Better disclosure would help. Your average credit card application is easier to decode than many mortgage documents. Alex J. Pollock of the American Enterprise Institute, in testimony to the House subcommitte on financial institutions today, says that banks should give all borrowers a one page document with the following information.

-Amount of loan -LTV [loan-to-value] ratio -Final maturity -Prepayment fee, if any -Balloon payment, if any -Points and closing costs -Initial rate on loan in % and monthly payment in dollars -How long this rate is good for=when higher rate starts -Fully indexed rate on loan in % and monthly payment in dollars -Your household income on which this loan is based -Initial monthly payment as % of income, and payment plus taxes and insurance as % income -Fully indexed monthly payment as % income, and payment plus taxes and insurance as % income -A name, number and e-mail for you to contact with any questions -An authorized signature of the loan originator -The signature of the borrower.

What's amazing is that all this isn't standard practice already.

(By the way, I'll be blogging fairly lightly this week. The day job is looking like it will be a day-and-night job for a bit.)

At CreditSlips.org, Tara Twomey tells us about one-way ARMs:

The Senate Banking Committee has invited representatives from the top five subprime lending companies to "explain their lending practices in the subprime mortgage market" at a hearing scheduled for tomorrow, March 22. With all the recent focus on teaser rates and no document loans, the one-way adjustable rate mortgage (ARM) probably won't get much attention. An analysis of the actual terms of recent ARM loans, however, shows that one-way ARMs are yet another example of how subprime lenders stack the deck against borrowers.

In its simplest form an adjustable rate mortgage is one in which the interest rate for the loan is pegged to an "index" and for which the interest rate is adjusted at set intervals (e.g., 6 months, 1 year, etc.). If the index increases, the borrower's interest rate increases, if the index declines, the borrower's interest rate goes down. The floating rate structure of the ARM allows lenders and borrowers to share the interest rate risk. In exchange for assuming some of this risk, borrowers generally receive lower initial interest rates. This economic reward for risk-sharing is the justification for ARM loans--at least in theory.

In practice, the one-way ARM, which is ubiquitous in the subprime market, only adjusts upwards from the initial rate. By the terms of the note the interest rate can never drop below the initial rate even if the index goes down. As a result, borrowers, not Wall Street, bear the brunt of any interest rate volatility.

Please buy this annuity. My daughter needs surgery.

Investment News, a trade newspaper for financial advisers, reports:

Some insurers are taking away their advisers' group health insurance and other employment benefits if proprietary-product quotas aren't met, advisers say.

..."For some advisers, health insurance is a bigger incentive than trips to Rio [de Janeiro, Brazil], extra commission income or plaques and trophies," [investment adviser Chris] Cooper said.

Harvard Law School bankruptcy expert Elizabeth Warren points to these numbers in this blog post at one of my new favorite wonk sites, CreditSlips.org. Here's Warren:

