|

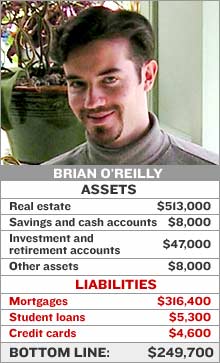

NEW YORK (CNN/Money) - Brian O'Reilly doesn't work a 40-hour week, but he's 28 years old with three properties. His Jaguar is paid for and he makes $60,000 a year. His net worth is about $250,000, but the guy doesn't have a trust fund.

"I'm not real frugal or thrifty," said O'Reilly. "I just don't waste money on little things that don't matter, but spend on big things that do."

For example, Brian eats in and lives a day-to-day life well below his means. But he has managed to fund trips to 14 countries in the last two years...all while saving more than $10,000 a year since graduating from college in 1999.

He did it all by starting a small business and buying a home soon after graduating from college � big risks for a recent grad with $1,000 in credit card debt and $14,000 in student loans.

Moreover, the self-employed computer consultant is shooting for a spot in the millionaire's club by the time he's 40; and is pretty sure he can do it without living like a pauper.

"You cannot ignore your financial situation," he said. "Figure out what you make and base your spending on that amount."

O'Reilly believes it's better to be realistic and enjoy reasonably nice things rather than indulge in extravagant spending, and later deal with the consequences of debt and financial stress.

A different kind of dream

Consumerism, conspicuous, rampant and otherwise, is as American as apple pie, accounting for about two-thirds of the nation's economic activity.

And for many Americans, they're buying what they can't afford. According to research group RoperASW, only 38 percent of Americans can pay off their credit cards each month, and only 28 percent have enough savings to weather a financial hardship.

But O'Reilly isn't having it.

If he can't pay off a credit card bill, rather than carry a balance he pays with his home equity line of credit. This way he said he pays 6.5 percent APR interest, and it's fully tax deductible.

"I've managed to save so much because I live below my means," Brian said, adding that America's consumer culture is difficult to resist.

So he avoids debt by buying the best quality item he has the cash for, at the lowest cost, rather than buying the most expensive thing he can afford.

"I own a Jaguar, but I bought it eight years old and paid $11,000 for it in cash. You can't get a new Honda Accord for that," said O'Reilly. "I could have afforded a more expensive car, but wouldn't have been able to pay for it without having to make car payments."

He also vacations where the great deals are, like scoring a $528 roundtrip ticket to Japan. And he foregoes high-end accommodations to free up money for things he cares about more.

Business owner, real estate tycoon

"Starting your own business isn't for everyone, but for the right people it's much better than climbing the corporate ladder," said O'Reilly.

He saves big on tax deductions by running his computer consultancy out of his home, and just started a tech partnership that will allow him to implement tech ideas rather than just set up computer systems for other companies.

And while his consulting work is his primary source of income, it's not his only source of wealth.

"When I graduated from college I was paying $900 a month in rent, and finally decided that I was tired of throwing that away," said O'Reilly.

So he bought his current home near his alma mater Johns Hopkins University, where he also works as a consultant.

In 2000, the price was a touch high at $80,000 for a three-bedroom house on a quiet street, but the neighborhood soon took off and O'Reilly bought two rental properties.

The mortgages on his investment homes are completely covered by his tenants, and he rents out a room in his house as another source of cashflow.

While other people have made a lot of money thanks to smart real estate buys and long hours at the office, O'Reilly refuses to sacrifice enjoyment of life to amass savings.

"I don't do work I don't like, and I don't feel that I have to deprive myself," he said. "And that's what sets me apart."

|