote yesterday, the economy isn't in great shape. Still, it would be an overreaction to think we're now double dipping either.

The central bank has already completed two iterations of so-called quantitative easing, a last resort move to help push longer-term interest rates down when short-term rates can't go lower. Still, what purpose would a QE3 program serve?

The economy has many big problems. Prohibitively restrictive monetary policy is not one of them.

"We're nearing a point where the Fed would just be pushing on a string. Yields are already low enough to stimulate the economy," said Matt Toms, head of US public fixed income for ING Investment Management in Atlanta.

QE and QE2 did not create an environment conducive to massive job growth. Why would QE3 be any different?

"If we have another month with a jobs report like this, you may have people pounding the table for the Fed to do something," said Rob Crimmins, fixed income portfolio manager with RS Investments in New York. "But I'm not sure if there is anything more the Fed can do."

Keep in mind that the Fed is also reinvesting proceeds from maturing securities on its balance sheet. That amounts to about another $300 billion or so in Treasury purchases. Norris called that a "shadow QE3." My colleague Chris Isidore has dubbed it QE 2.5.

Either way, it's hard to justify why the Fed should spend even more on bonds. By doing so, it risks alienating big creditors like China, who can't be thrilled to see bond rates falling further on their own, due to weak U.S. jobs numbers.

QE3 could also further weaken the dollar, which would no doubt irritate big trading partners, such as, well, hello again China!

"There is a big risk of diminished returns with more easing from the Fed," said Steve Van Order, fixed income strategist for Calvert Investment Management in Bethesda, Md. "There are many reasons the Fed should now sit on the sidelines. Protracted purchases of debt doesn't get you out of the ditch."

It's also worth remembering that it often takes a while for Fed actions to have a noticeable effect on the economy. QE2 only began last November. It may be premature to declare it a complete, utter failure.

And even if it didn't help stimulate job creation, Toms argues that low rates may have prevented things from getting worse. He said cheap financing is one reason why the commercial real estate market never really blew up as many feared it would.

Finally, the fact that yields are as low as they are may also mean that some of the worst-case fears about the U.S. not being able to raise the debt ceiling by early August are just that: fears.

Yes, I'm really trying to accentuate the positive today. But think about it.

If the bond market was truly worried that the nitwits in D.C. will be unable to stop bickering and actually let the U.S. default on its financial obligations, yields would be much higher than they are now. They might not be Greece, Italy or Portugal high. But a lot higher than 3%.

"I don't think anyone in their right mind thinks the debt ceiling talk is anything more than political posturing. It will get raised. It has to," Norris said.

One can only hope (and pray) that he's right.

Reader comment of the week. I ranted about the Thursday jobs head fake on Twitter this morning with the following bit of bile. "D-mn you $ADP. D-mn you to h e double hockey sticks! 18K jobs added in June. Much much much much lower than expected. Futures plunge."

Loyal Twitter follower Sven Reigle, who goes by @FollowSven (and I suggest you do) concurred. He summed it up thusly this morning.

"Crap!"

Well said, Sven.

The opinions expressed in this commentary are solely those of Paul R. La Monica. Other than Time Warner, the parent of CNNMoney, and Abbott Laboratories, La Monica does not own positions in any individual stocks. ![]()

| Index | Last | Change | % Change |

|---|---|---|---|

| Dow | 32,627.97 | -234.33 | -0.71% |

| Nasdaq | 13,215.24 | 99.07 | 0.76% |

| S&P 500 | 3,913.10 | -2.36 | -0.06% |

| Treasuries | 1.73 | 0.00 | 0.12% |

| Company | Price | Change | % Change |

|---|---|---|---|

| Ford Motor Co | 8.29 | 0.05 | 0.61% |

| Advanced Micro Devic... | 54.59 | 0.70 | 1.30% |

| Cisco Systems Inc | 47.49 | -2.44 | -4.89% |

| General Electric Co | 13.00 | -0.16 | -1.22% |

| Kraft Heinz Co | 27.84 | -2.20 | -7.32% |

| Overnight Avg Rate | Latest | Change | Last Week |

|---|---|---|---|

| 30 yr fixed | 3.80% | 3.88% | |

| 15 yr fixed | 3.20% | 3.23% | |

| 5/1 ARM | 3.84% | 3.88% | |

| 30 yr refi | 3.82% | 3.93% | |

| 15 yr refi | 3.20% | 3.23% |

Today's featured rates: