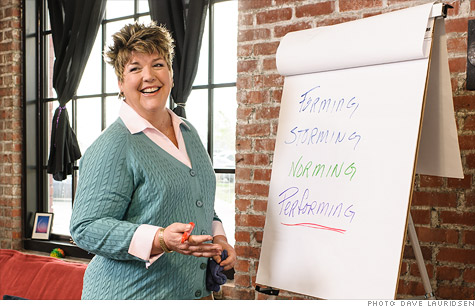

Stephanie Ringer, 51, Louisville, Ky.

(Money Magazine) -- As a regional director for Aflac insurance, Stephanie Ringer had built her Louisville sales team into one of the top in Kentucky. One of her secrets for keeping her staff motivated? Holding brainstorming sessions in a local meeting space called WorkShop. She found that the center -- with its whiteboards, comfy couches, and crazy toys like hula hoops -- fueled productive sessions. So when WorkShop's owners put the business up for sale in 2007, Ringer, then 46, decided to buy it.

Family and friends were surprised at her willingness to take such a risky step at that point in her career. "Everyone said, 'Are you sure this is a good idea?' " she recalls. "But I felt in my gut it was right." With decades of leadership experience behind her, she was sure she could run a successful business.

Five years later Ringer has six employees and nearly $300,000 in annual revenue. While she drew only a $30,000 salary last year, she expects to earn $60,000 this year and clear six figures by 2013. Most important, she loves being the boss -- or, as she calls herself, chief fun officer. "This is the best career move I've ever made," she says.

When you think of today's entrepreneurs, young hot-shots like Facebook's Mark Zuckerberg or Google's Larry Page may be the faces that come to mind. But it's baby boomers like Ringer who are striking out on their own at the fastest clip of any generation.

Americans 55 to 64 have launched more businesses than any other age group during the past decade, closely followed by those 45 to 54, reports the Kauffman Foundation, a nonprofit dedicated to entrepreneurship.

For some, the change has been forced upon them by the tough job market. Others are taking the leap to escape boredom, become their own boss, pursue a passion -- or simply in hopes of hitting it rich.

Whatever the motivation, entrepreneurs face a tough road. Half of businesses fail within the first five years, the U.S. Small Business Administration reports. Some research shows that boomerpreneurs have more staying power than younger folks, but the stakes are also higher: You have little time to recover from failure, you have higher living expenses to cover, you may have a family depending on your income, and though you've likely amassed more wealth, you're closer to the time when you need to tap those assets.

So how can you beat the odds if you want to join the boomerpreneur boom? MONEY put that question to small-business experts and dozens of fiftysomething entrepreneurs for their best advice.

This is the first of three articles on how to become a boomerpreneur. This one will help you to see if you've got what it takes to own your own business and how to put time on your side. You can also get tips for changing your lifestyle, knowing the real costs of starting up a business and financing with caution.

After discovering shops in Europe dedicated to gourmet olive oils and vinegars, Jim Milligan dreamed of opening a similar store with tasting rooms. Then living outside the Twin Cities, he thought such a business would do well in a vacation destination like Traverse City, Mich., where he'd often spent time with his in-laws. Getting laid off at age 55 in 2007 from his position as a general manager at 3M gave him the push he needed.

Those first few years running Fustini's -- named for the Italian word for the stainless-steel containers used to store olive oil -- were harder than he'd expected. Milligan put in 80-hour weeks. "I was on my feet a lot," he says. Between hiring staff, managing inventory, and working the register, he was more mentally and physically taxed than ever before. But, he's quick to add, "it's been incredibly satisfying too."

No matter what field you go into, you'll probably find that owning a business requires more multitasking, risk taking, and stress management than your old job did.

In the beginning, at least, you'll be CEO, secretary, and everything in between -- expect long days on the job and sleepless nights ruminating over what-ifs.

"You have to consider your health, your stamina, your tolerance for risk, and whether this is something you really want to do at this stage of life," says Colorado Springs financial planner Mary Alpers.

Do a self-assessment. "Successful entrepreneurs are calculated-risk takers," says Mary Beth Izard, startup consultant and author of "BoomerPreneurs". Look back on your career to see how well that describes you: Have you set high goals for yourself? Are you fiercely competitive, always looking to what's next? Have you thrived amid uncertainty? Do you enjoy making decisions? Are you quick to adapt? Most important, have you maintained your drive as you've aged?

If you can't say yes to most of those questions, the entrepreneurial life isn't for you. To be fair, not all businesses require the same amount of chutzpah. A freelance graphic designer won't face the same pressures that a restaurateur with high overhead and a big staff does. "You can match a business with your risk tolerance," suggests Izard.

Make sure you're in love. Unless you're 100% enthusiastic about your product or service, you'll resent the time you put in. Passion, on the other hand, can sustain you through long hours and energize you in ways you haven't experienced in years, says Lesa Mitchell, vice president at the Kauffman Foundation.

Should you be forced into entrepreneurship, look for a niche that motivates you. If you're leaving a job, find ways to put your fervor to the test before quitting. Before opening a café, for example, shadow a restaurateur to see whether you'd like it as much as you think. Try out your idea in your spare time before launching it.

PUT TIME ON YOUR SIDE

Marguerite Cole had long wanted to start her own business but figured she'd wait until age 60, when her home would be paid off. When a 2009 restructuring at Microsoft cost her her job as director of sales strategy, however, the then-47-year-old moved up her plan.

With only six months of severance and a monthly mortgage bill, she needed income fast. Since she had lots of contacts, she decided to launch a business-strategy consulting firm. Thanks to low overhead, "I've been able to pay myself a salary every month since starting," says the Redmond, Wash., resident.

Have a question about starting a business? Ask The Help Desk

As Cole was acutely aware, older entrepreneurs don't have the many years a twentysomething has to succeed, let alone recover from failure. So put in legwork to make sure your venture will be among the 50% that survive -- and to ensure that you'll be thriving soon. The average business takes three years to show a profit, the SBA reports. Shoot for under that average so that you don't have to lean too heavily on your savings, says planner Alpers.

Aim for a quick profit. Buying an existing company, as Stephanie Ringer did, will get you up and running faster than starting from scratch. Or aim for a business that's not capital-intensive, à la Cole and the other 5 million boomers who are consultants, according to small-business services provider MBO Partners. Most start up with less than $5,000.

Have a more ambitious idea in mind? Run a break-even analysis -- find help at sba.gov -- to see whether you'll profit within three years.

Do what you know -- or learn before you launch. "If you're starting a business within your area of expertise, the likelihood of success will be higher," says Izard. You'll be able to leverage your network and years of experience.

Going boldly into new territory is especially risky in your fifties. But if you're set on it, familiarize yourself with the field first: Get training, attend conferences, find a mentor. Or bring in a collaborator with the knowledge you lack.

Have a plan B. Even careful planning won't guarantee results. Set a limit now on how long you'll give the venture to meet your projections, based on your resources. Also think about what you'll do if the business doesn't survive. Go back to your old employer? Retire early? Stay connected with former bosses and colleagues in case you need them.

Her strategy: Buy a business that's up and running.

Worked for: Aflac, the insurance company, as a regional director.

Now runs: WorkShop, the Creative Workplace, a corporate meeting space designed to foster innovation.

Quote: "Believe in yourself, but also ask questions of people who have been there and done that."

By the numbers

How to be a boomerpreneur:

Buy a biz that's up and running

Do you know a Money Hero? MONEY magazine is celebrating people, both famous and unsung, who have done extraordinary work to improve others' financial well-being. Nominate your Money Hero. ![]()