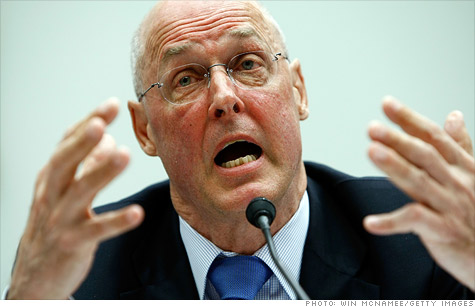

Former Treasury Secretary Henry Paulson put mortgage agencies Fannie Mae and Freddie Mac into conservatorship in 2008. But little progress has been made since to help them.

NEW YORK (CNNMoney) -- It has been more than three years since then Treasury Secretary Henry Paulson fired his famous metaphorical bazooka and the federal government seized control of mortgage agencies Fannie Mae and Freddie Mac.

Sadly, Fannie and Freddie are still a cause for worry and a source of national embarrassment.

Late Tuesday, Fannie Mae said that CEO Mike Williams was stepping down sometime this year. That follows the news late last year that Freddie Mac CEO Ed Haldeman was also planning to leave.

Former Fannie CEO Daniel Mudd and former Freddie CEO Richard Syron have each been charged with fraud by the Securities and Exchange Commission.

Both agencies, which play key roles in helping to secure financing for homeowners, have continued to rack up sizeable financial losses over the past few years. It is estimated that their bailout will eventually cost taxpayers as much as $124 billion through 2014.

Yet, not much has been done to try and change the two companies for the better. There was shockingly little in the way of actual reform for Fannie (FNMA, Fortune 500) and Freddie (FMCC, Fortune 500) in the Dodd-Frank Wall Street Reform Act that became law in 2010.

Several members of Congress, including former Senator Chris Dodd and House Rep. Barney Frank, have been accused of conflicts of interest regarding Fannie and Freddie. Lawmakers have repeatedly denied that this played a role in the lack of any major new regulations for Fannie and Freddie.

But the biggest problem is that the full government control of Fannie and Freddie makes the agencies convenient legislative tools for members on both sides of the aisle.

For example, Congress finally agreed on a temporary extension of the payroll tax cut late last year. But to help finance that, Fannie and Freddie were forced by their overseer, the Federal Housing Finance Authority (FHFA), to raise fees they charge lenders to guarantee new loans.

"The problem is that Fannie and Freddie are the cookie jar for Congress. What is going to need to happen is that Fannie and Freddie need to be moved out of conservatorship or this won't end," said Anthony Sanders, senior scholar with the Mercatus Center at George Mason University in Fairfax, Va.

"Every time you look at the news and see Freddie Mac or Fannie Mae in a headline, you wince about what Congress and FHFA are going to ask them to do next," Sanders added.

Others argue that politicians need to rethink housing policy overall.

It may be heretical for an elected official to suggest that renting is the new American dream. But as long as home ownership is still held up as the pantheon of financial success and a goal for all Americans, expect more of the same from Fannie and Freddie.

"Originally, Fannie and Freddie were born out of a sensible goal to create more liquidity in the housing market. But they got co-opted for political reasons," said Joseph Mason, professor in the department of finance at LSU's E. J. Ourso College of Business in Baton Rouge.

"Nobody in Washington has backed off the populist proposition that everyone should own a home. Until that changes, nothing will change at Fannie Mae and Freddie Mac," he added.

So what's the solution for Fannie Mae and Freddie Mac? They need to be weaned off the government dole. Instead of having FHFA (foofa!) be their master, the free market should take that job.

Yes, I realize that's asking the same people who helped contribute to the 2008 financial calamity to become more involved again. But that's still a better alternative than the status quo.

"You would hope that over time there is greater private sector participation in the mortgage financing business. It's not going to happen now given the state of the market, but continuing to use Fannie and Freddie to stimulate housing is not feasible," said Brian Levitt, economist with OppenheimerFunds in New York.

"We have to realize the way things worked before will not work in the future," Levitt added.

Exactly. What incentive is there for a bright, capable CEO to come work for Fannie or Freddie as long as the government is the ultimate boss?

To be fair, Fannie Mae and Freddie Mac have cleaned up their balance sheets a bit in the past few years. They have not made the same mistakes in regard to financing bad credit risks as they did during the housing boom.

But as long as older loans are a problem, who would want to lead Fannie or Freddie? It's a thankless job. Both Williams and Haldeman were criticized for their salaries. Who needs that grief?

"Fannie and Freddie probably will have a revolving door with CEOs for awhile until something is done on a permanent basis to fix them," Sanders said. "Legacy loans are killing Fannie and Freddie. It's an untenable position for executives right now."

But it's not so untenable for politicians and bureaucrats. That's the problem.

Best of StockTwits: A cleanup is needed in aisle 8 for grocery stocks. China is hot again. And investors apparently can all use a little KFC.

Retail_Guru: Supervalu pulled back promos to lift margin, but sales, traffic fell as result. After 5 years, still taking charges on Albertsons $SVU

SuperValu (SVU, Fortune 500) posted a big loss and investors are not happy. Shares plunged 12% Wednesday. Kroger (KR, Fortune 500) and Safeway (SWY, Fortune 500) dipped too.

Here's something I've always found interesting. The two big supermarket chains that I personally find to be the best (as in most pleasant to shop in) are both private: Publix and Wegmans. Maybe there's something to be said for not having to worry about fickle shareholders.

LTbioinvestor: looks like CHINA is back ... watch the leaders $SINA $BIDU $NTES .... the laggards $YOKU $DANG $RENN .... the micro$COGO $KGJI ....

Dlerch: Think it's a reflection of china story as a whole. Hang Seng back over 19k.. So stocks beat down hardest pop the most. $SINA $YOKU

As I wrote yesterday, fears of a China slowdown may be slightly overdone. So some Chinese stocks should bounce back after a brutal 2011. But I'd be wary of some of the laggards though. Online video company Youku (YOKU), for example, is unprofitable in a highly competitive area.

So if you really want to invest in China, you might be best doing it through American companies.

TrendRida: $YUM getting it done at all-time highs...

KFC and Taco Bell owner Yum! (YUM, Fortune 500) has been wildly successful in China. And it's doing pretty well in the U.S. too. This is a solid company. It may be a tad pricey but it pays a strong dividend and arguably deserves a premium.

The opinions expressed in this commentary are solely those of Paul R. La Monica. Other than Time Warner, the parent of CNNMoney, and Abbott Laboratories, La Monica does not own positions in any individual stocks. ![]()

| Overnight Avg Rate | Latest | Change | Last Week |

|---|---|---|---|

| 30 yr fixed | 3.80% | 3.88% | |

| 15 yr fixed | 3.20% | 3.23% | |

| 5/1 ARM | 3.84% | 3.88% | |

| 30 yr refi | 3.82% | 3.93% | |

| 15 yr refi | 3.20% | 3.23% |

Today's featured rates:

| Latest Report | Next Update |

|---|---|

| Home prices | Aug 28 |

| Consumer confidence | Aug 28 |

| GDP | Aug 29 |

| Manufacturing (ISM) | Sept 4 |

| Jobs | Sept 7 |

| Inflation (CPI) | Sept 14 |

| Retail sales | Sept 14 |