|

Playing the 401(k) game

|

|

August 12, 1999: 10:57 a.m. ET

Borrowing against retirement funds can pay, but you also can get burned

By Staff Writer Shelly K. Schwartz

|

NEW YORK (CNNfn) - Planning for retirement is challenging enough, and borrowing against your 401(k) plan complicates matters. The experts say it could make sense, but they advise caution since a 401(k) loan could end up costing you a bundle.

Some experts say 401(k) retirement accounts -- popular with Americans since they allow pretax contributions and defer taxes on the funds in the account until retirement -- were never intended to act as loan pools. These critics say that if you borrow from your account, you may end up seriously short-changing yourself in the end.

But others say loan provisions in employer-sponsored 401(k) plans encourage workers to save more -- and they point to a congressional study that reached a similar conclusion. They say "k-plan loans" are a good option for people strapped for cash who otherwise would be stuck paying the exorbitant interest rates sometimes charged by banks and other creditors.

So what's an investor to do?

As a general rule of thumb, Dallas Salisbury, president of the Employee Benefit Research Institute (EBRI), said 401(k) loans should be viewed as a last resort.

"Generally, you are going to be better off finding other places to borrow money so you stay invested and you benefit from diversified compounded returns," he said.

In certain situations, however, especially in an emergency, Salisbury said, investors may be better off borrowing from their own retirement plans than from a high-interest lender.

"It's better to borrow money from yourself than to take an outright withdrawal and never pay it back or to borrow from a bank or credit card company" if you fail to qualify for low-interest loans, he said.

Those who do it, however, should be prepared to pay back that loan on time. They also should be aware of the penalties, potential tax liabilities and drawbacks that such a scenario can derive.

Simple in theory, but complex in fact

The 401(k) loan is simple in theory.

You borrow against the money you've already set aside in your retirement account. By law, the maximum you can borrow is $50,000, or half your vested account balance, whichever is less.

Most 401(k) loans must be repaid within five years with interest. But loans for buying real estate can be longer-term.

Most but not all employers that offer 401(k) plans to employees include some type of loan provision. About 20 percent of plan sponsors do not. And some restrict loans against the 401(k) to medical emergencies and the like.

For those employers with plans that do make loans, the Internal Revenue Service requires that they charge borrowers fair-market interest rates. But rates can vary widely.

Today, most plan sponsors charge between 8 percent and 10 percent interest rates on 401(k) plan loans, industry experts say. That compares with the 12 percent to 20 percent that banks and credit card companies would charge.

One good thing about borrowing from your 401(k) is that you pay the money, with interest, back to yourself.

"If it's money that an individual would otherwise have to borrow, meaning they'd take out a loan against a credit card or run up a balance, they are better off economically if they borrow from themselves," Salisbury said.

Jeffrey Levine, a certified financial planner at Linsco/Private Ledger in Albany, N.Y., said 401(k) loans are much easier to secure and typically less costly than any other type of loan.

Employers rarely require you to undergo a background or credit check, since the other half of your 401(k) investment, which you cannot touch under the law, serves as collateral.

Most often, your employer simply docks your paycheck as you repay your loan.

As for fees, Debbie DeWall, senior vice president and director of plan consulting at The 401(k) Company in Austin, Texas, said you'll likely pay $20 to $25 a year to maintain the loan, plus a one-time fee of about $50.

There is a downside

There is a downside to 401(k) loans.

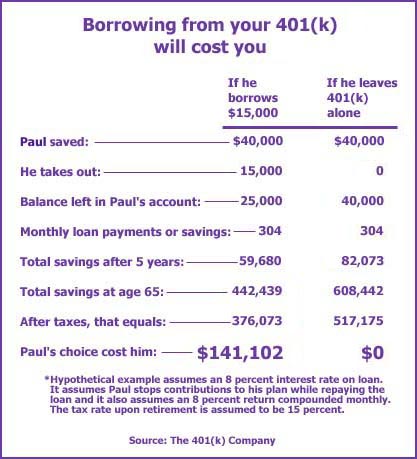

Consider Paul, a hypothetical 35-year old investor who borrowed $15,000 of the $40,000 in his 401(k) plan. Since he didn't contribute to the plan for five years while paying back the loan, he lost the returns that he otherwise would have received on those contributions.

Had he not borrowed and continued contributing during those years, he would be able to withdraw $517,175, according to calculations by The 401(k) Company, using an 8 percent return and a 15 percent tax rate upon retirement.

But because of the loan, the funds he would have after withdrawal would be just $376,073, using the same assumptions. That low-interest loan cost him $141,102.

(Click here for a hypothetical chart showing how much a 401(k) can cost you long-term)

"If you need money, 401(k) loans are an attractive way to borrow because you are paying yourself back vs. paying somebody else back," Levine said. "But you have to be very careful in evaluating it, because in a bull market like we're in, where 401(k) funds are doing very well, you are taking out money that potentially could be growing substantially."

Double taxation also an issue

Then there's Uncle Sam to contend with.

In a 401(k) loan, you borrow dollars that were contributed before taxes and paying them back, plus interest, with after-tax income. Then, when you cash out of your plan upon retirement, you'll be taxed on that money again.

That's what experts call "double taxation."

"That's something that a lot of participants don't think about," DeWall said. "They are less expensive in interest rate fees than banks, but you are also short-changing yourself on [taxes]."

Also, the IRS does not look kindly upon those who take out a fixed-term loan against their pretax retirement account and fail to pay it back.

In fact, the Internal Revenue Service views an overdue 401(k) loan as a taxable distribution, or an outright withdrawal, taxable as regular income.

In addition, if you're under 59-1/2, you'll be assessed an early withdrawal penalty equal to 10 percent of the outstanding balance.

You may end up dipping further into what's left of your 401(k) plan to pay it back. That will get you out of trouble with the IRS, but it won't do your account balance any good come retirement day.

Lastly, if you do borrow from your 401(k), make sure your employment status is secure.

Salisbury of EBRI said that's because investors who take out a 401(k) loan and later quit or get fired from their job are required to pay back the amount of the loan outstanding, usually within 30 to 60 days.

"You could very readily have a situation where if you've used a 401(k) plan as a source of emergency capital and you lose your job, you could end up even deeper in debt," he said.

Loan provisions encourage saving

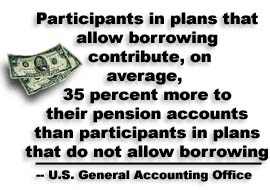

Despite the potential drawbacks of 401(k) loans, a study released by the General Accounting Office in October 1997 found that employees are more likely to participate in voluntary 410(k) plans when they are allowed to borrow from them.

Participants in plans that allow borrowing also tend to contribute more to their 401(k) -- on average 35 percent more, according to the study by the GAO, the accounting arm of Congress.

Those who most often borrow against their 401(k) plans include African Americans, Hispanics, lower-income persons, those who have recently been turned down for a loan, and workers who are also covered by other pension plans, the study found.

|

|

|

|

|

|

|

{kind=link}