|

Bonds refuse jobs balm

|

|

June 4, 1999: 3:41 p.m. ET

Choppy day ends with yields rising again as traders turn away from payrolls data

By Staff Writer Robert Scott Martin

|

NEW YORK (CNNfn) - U.S. bond yields drifted back their 2-month high-water mark Friday after a long-awaited employment report proved unable to sustain a weak morning rally among investors steeled to expect bad news.

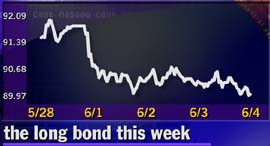

Shortly before 3 p.m. ET, the benchmark 30-year Treasury bond slipped 5/32 of a point in price to 90-2/32, pushing the yield up to 5.96 percent.

Trading was choppy as investors struggled throughout the day to put the May employment report into context, eventually failing to find fresh incentive for buying in the overall implication that while the labor market remains tight, it is not oppressively so.

Bill Sullivan, money market economist at Morgan Stanley, called the data "inconclusive" as a strong hourly wages component clashed with a dramatic slowdown in job growth. He said the report "doesn't tell us anything" about what the Federal Reserve will do when it next meets to set U.S. interest rate policy June 29 and 30.

The report showed that the U.S. economy added only 11,000 jobs in the month, a profound downturn from expectations of 216,000 and a profound relief for bond traders steeled for the worst.

When the economy is creating a large number of new jobs, workers find it easier to demand higher compensation from the employers who compete for qualified help. This naturally leads to rising wage inflation, which the Federal Reserve is known to watch with a hawkish eye as the most likely harbinger of broader inflationary pressures.

However, the April figure was upwardly revised to 343,000 from 234,000, providing only narrow comfort to investors eager to see a firm trend of slowing job growth.

As such, the implication that April's growth was far stronger than previously suspected, while May's job market was conversely looser than expected, offered only limited comfort to the jittery bond market.

"We're slowly leaking," said Theodore Ake, Everen Securities bond analyst. The market still harbored "a lot of fear" which contributed to the overall bearish tone, he added.

The hourly earnings component of the report was more decisively negative for bonds. Average hourly earnings climbed 0.4 percent, or 5 cents, a slight but significant surprise for investors who were prepared to see the figure rise 0.3 percent from last month's 0.2 percent rise.

As a direct indicator of wage inflation, the earnings statistic is an especially valuable window into Fed policy, particularly in an investment climate in which many traders expect the Fed to raise interest rates in the near term.

Picking up the pieces

The afternoon's losses brought the long bond's decline for the week to 1-3/4 points in price, or $17.50 per $1,000 bond. The yield edged up 13 basis points.

Moving forward, Bill Sullivan from Morgan Stanley expected to see "waves of selling and buying" in the bond market throughout the day as investors wrestle with the data.

However, the market's emphasis will now likely shift to the May producer price index (PPI) as a more comprehensive picture of inflationary forces at work in the economy. The report, due June 11, is the last PPI reading the Fed's rate-setting Open Market Committee (FOMC) will consider in its next meeting.

Because Fed Vice-Chairwoman Alice Rivlin was known to be a rate "dove," favoring lower rates, Sullivan doubted that her resignation would have much effect on the bond market. Rivlin won't attend the June FOMC meeting.

Bonds are especially sensitive to interest rate shifts because rising rates depress the fixed returns Treasury debt offers, making them a less tempting investment than cash.

Although bond yields have edged up in recent sessions to near the ominous 6 percent level, some analysts remain unconvinced that the market has adequately braced for the prospect of higher rates ahead.

"I almost thought that a quarter-point rise in rates was priced into the market," said Brian Finnerty, head of Nasdaq trading at C.E. Unterberg Towbin. "But I think it depends on how the Fed says it or what they do because if it's the first in a series of hikes the market is going to get slammed hard."

The Federal Reserve spooked financial markets in mid-May by announcing that it will now lean toward raising rates, ensuring the near-inevitability of at least one rate hike on the horizon.

Dollar exerts mild pressure

Currency markets exhibited a customarily cool reaction to the employment report as traders discounted the news as ambivalent and, hence, less important to Fed policy than the upcoming CPI.

The dollar edged up to 122.19 yen, continuing its meandering course against the Japanese currency. However, the euro offered firm resistance, rising more than a cent from a fresh lifetime low of $1.027 hit in European trading to trade at $1.0371.

Although the European currency's decline would have been almost unimaginable when it was launched five months ago, an increasing number of traders looked to the euro to hit parity with the dollar in the near term.

A conspiracy of factors have kept the euro on its knees. The prospect of widening war on Europe's Balkan borders now seems unlikely, but uncertainty from that direction continues to give traders a handy hook on which to hang bearish sentiments.

More deeply, the euro labors under an unflattering comparison between the sluggish European economy and unexpectedly sustained expansion in the United States. While the climate for U.S. interest rates, which measure the cost of dealing with dollars, now encourages the dollar to rise with rates, European traders still look toward an interest rate cut in the near future.

"Not at all concerned"

Finally, currency markets increasingly see the euro as something of an orphan, abandoned by its political and monetary masters. Although some European officials, notably from Germany's Bundesbank, have weighed in with support for the struggling euro, the European Central Bank has been alternately cheerful and silent as the currency loses ground.

On Friday, this policy of nonsupport was highlighted by reports that the European Council only narrowly omitted an official statement of unconcern from a recent press release.

Although the final draft of the document did not include the phrase "not at all concerned by the current development in the euro's foreign exchange rate," the notion that Europe's leadership had even contemplated such a gesture of indifference disturbed euro bulls and gave succor to euro bears.

|

|

|

|

|

|

|