|

Pragmatism and prenups

|

|

May 6, 2000: 8:00 a.m. ET

With divorce on the rise, prenuptial agreements are gaining popularity

By Staff Writer Shelly K. Schwartz

|

NEW YORK (CNNfn) - Mention the words "prenup agreement" at your next social gathering and you'd best be prepared to go eight rounds.

Few topics in modern-day America inspire such swift fury -- even from those who aren't directly involved. After all, asking your betrothed to sign a contract that limits his or her rights to your assets flies in the face of romance. It implies you don't have faith in the relationship. And that you care more about your bank account than your soon-to-be spouse.�

Doesn't it?

Not necessarily, said Miriam E. Mason, president of the American Academy of Matrimonial Lawyers.�

Prenuptial agreements, she said, are beginning to shed their one-time reputation as cold-hearted relationship killers and are, in fact, fast becoming the financial planning tool of choice for middle-aged Americans heading back down the aisle for the second or third time.

"I still think people have a stereotyped view of prenup agreements; that they  say let me have everything and you get nothing," Mason said. "Certainly those kinds of contracts still exist, but are these good solid relationships? Don't believe it." say let me have everything and you get nothing," Mason said. "Certainly those kinds of contracts still exist, but are these good solid relationships? Don't believe it."

Mason, a long-time family law attorney, said prenups today serve a much different purpose. They establish a dividing line of sorts between the hard-earned assets each party brings into the marriage and those they will share jointly after the vows are exchanged.

"More and more people are divorcing and marrying a second time and they [set these contracts up] because they don't want to make the same mistakes over and over again," Mason said. "They really want it to last, and both parties are usually far more open to doing all they can to [create a dispute-free] relationship."�

Perhaps most important, however, such contracts provide financial security for the children being thrown into a new family unit.��

Click here for CNNfn's top personal finance features of the week

Stars come out for stocks - May 5, 2000

How to retire comfortably - May 5, 2000

Some hedge funds prevail - May 4, 2000

Venture funding soars - May 4, 2000

ClubFixit - Diary of a startup - May 3, 2000

Gen Xer crushed by debt - May 1, 2000

Divorce insurance

Prenuptial agreements are legally binding contracts that spell out who owns what going into the marriage and who will own what in the even of a death or divorce.

As the name would suggest, prenuptial agreements are created before the couple says "I do." Contracts created after the wedding day - which are far less common - are called postnuptial.

The rules that govern such agreements differ slightly from state to state, but virtually all stipulate that in order for such a contract to be binding there must be full and fair disclosure of all assets by both parties. Both parties also must have legal representation and the document cannot be punitive on its face. That means the contract can't be designed to penalize the "non-wealth" spouse.�

"Basically, it resolves all of the issues in advance that would normally be resolved in a divorce case," said George Stern, an Atlanta-based family law attorney of 36 years.

Depending on legal fees and the complexity of assets being declared, they can cost anywhere from a few thousand dollars to $25,000 to arrange.

But with divorce rates where they are today, experts say that can be a small price to pay for peace of mind.

"It's a form of protection," said Michael Viola, a divorce lawyer with Shainberg & Viola in Philadelphia. "You have health insurance in the event something should happen to you physically. Think of this as divorce insurance."�

In some states, failure to create such a document could cost you up to half of your holdings - even if your marriage lasts only a few months or years.

The U.S. Census Bureau reports that 19.4 million adults were divorced in 1998 - the most recent year for which data are available.

"In the past, the only people who really needed prenups were the very rich and those entering into a second or third marriage; or widows and widowers trying to preserve their estates for their children and grandchildren," Stern said. "But in the last five years, with the economy changing and everyone making all this money on the Internet, prenups got to be really big time in that even first marriage spouses are looking to preserve the assets they are bringing into the marriage."

Stern estimates 10 percent to15 percent of altar-bound Americans enter into these types of arrangements each year - mostly those who have accumulated or inherited significant wealth of a million dollars or more.

Interference from the sidelines

Interestingly, however, Stern noted it's not just the brides and grooms-to-be pushing for financial protection. In many cases, he said, it's their parents.

"I've done more of these in the last two years than I had done since I started in this business," he said. "What happens is the parents have accumulated large sums of money in real estate, or in initial public stock offerings and they've put much of it in their children's names through trusts. They then insist that their child's fianc� enter into a prenup with their child."

Sound like something out of "Mommy Dearest?" To most of us, maybe. But to hard-working baby boomers who wish to ensure that their money be divided among their children and grandchildren, it's a little less callous than it sounds. It's nothing more than a basic estate planning tool.

"This is a new look at things," he said, noting the ultimatum may not be directly communicated but "the innuendo" is that the son or daughter won't receive the assets at all if they insist on getting married without the prenup.

The alternative

It doesn't happen often, but in certain cases where a prenup is in place the divorce court judge will overturn that document and rule in favor of the "non-wealth spouse." This happens most often to the very wealthy, where one spouse (usually the wife) receives virtually no division of assets upon the divorce.

Consider the break-up of real estate mogul Donald Trump and ex-wife Ivana. The latter walked away with more than $50 million in a settlement after Trump's highly publicized affair with beauty queen Marla Maples. Under terms of the original agreement, she would not have been entitled to Trump's funds.

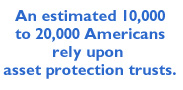

Enter: Asset protection trusts.

These little-known tools allow individuals to transfer ownership of all their  assets - including real estate, stocks and savings - into a trust account that is held overseas. The assets themselves remain unchanged and you would then designate yourself as the trustee. assets - including real estate, stocks and savings - into a trust account that is held overseas. The assets themselves remain unchanged and you would then designate yourself as the trustee.

Rob Lambert, president of the Asset Protection Corp. in Manhattan, said the beauty of these trusts is that they allow the trustee to name as a primary beneficiary anyone they like - including their spouse. In the event of your death or disability, the spouse takes on ownership of those assets.

"This way you get to name your spouse as the beneficiary," said Lambert, who estimates between 10,000 and 20,000 Americans have set up these types of trusts. "You have something in writing that shows you believe in the marriage."�

Better yet, (depending on your perspective) you retain the right as the trustee to remove your spouse as the beneficiary anytime you choose. If the marriage remains on course, your spouse keeps the beneficiary status. But if it starts to crumble, you can always change your mind.

"Prenuptial agreements destroy trust in a relationship," Lambert said. "It's not romantic and it can leave the marriage bed very cold. But these trusts ensure that you are protected in the eventuality of a divorce and they allow you to name your fianc� as the beneficiary while the marriage is going well."

Such trusts, he noted, are virtually tamper proof once created. That's because the trusts are set up in other countries, including England and France, rendering the assets untouchable by U.S. divorce courts.

It will not, however, render those assets untouchable by the Internal Revenue Service.

"Anyone who tells you that offshore trusts are a way to hide your assets from the tax man is telling you to commit a crime," Lambert said. "If you are a U.S. citizen, you are taxed on your assets worldwide. These trusts won't save you any taxes at all."�

They won't save you any money upfront either. Asset protection trusts cost anywhere from $15,000 to $25,000 to set up. They are therefore only advised for the very rich.

"Most people who set these up have several million dollars to protect," Lambert said. "But would I spend $20,000 to protect $500,000 that I've worked 10 years to build? Sure."

|

|

|

|

|

|

|