|

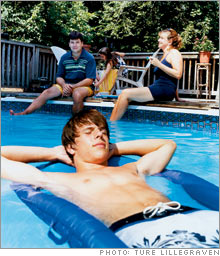

| The Hart kids -- Jordan, 17, Madison, 11 (background), and Savannah, 8 (not shown) -- all chipped in with parents John and Sheri to buy a backyard pool. |

|

|

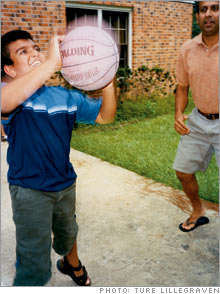

| Sabrina Kumaran, 6, and her brother Sathesh, 10 (below), earn money by helping their Avon rep mom organize beauty products. |

|

|

|

|

| Tip: Let kids do odd jobs. Sathesh Kumaran, 10, learns by helping his mom at her work. |

|

|

| Lisa (left) and Jaime Alpert, 23, learned to be thrifty as kids when their mom sent them on scavenger hunts at the store to find the best deals. |

|

|

| | � | | � | | Total outlay:� | $20,000� | | Retirement kitty:� | $1,100,612� |

| | |

| �Note: Assumes return of 8 percent annually. |

|

|

NEW YORK (MONEY Magazine) -

Seven out of 10 Americans believe they are living a better life than their parents, according to a new MONEY survey, and almost all of those who are moms and dads say they want to make sure their kids do the same.

It's an integral part of the American dream -- the notion that each generation should enjoy a higher standard of living than the one that came before it. And if you're a mom or dad, chances are you want that for your kids too.

But while your own parents and grandparents could pretty much take this outcome for granted, today's children face a far different economic landscape -- one marked by stiffer global competition, an uncertain job market, easier credit, declining retirement benefits and a host of new financial products that make managing money on a day-to-day basis increasingly complex.

The result: That rising standard of living is no longer the slam dunk that previous generations of Americans enjoyed.

Scary stuff, huh? Sure, but challenging too, with the potential for greater rewards -- yes, that better life -- for young people who are well equipped to navigate the new terrain. Whether your kids are toddlers or have toddlers of their own, you have the power to tilt the financial odds in their favor. These strategies will help.

Strategy No. 1: Explain the new money rules

Unlike you and your parents before you, kids today are growing up in a world in which technology has made money largely invisible. Want to buy something? Hand a piece of plastic to a cashier and the goods are yours. Need cash? Stick a card into a bank machine and out pops the dough that probably landed in your account through direct deposit of your paycheck.

Since actual dollars change hands far less often these days, children don't get to learn by observation how financial transactions work, and parents miss out on everyday opportunities to teach the basics of managing money.

So it's up to Mom and Dad to explain what kids can't see with their own eyes, starting as soon as your son throws his first candy-demanding tantrum at the grocery store or your daughter asks for a magic money card like yours.

"The earlier you begin talking to your children about money, the better chance you'll have to instill the values you think are important," says Philip Heckman, director of youth programs for the Credit Union National Association.

Instead of delivering formal lectures, casually drop lessons into your daily financial routines. When your preschooler accompanies you to the ATM, let him know that you're taking out money you earned at work and put in the bank for safekeeping. Verbalize your purchase considerations at the store, comparing prices and quality out loud.

If you whip out the plastic to pay, explain that either the amount is being taken out of your bank account directly (if you are paying with a debit card) or you will get a bill in the mail that you must pay later (if it's a credit card). Add layers of detail and sophistication as your child gets older, explaining, for example, the concept of interest and late fees.

Look for ways to directly involve your child in financial activities, making a game of it if possible.

When twins Jaime and Lisa Alpert were little, their mother Joni routinely armed the girls with coupons while shopping together for groceries, then sent them on scavenger hunts through the store to find the best deals. At checkout, she'd show her daughters the register tape so they could see how much they'd saved. And if Joni caught a scanner error and got a refund, she'd immediately hand the money to the kids.

If you talk to a child about the importance of saving money, "it just goes in one ear and out the other," says Joni, a radio producer in Atlanta. But if you give them the money saved, she says, "it's a very powerful motivator."

