|

Preparing for the bears

|

|

May 27, 1998: 3:06 p.m. ET

SEC simplifies prospectuses, but industry says investors know risks

|

NEW YORK (CNNfn) - A string of new rules take effect Monday that force the U.S. fund industry to use "plain English" in prospectuses with easy-to-read information on performance and risk.

The Securities and Exchange Commission drafted uniform guidelines because of nagging fears that bull market investors don't understand the risks of Wall Street.

The changes raise questions about what these starry-eyed investors would do in a bear market -- and whether the fund industry is prepared.

SEC Chairman Arthur Levitt gave the fund industry a "failing grade" for not properly educating shareholders about risks at a May 15 conference of the Investment Company Institute, a Washington, D.C. trade group.

"We are not looking for a bit of window dressing on the same old recycled gobbledygook," Levitt said at the ICI conference. "We expect you to do whatever it takes to speak to investors in a language they understand -- English."

As part of the changes, fund companies must use short sentences and "definite, concrete, everyday words," in prospectuses. The documents mustn't contain any "legal jargon or highly technical business terms." The SEC is also requiring bar charts showing total returns over 10 years, and tables comparing returns to market benchmarks, among other changes.

Fund companies have used arcane, hard-to-understand language in prospectuses because they fear lawsuits, said Roger Kubarych, chief investment officer at Kaufman & Kubarych Advisors, a New York financial advisory firm.

"Companies use language that's worked in the past, so prospectuses become bigger and bigger mountains of words," Kubarych said.

But Kubarych also said prospectuses are complete and elaborate. The problem is investors don't read them.

"The fund industry lobby their own members to improve the clarity of prospectuses," Kubarych said.

The industry insists companies offer vast amounts of information in prospectuses, newsletters and on websites regarding investing risks.

"The fund industry is making sure investors know that nothing grows to the sky," said Chris Wloszczyna, an ICI spokesman. "The party doesn't last forever."

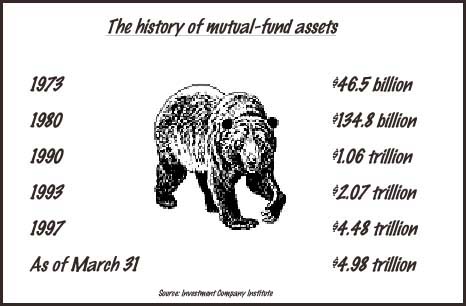

But what happens when the party's over? The question triggers fear throughout the $4.98 trillion fund industry, which hasn't had a major challenge since it became a powerful force on Wall Street over the last five years. One fear is that investors would pull their dollars out of mutual funds.

"It's true the mutual fund industry is more of a bull market phenomenon," said Amy Arnott, an editor at Morningstar Inc., a Chicago fund tracker. "The fund industry has never been tested before."

Arnott thinks the industry hasn't been doing much to prepare for a down market. Most mutual fund portfolios don't hold investments long-term, she said. The average equity fund has an annual turnover rate of 90 percent -- meaning it sells most of its holdings every year. And the average tenure of a fund manager is just three years.

A recent survey shows that the average shareholder expects annual returns of 20 to 30 percent, Arnott said.

But the fund industry said companies have lines of credit with banks in case they get a high number of "redemptions," the term used when investors sell shares. Funds hold an average of 4.6 percent in cash.

Vanguard Group, a Pennsylvania-based fund company, is asking shareholders for approval to allow funds to borrow assets from each other.

One safety valve against a mass exodus is that most Americans have their retirement savings in mutual funds -- either 401(k) plans or IRAs. They're not likely to do anything drastic with a long-term investment, Wloszczyna said.

The fault doesn't lie with prospectuses -- it's that investors hear what they want to hear, said Mike Lipper, president at Lipper Analytical Services, a fund researcher in New York. There's no way to combat unrealistic optimism, he said.

"Every person who goes to college thinks they're going to graduate, and every person who gets up in the morning thinks they're going to live through the day," Lipper said. Likewise, most investors these days assume they'll make money.

Kubarych said one issue is whether the next downturn comes dramatically or gradually. If there's a sharp market drop, investors might move their money out of aggressive stock funds and into safer money market and bond funds. Investors who lose everything might switch to bank CDs. Then they'll call their lawyers.

"There's no doubt about it there will be a lot of lawsuits (in a down market)," Kubarych said. "The industry is well aware that there will be a rash of class-action lawsuits."

History has some clues about what may lie ahead, but no real answers.

U.S. funds suffered in 1973 when inflation soared and gas shortages led to long lines at the pumps. Many U.S. funds had years of net redemptions until about 1980, said Henry Hopkins, chief legal counsel at T. Rowe Price, a Maryland-based mutual fund company.

"We learned to live in that environment," Hopkins said. Fund companies survived by keeping higher levels of cash reserves.

But Kubarych argued that the 1970s were much more turbulent. Today, inflation and unemployment are at record lows and the economy seems unstoppable. The political climate is more stable than ever.

Plus, the U.S. fund industry in 1973 was relatively tiny, with just $46.5 billion in assets. Assets in funds didn't top the trillion market until 1990 and have climbed ever since.

One reassurance for the industry is that investors generally haven't panicked during previous market blips, said Hopkins.

"By and large, investors have been very wise," Hopkins said. When the Dow Jones industrial average dropped 550 points in October 1997, investors showed "patience and wisdom," and the market rebounded.

Perhaps the closest comparison is Japan, whose economy seemed just as miraculous in the late 1980s when the Nikkei danced at 39,000. The country's fund industry, while tiny, saw massive losses when the Nikkei dropped to a low of 14,000 in 1989. These days, most Japanese keep their money in post office accounts. The Tokyo benchmark closed Wednesday at about 15,664.

Arguably, it's impossible to compare America of 1998 with Japan of 1988. Japan's economy was highly leveraged, with businesses issuing stock to each other at crazy prices, said Jeff Uscher, editor of Grant's Asia Observer. But the Japanese never imagined a downside, either.

"The risky investing behavior by individuals here is much worse than it ever was in Japan," Uscher said.

American investors have watched the bloodletting in Asian markets with a mixture of horror and denial. Most U.S. mutual-fund investors can't imagine losing 30 or 40 percent in their mutual funds, said John Moon, managing partner at Moon Capital, an investment management firm in New York. But it could easily happen, he said.

"It's beyond people's belief," Moon said. "But I think it's very likely to happen."

-- by staff writer Martine Costello

|

|

|

|

|

|

|

{kind=link}