|

Biweekly mortgage plans

|

|

May 15, 2000: 9:11 a.m. ET

Paying your loan twice a month can save big bucks, but is it right for you?

By Staff Writer Shelly K. Schwartz

|

NEW YORK (CNNfn) - The sales pitch is nothing if not enticing.

Simply set up a biweekly payment plan and save tens of thousands of dollars on your mortgage, build equity in your home more quickly, and shave up to 10 years off the life of your loan -- all without increasing your monthly bills.�

Proponents say the benefits of such plans, in which borrowers make mortgage payments twice a month instead of once, are unparalleled. You say it sounds too good to be true.

As is often the case, the truth lies somewhere in between.

"You really can save an enormous amount of money making biweekly payments," said Robert Irwin, a long-time real estate broker and author of the book, "Tips & Traps When Mortgage Hunting."� "Over the long haul, you can save 30 percent to 40 percent on interest payments."

But Irwin and other experts agree that the much-vaunted biweekly mortgage plan isn't right for everyone. And they say there are more flexible alternatives that can do the trick just as well.

Is it right for you?

Biweekly mortgages, also called accelerated equity plans, are fairly simple. Rather than making, say, a $1,000 mortgage payment at the end of each month, you'd pay the bank $500 every two weeks.

Doesn't sound any different, you say? Oh, but it is.

By paying on a monthly basis, you end up making 12 mortgage payments over the course of a year. But due to the odd number of days in certain months, there are actually 52 weeks in the year. (That's why those of you who are paid every other week end up with two extra paychecks a year.)

Therefore, paying your mortgage every two weeks results in 26 payments per year. That's equivalent to making two extra biweekly payments - or one full  mortgage payment - per year. mortgage payment - per year.

That payment then gets applied to your principal, which reduces the number of years you pay your mortgage and therefore the amount of interest you owe.

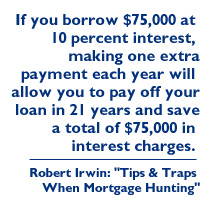

Here's an example, from Irwin's book: If you borrow $75,000 at 10 percent interest, making one extra payment each year will allow you to pay off your loan in 21 years and save a total of $75,000 in interest charges over that term.

Irwin said it all comes down to interest.

"In the early years of your mortgage, nearly 100 percent of your payments are applied to interest," Irwin said, noting that payments gradually begin to apply more to your principal than the interest as the years go by. "Whenever you increase your principal, you change the mathematics entirely."

As such, he said, consumers may be surprised to learn that by making one extra mortgage payment in the first year that goes entirely toward principal can reduce the time it takes to pay back the loan by over a year and reduce the interest paid over the term of the mortgage by more than $10,000.

Bob Van Order, chief economist for Freddie Mac, a federally chartered mortgage finance corporation, agrees that biweekly plans can yield big benefits. But he notes consumers should not view them as a freebie.

"The advantage of biweekly payments is one of convenience, not that you're getting something for nothing," he said. "It's true that if you pay off a loan sooner you do indeed pay less interest. But you are still paying out more money each year than you would if you paid once a month. People need to know that they are not getting something for nothing here."

What works for you?

To be sure, bi-weekly plans aren't for everyone.

Teachers, military workers, and others who are paid once a month may find it tough to manage their money if they lock themselves into paying their bills every 15 days.

Same goes for the self-employed, many of whom can't safely estimate their cash flow status two months in advance, let alone 20 years down the road.

"If you are on a salary and you're paid every two weeks, this is logical," Irwin said. "But it's not a good idea if you work for yourself or of if get a pay check once a month, because as soon as that money comes in you're ready to spend it. Also, it is more money out of your pocket and it's something else you have to think about. You have to remember to send in 26 payments instead of 12."

That takes discipline. After all, you don't want to forget or fall behind on your mortgage payment. Just a few can leave a permanent black mark on your credit history. You could avoid that problem by asking your bank to automatically withdraw your payment from a designate checking or savings account every two weeks. �

The benefits of the biweekly plan don't show up immediately. It's a long-term money-saving strategy. As such, experts say, it's best suited for those who plan to remain in their home for at least eight to ten years.

Van Order named one other group that is ill-suited for a biweekly mortgage: "If you are living paycheck to paycheck, you may find that difficult. Sure, you can make provisions for that and save ahead. But you can also just pay monthly as you already do and just add a bit more principal."

That leads us to alternatives.

As Van Order suggested, you can set up your own accelerated payment plan by maintaining your existing monthly mortgage and adding a little extra to each bill. A good way to do that is to take your monthly bill, divide it by 12 -- and add that amount to your check. At the end of the year, you will have made one extra mortgage payment.

You can also simply set aside that extra amount each month in your savings account, Irwin said. At the end of the year, you can send in the extra payment to your lender.�

And, you can set up a biweekly payment plan with your bank on your own. Some banks allow it; others do not. Those that do generally charge a small fee.

Both practices will produce the same effect as the biweekly plan by lowering the life of the loan, significantly reducing your interest owed and building up your equity faster. Unlike the biweekly plan, however, it will also grant you the flexibility to return to your regular monthly payments if you lose your job or become ill.

If you create your own accelerated mortgage plan, be sure you instruct the bank to apply that extra money to the principal, which will have the same effect of reducing the life of your loan, trimming interest payments and building equity faster. Otherwise, the bank may just consider it an early mortgage payment and apply it to interest.

Also, Irwin suggests you verify with your bank in advance to ensure your loan does not come with a prepayment penalty. Most banks these days, he notes, allow prepayment without penalties -- but it never hurts to ask.�

Another option is to take out a 15-year loan. These loans also reduce significantly the amount of interest you will pay, since they are paid off in half the time and because you can secure a lower rate with the banks. Another option is to take out a 15-year loan. These loans also reduce significantly the amount of interest you will pay, since they are paid off in half the time and because you can secure a lower rate with the banks.

As you might expect, they also result in higher monthly mortgage bills, but probably not as much as you think.

In his book, Irwin points out that on any mortgage, the monthly payments only go up by 15 percent when you cut the term in half. His book also reveals how much can be saved in interest by using the 15-year loan rather than a 30-year.

On a $100,000 loan at 12 percent (not uncommon for subprime borrowers), for example, you would pay $270,016 in interest over 30 years. Interest on a 15-year mortgage, using the same terms, amounts to $116,032. That's a savings of $153,984.��

"This is something you can easily set up yourself," Irwin said. "The worst things are these services that charge you $400-to-$500 to set them up for you. It's outrageous."

Brokers, however, disagree.

Shelly Lambert, branch manager for mortgage broker Home Port Mortgage of Port Orchard, Wash., said in many cases, consumers don't have a choice.

"Most banks don't even offer these plans," she said. "By setting up a biweekly payment plan through a third party administrator, rather than a true biweekly mortgage which is arranged directly between the consumer and the lender, you get the same results. We handle all of your payments for you so you don't have to think about it. And say you get into financial trouble; this way you are not locked into biweekly payments. You can stop and resume when you like."

Moreover, she said, the plan follows your mortgage wherever it goes.

"Sometimes you'll run into problems where the consumer sets up a biweekly plan with their lender, they pay a small fee to do it, and then the lender turns around and sells the mortgage," Lambert said, noting she charges clients $195 to set up a biweekly contract. "The new owner of that mortgage only bought the original terms, not the biweekly plan. It doesn't always transfer."�

|

|

|

|

|

|

|