These childhood shopping trips have made thriftiness so deeply ingrained for Jaime and Lisa, now 23, that they routinely and creatively search for bargains, no matter what they're buying. Case in point: When the girls graduated from different colleges on different weekends earlier this year, they didn't each buy graduation robes. Instead, they shared a single cap and gown, saving one last $30 on their college education.

Strategy No. 2: Fight the spend trend

Saving money, of course, has always been a virtue. But for 21st-century kids like the Alperts, who can no longer rely on company pensions and Social Security to fund their old age, it is an absolute necessity. Yet the temptation to spend, spend, spend has never been greater, with the average child viewing at least 20,000 commercials a year and credit-card issuers peddling plastic to consumers at ever-younger ages.

One way to counter today's gotta-have-it-now mentality is to make saving money a habit early on. Start with a traditional piggy bank, preferably a see-through container. A kindergartner may not be impressed by a bank balance statement, but he will intuitively understand that a large pile of coins is better than a small one and will get satisfaction from watching it grow.

That's why New York City media director Vladimir Leveque, 32, gave his son Amir, 5, an empty five-gallon watercooler bottle that the boy is filling up with loose change that his dad brings home from work each night.

When the bottle is full, Leveque will use the money to fund Amir's first savings account. "I'm introducing him to the ideology of saving," Leveque says.

As your child grows older, give her money of her own to manage. Then encourage her to regularly set some of it aside for long-term goals, like a coveted toy or, for a teenager, a cell phone. Help her plan how much she'll need to save, over what time period and, as extra incentive, consider matching a portion of what she socks away -- an early introduction to the 401(k) concept. Open a savings account for her at the bank and suggest that she put some of her money there for safekeeping.

The idea: "Make it easy to save and hard to spend," says Robert Manning, a finance professor at Rochester Institute of Technology.

Get the whole family involved in savings efforts too, as opportunities arise. For instance, when their three kids clamored for a pool in the backyard a few years ago, Sheri and John Hart of Dayton spearheaded a "pool plan" to save the necessary $3,500 for the aboveground model they wanted.

Everyone agreed to make sacrifices: The family ate fewer meals out; John, 46, general counsel for the University of Dayton, moonlighted doing some extra legal work; Sheri, 43, postponed haircuts; the kids contributed some birthday money. If one of them whined to buy something on a shopping trip, "We just used the phrase 'pool plan,'" says John, "and they would remember why this was a looking trip and not a buying trip."

When the pool was finally installed, "there was a sense of pride and accomplishment," says John. "The kids didn't miss what they gave up in order to achieve it."

And the lesson appears to be sticking. His son Jordan, 17, recently used his own savings from afterschool and summer jobs to buy his first car.

Strategy No. 3: Hone their competitive edge

The paternalistic, cradle-to-grave employer is so 20th century. Kids of the new millennium can expect to switch jobs several times in the course of a career, and perhaps industries as well, as technologies change, companies seek to keep costs down and global competition stiffens.

While you can't know which jobs will be in demand a generation from now, you can count on workers with an enterprising and entrepreneurial bent to have an edge.

"We've got to prepare our children to be flexible and self-sufficient to survive in an unpredictable job market and a changing economy," says Bonnie Drew, an executive at YoungBiz, which teaches business skills to young people.

Nurture your child's inner entrepreneur in the grade school years by helping him find odd jobs to do, like washing cars or raking yards. Encourage moneymaking projects such as a used-toy sale or a lemonade stand. They provide an opportunity, says Drew, to talk about various aspects of a business, including how to market it and set a price that will turn a profit.

Be sure also to make your own work visible, talking to your kids about your job, taking them with you to the office occasionally and maybe even giving them a task or two to do.

Every couple of weeks or so, for example, Avon representative Poonkulali "Lee" Suresh pays her children Sathesh, 10, and Sabrina, 6, a few dollars an hour to help her set up tables, stamp her name on catalogues and sort out products.

"This is the best way for them to understand that money does not come easily and you have to work for what you want," says Suresh, 38, who grew up in Sri Lanka and immigrated to the U.S. with her husband Suresh Kumaran, 42, six years ago.

