NEW YORK (CNN/Money) -

For Mari Frank, an attorney in Orange County, Calif., the nightmare began with a phone call in August of 1996.

"The Bank of New York in Delaware called to ask why I had not paid my $11,000 credit card bill," Frank said. "I didn't have a credit card from that bank, and I certainly hadn't charged $11,000. No one had stolen my wallet, and I had always been careful with confidential documents. I just kept asking -- how could this have happened?"

Frank was the victim of identity theft, a crime in which someone uses your personal information to access your accounts and good credit, then rips you off.

"The police searched the thief's mailing address, and found billing statements in my name from various creditors, letters from collection agencies, a letter from a rental car company threatening to sue for damages to a vehicle she'd rented, checks, and my own business cards that she'd taken from my office," Frank said.

All told, the woman who stole her identity had spent about $50,000, including charges on several high-limit credit cards and the purchase of a red Mustang convertible.

In the wrong hands

Unfortunately, stories like this are not uncommon.

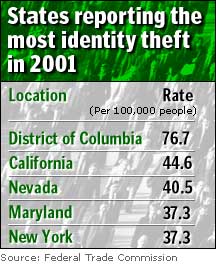

In fact, identity theft was the fastest growing crime in the U.S. last year, according to the Federal Trade Commission. And some experts estimate that as many as 1.1 million people were victimized last year.

"Identity theft is a huge problem, and every number and indicator shows that it's on the rise," said Edmund Mierzwinski, a consumer advocate at the U.S. Public Interest Research Group. "This is not a question of six degrees of separation -- everybody knows somebody who's been a victim."

With just your name, Social Security number and birthdate, identity thieves are often limited only by their creativity. They can go on a shopping spree using credit cards in your name, take out large sums of money at the bank, and apply for health insurance, cell phone service or even a new job as your financially irresponsible clone. And it can take years to set the record straight.

In addition to pressing charges, for example, Frank faced the formidable task of cleaning up her destroyed credit. She spent over 500 hours on the phone and wrote 90 certified letters to credit reporting agencies, communicating with credit grantors, crime investigators, banks, insurance companies and even the State Bar of California.

"It took tremendous effort to overcome these obstacles, and assert my legal and financial rights," Frank said.

Stealing your good name

Identity thieves once rifled through the trash (a practice known in criminal circles as "dumpster diving") to look for discarded credit offers, bank statements and other useful documents, but these days they're more likely to cut to the chase and just steal your mail, according to Linda Foley, executive director of the Identity Theft Resource Center.

There can also be some acting involved. Thieves can call one of the three main credit bureaus and pretend to be a prospective landlord, employer or lender, asking for your credit information; or they can even call you, representing a company that doesn't exist, in an attempt to squeeze out your name, Social Security number and other goodies, said Brad Dakake, a consumer advocate at the Massachusetts Public Interest Research Group.

Computer-savvy thieves can even get your information from the Internet. And an alarming number of swindlers now get their data from insiders, or are insiders -- at your office, the doctor's office, credit bureaus and health insurance carriers, and so on. These people are willing to sell your name and information or use it themselves, said Frank, who later wrote a book about her experiences and created the Identity Theft Survival Kit to help other victims.

An ounce of prevention

You can't control what other people do with your information, but you can take a few preventative measures of your own. Here are the guidelines:

Keep your Social Security number to yourself. Don't give it to folks who don't need it, and know that many people who don't need it will ask for it. If you have a driver's license, never opt to use your Social Security number as your license number as well.

Remember to shred. Enron and Andersen may have recently revealed the darker side of document shredding. But if you're tossing old tax returns, bank statements, or other documents that contain the information hungry identity thieves crave, shredding is the only way to go. A crosscut paper shredder works best, according to the Identity Theft Resource Center.

Get your credit report at least once a year. Call the three main credit bureaus, Equifax (1-800-685-1111), Experian (1-888-397-3742) and Transunion (1-800-888-4213) and ask that they mail you a copy of your credit report. Make sure there are no surprises, and that you can account for all the activity on that report.

Opt out. Thieves use mailed pre-approved credit offers and the "convenience checks" that often accompany them to get a credit card quickly. According to the postmaster general, 30 percent of convenience checks get used fraudulently. If you want fewer pre-approved credit offers in your mailbox, you can call (800) 5-OPT-OUT and ask them to remove your name and address from the mailing lists.

Tell your bank, health insurer, and others not to share. Call the companies and services you deal with regularly and tell them not to share your information with their affiliates.

Use common sense! Don't have conversations about your bank account or credit in public. Deposit mail in a locked mailbox, ideally inside the post office itself. Pay attention to your billing cycles, use complicated ATM passwords, memorize your Social Security number (so you don't have to show the card in public) and be cautious about who has access to information in your home.

Getting your identity back

Dealing with identity theft poses immense frustrations. Many consumer advocates blame the credit industry for issuing credit with so few restrictions. Creditors often write off a large portion of the losses, or make up for them by charging hefty fees, leaving consumers, merchants and law enforcers to deal with the rest, said Frank.

"When you're a victim of identity theft, you're not liable for the money, but you are responsible for getting rid of the accounts and restoring your credit," Merzwinski said. "That means you have to deal with the credit industry, and they often refuse to take your calls. They'd be happy to leave you on hold until the next Final Four [NCAA basketball tournament]."

If you do fall victim, there are a few things you must do: first, of course, ask that any fraudulent accounts be closed. Contact the fraud departments of the three major credit bureaus (see telephone numbers above) and have a fraud alert placed on your account. The alert requires that no new credit be granted without your approval.

| |

Related stories

Related stories

| |

| | |

| | |

|

File a report with the police, and get a copy, in case the bank, the credit card company or others need proof of the crime later on. Finally, file the Federal Trade Commission's ID Theft Affidavit, which alerts many companies and organizations that may have fraudulent accounts opened in your name.

Unfortunately, there's no quick and easy solution, and you'll likely spend a lot of time explaining the situation on the phone. Each victim, on average, spends 175 hours and about $800 out of his own pocket to clear his name, said Dakake.

|