|

Secrets to retiring rich

|

|

May 19, 2000: 6:43 p.m. ET

Pssst. Want to be a millionaire by 40? Then follow these tips from pros

By Staff Writer Martine Costello

|

NEW YORK (CNNfn) - So you really are all about money. You like fast cars, luxury hotels, and Italian shoes. You want Oriental rugs in every room and a place in Florida. You want a maid to make your lunch.

And, since you're one of those people who understands the finer things in life, you want to stop working while you're still young enough to appreciate it.

But it isn't easy to save millions by the time you're 40 - or everybody would be doing it.�

Don't hate yourself for being in love with money - just hate yourself if you don't follow the tips of investing pros.

"Tip number one is you have to start saving immediately," said James O'Shaughnessy, founder of O'Shaughnessy Funds and author of "How to Retire Rich."� "The younger you are when you start, the better chance of retiring in style." "Tip number one is you have to start saving immediately," said James O'Shaughnessy, founder of O'Shaughnessy Funds and author of "How to Retire Rich."� "The younger you are when you start, the better chance of retiring in style."

Many people don't realize the enormous power of compound interest when they start saving young, said Frank Armstrong, a certified financial planner and president of Managed Account Services. He is also author of "Investment Strategies for the 21st Century."

"Suppose the day you're born, your parents put $1,000 away a year for you until your 10th birthday," Armstrong said. "At this point, your parents stop making contributions. The fund continues to earn 10 percent net, and you are able to resist the overwhelming urge to cash it in for a new Corvette when you reach 21. The fund grows to $3,013,115.83 over the next 55 years."

Compounding is so important that if you save $2,000 a year starting at 20 until you're 30, you'll still have more money than a person who saved the same amount between ages 30 and 60, he said.

The easiest way to get started saving is through your company 401(k), O'Shaughnessy said. Put in the maximum allowed - the limit is $10,500 annually or 15 percent of your salary - as soon as possible. The money grows tax-deferred, and your employer will often match a certain percentage. The easiest way to get started saving is through your company 401(k), O'Shaughnessy said. Put in the maximum allowed - the limit is $10,500 annually or 15 percent of your salary - as soon as possible. The money grows tax-deferred, and your employer will often match a certain percentage.

"If you have a 401(k) at work and you don't use it, it's like literally walking by buckets of money every day," O'Shaughnessy said. (Click here for some good 401(k) funds).

Click here for CNNfn.com's top personal finance stories for the week.

Best catchup strategies

Biweekly mortgage plans

Countdown to retirement

The 25 best tech stocks

The artful investor

Wild market, winning funds

Betting the farm on stocks

The next step is to open an IRA. You can qualify for a Roth IRA if your adjusted gross income is $150,000 or less for couples or $95,000 for a single person. You can't deduct the contributions as you can with a traditional IRA, but the money grows tax-free and you can withdraw it tax-free at age 59-1/2.

Automatic payroll deductions into a mutual fund account are another good way to set money aside. If the money goes straight into an investing account, chances are you'll never even miss it. Automatic payroll deductions into a mutual fund account are another good way to set money aside. If the money goes straight into an investing account, chances are you'll never even miss it.

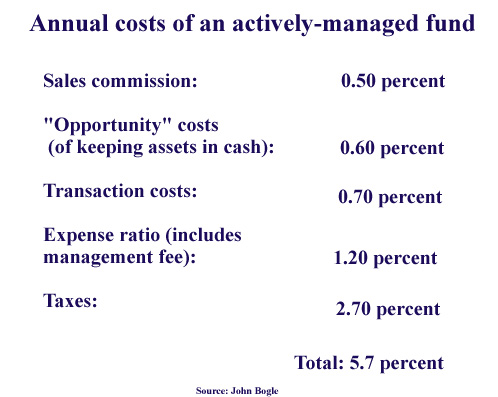

Armstrong recommends index funds because the costs are much lower than actively-managed funds. (Click here for more on the differences between actively-managed funds and index funds).

"Lower costs will give you higher net returns," Armstrong said. "I think cost is critically important."

Check your mutual funds, and read the latest fund news on CNNfn.com.

But how much will you need, you wonder? Because of increasing life expectancies and the impact of inflation, you'll need a lot more than you think, said Charles Hamowy, a senior financial adviser at American Express Financial Advisors in New York. But how much will you need, you wonder? Because of increasing life expectancies and the impact of inflation, you'll need a lot more than you think, said Charles Hamowy, a senior financial adviser at American Express Financial Advisors in New York.

"The good news is people are living longer, and the bad news is people are living longer," Hamowy said.

There's a good chance that people born today will live well into their 90s or even past 100. That means you may spend more time retired as you do working.

If you need $1 million today, you'll need $5 million in 30 years because of inflation, Hamowy said. At a 4 percent rate of inflation, costs double every 18 years, he said.

Someone who is 30 years old today will probably need $3 million to $4 million in 30 years - possibly as much as $5 million, Hamowy said. Someone who is 30 years old today will probably need $3 million to $4 million in 30 years - possibly as much as $5 million, Hamowy said.

People are also doing more in retirement these days - they're traveling, starting new hobbies, and building vacation homes. But having big dreams means you'll need more cash to make them come true.

"I know a lot of people in their 40s now who can retire if they want to," Hamowy said.

Many experts say you'll have to save 15 percent to 20 percent of your annual salary every year if you really want to retire comfortably. Many experts say you'll have to save 15 percent to 20 percent of your annual salary every year if you really want to retire comfortably.

"Stuff every penny away that you can," Armstrong said. If you think 20 percent is a lot, you'll look back years later and see missed opportunities, he said.

If you're not sure how much money you'll need, try using online retirement planning calculators to get started, O'Shaughnessy said. Try a couple of them to get different opinions.

"I tell people to design their ideal life. What do you want to do? What do you want to be?" O'Shaughnessy said. "Sit down, add up your expenses, write out your life."

A good long-term investing plan is crucial to retiring young rich - and you have to stick with it, he said. Don't be swayed by other optional expenses that come up in life. A good long-term investing plan is crucial to retiring young rich - and you have to stick with it, he said. Don't be swayed by other optional expenses that come up in life.

"You have to pay yourself first," O'Shaughnessy said. "You can't let other things get in the way."

Put your money in the stock market and don't worry about the volatility, O'Shaughnessy said. It won't matter in 30 years. Don't panic and be swayed into selling when the market falls.

"Investing in the stock market is the only way you're going to get rich over time," Oshaughnessy said. "One thing I tell people is I can guarantee them that on their road to retiring rich they're going to panic. But the only way to turn a temporary loss into a permanent one is to panic and sell."

In fact, anybody who wants to retire young and rich might want to hope for a bear market, Armstrong said. After all, they'll be able to invest in good stocks selling at a big discount. In fact, anybody who wants to retire young and rich might want to hope for a bear market, Armstrong said. After all, they'll be able to invest in good stocks selling at a big discount.

"You're buying stocks on sale," Armstrong said. "There's never been a market that didn't recover."

|

|

|

|

|

|

|

{kind=link}

{kind=link}