Parents of teens with afterschool and summer jobs can give their kids a huge leg up by helping them to invest some of their earnings in a Roth IRA. Although it may seem ludicrously premature to think about retirement savings for a teen, the power of compounding over a half century or so makes the payoff huge: A young worker who contributes $4,000 a year from ages 14 to 18 and lets it ride at 8 percent for the next 50 years will amass a nest egg of more than $1.1 million, even if she never saves another dime.

Of course, you may discourage your child from ever working again if you insist that she lock away all her earnings for decades. A more practical approach, if you can afford it: Ask your child to put some of her money into the Roth, and fund the rest yourself, up to the total your child earned or the current maximum of $4,000, whichever is less.

Strategy No. 4: Reach higher for education

For past generations, graduating from a good college was an almost surefire means to success. With degrees increasingly commonplace, however, future generations may need to kick it up a notch to get the same higher-education advantage.

According to the College Board, the median income of someone who graduates with a master's degree was $59,500 in 2003 -- nearly 20 percent more than the $49,900 earned by those with a four-year degree. A professional degree was worth $95,700, or 92 percent more.

And, yes, quality counts. A 2005 Cornell University study reports that students who attend better-rated colleges do indeed end up earning more than their counterparts at lesser institutions -- and that the boost to income from attending higher-quality schools is big enough to compensate for their typically higher cost.

So try bumping up those contributions to your 529 plan (or get started now), and steel yourself to the idea of paying those tuition bills somewhat longer than you'd planned. The ultimate price tag, though, may be smaller than you think if you send your child to a top-rated public institution. In fact, the same study found that attending highly rated public colleges packed the same earnings punch as comparable private schools, making them the better investment, in the researcher's estimation.

Strategy No. 5: Give big kids a hand too

Your role as a financial mentor doesn't necessarily end once your child is an adult. According to a University of Michigan study, people ages 25 to 34 who live on their own typically receive more than $14,000 in assistance from their parents. As the economic climate gets tougher, odds are your adult child could probably use a hand from you too.

Giving money to your kids can reduce the taxes your heirs may ultimately owe on your estate. (Only estates worth more than $1.5 million will be taxed this year, and that amount is due to rise over the next few years. The estate tax is scheduled to be eliminated in 2010, and then, unless the law is changed, it will be reinstated with an exemption of $1 million in 2011.) You can give as much as $11,000 to each child this year without paying a gift tax; couples can give up to $22,000.

If you're like most families, though, you're probably less concerned about estate planning than you are with simply providing the help your child needs now.

To make sure a gift of money has the most impact, consider targeting it for a particular purpose -- say, chipping in for the down payment on a first home or paying off the balance on a high-interest credit card.

If you're attaching conditions, however, make your expectations clear. If you intend that the money be used for graduate school and you'd be unhappy if it were spent on a new car instead, say so in advance to avoid hard feelings, and give your child an opportunity to decline the gift.

Also consider that, however well intentioned your gifts may be, too much of a good thing can hurt your kids in the long run. Regular gifts may encourage a lifestyle your son can't really afford or send the message to your daughter that she can't take care of herself.

"Parents should use their money to help their kids become independent," says Jon Gallo, co-author of "Silver Spoon Kids: How Successful Parents Raise Responsible Children," "not to maintain their dependence."

In fact, the single best step you can take to help your kids prosper as adults won't cost you a dime: Be a good role model. After all, children learn most of what they know by observation. So if you rely on plastic to keep up with the Joneses and never manage to save a dime, don't be surprised if your children grow up to do the same, no matter how much you preach to them about living within their means.

"It's like parents telling their kids not to smoke and then lighting up a pack a day," says financial planner Kevin McKinley, author of "Make Your Kid a Millionaire."

In the end, there's no substitute for setting the right example. If you haven't exactly been a paragon of financial virtue lately, there's no time like the present to start.

Making allowances

Try these tips to get the biggest bang for your allowance buck.

- Start early As soon as kids understand that money can buy cool stuff, they're ready.

- Set ground rules Spell out how much you'll give and what expenses they should pay. Increase both as they get older.

- Don't attach strings An allowance shouldn't depend on doing chores or getting A's -- stuff kids should try to do anyway.

- Don't rescue them Don't stop a foolish purchase or grant an advance if they run out of cash before payday. Kids learn best from their own mistakes.

________________________

Looking for a new home to start your family? Click here.

Click here for the CNN/Money special report, "Back to School."

|