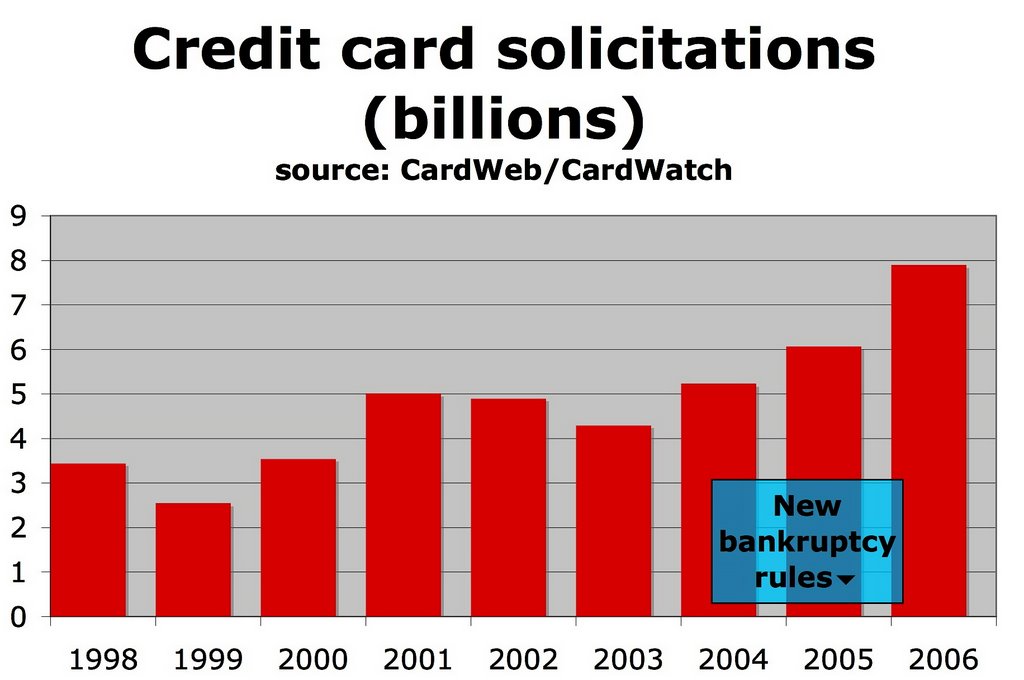

In 2005, Congress gave the credit industry what it wanted: tighter bankruptcy laws. In 2006, the credit industry responded by mailing out 8 billion credit card solicitations--up 30% from 2005. Larry Ausubel and others predicted during the debates over the bankruptcy laws that if Congress made it tougher to go bankrupt, then lenders would engage in riskier lending as they tried harder to get people to borrow.

What kinds of risks are the card companies willing to take on? With about 110 million households in the US, that's about 73 card offers per household. If the average card offers is about $5,000 in pre-approved credit, that about $365,000 in offers for every American household--or about $1000 a day, every day of the year....

If debtors have no bankruptcy option, Ronald Mann points out that creditors can keep them in the sweat box longer. Perhaps if bankruptcy were outlawed altogether the mailings would go to 16 billion, and if debtors' prisons were reinstituted, could the mailings top 25 billion? Ah, the possibilities.

By the way, you can call (888) 5-OPT-OUT if you want to stop getting these mailings. Click here for more info from the Privacy Rights Clearinghouse.

Senator (and Presdential hopeful) Chris Dodd is talking about it. After all, 2.2 million American households are at risk. Maybe more. But what would a bailout look like?

For a start, there's moral suasion. Before we considerany major government spending, lenders are going to have to take their licks. Here's Berkeley economist Brad DeLong, arguing that the problem here isn't simply that some homeowners got in over their heads. The whole system failed, and that means everyone with a stake in it has to pitch in to prevent a crisis:

I can see one constructive thing that bank regulators can do: they can publicly note [to lenders] that foreclosure is an appropriate response to individual cases in which payments are not being made because idiosyncratic things have gone wrong with individual household's finances, but that foreclosure is not an appropriate response to a systemic problem triggered by macroeconomic risks that have come calling. The appropriate response [for lenders] when it is an aggregate rather than an idiosyncratic shock is to renegotiate the loan--not to foreclose on a homeowner. And banks that do the second rather than the first are not fulfilling their responsibility to the system of which they are a part.

Don't provide direct financial support to homeowners in trouble, urges Nouriel Roubini of Roubini Global Economics:

Public funds to help borrowers should be used with care for several reasons. First, some forms of borrowers' financial support end up bailing out also the culprits of this mess; thus, these specific forms of support of homeowners under financial distress should be avoided. For example, direct subsidies to households who cannot afford their now-reset and excessively high mortgage payments end up helping the victims as well as the culprits.

By "culprits" Roubini means the lenders. Instead, he says, the feds should force the lender to renegotiate payments:

For example, suppose that the value of a home (with zero down-payment) has fallen 10% (following the current housing bust) and that the borrower cannot now pay the full value of the mortgage debt servicing payments that are now being reset at much higher interest rates. Then, if the borrower can afford a lower string of service payments that, in NPV [net present value, I think--P.R.] terms, is 10% lower than the initial terms of the mortgage (and equal to the true value of the home), the solution will be to allow a reduction of 10% (in NPV terms) of the debt-servicing payments for the borrower.

Hillary Clinton wants to make it easier for people to refinance out of onerous loans. From Bloomberg:

Clinton proposed eliminating pre-payment penalties that she said are "designed to trap borrowers" by imposing high fees for paying off loans ahead of time. Such penalties apply to 70 percent of subprime loans and less than 5 percent of prime loans, she said.

[Update 3/19:Here are Clinton's remarks. On reading it again, I see it's not clear if she's proposing to change the terms of current subbprime loans. Seems like not.] Washington Post columnist Steven Pearlstein suggests a new mission for Fannie and Freddie:

...what's needed is some mechanism to encourage the faceless investors who now hold those mortgages to accept less money than they were expecting, while at the same time helping homeowners to refinance their homes with more appropriate mortgages.

This, it seems to me, is a perfect assignment for Fannie Mae and Freddie Mac, which were chartered by the federal government with the express purpose of stepping in when private markets fail. They have the ability to raise and commit billions of dollars to the refinancing effort. They have active networks of lenders with necessary skills in financial counseling and loan workouts. And what better way for them to atone for their recent accounting sins and burnish their affordable-housing bona fides than to provide a market-based solution to this mess?

Even then, it won't be easy. Getting investors to forgo further interest payments and take 60 or 80 cents on the dollar they are owed may require some financial sweeteners. And to pay for those sweeteners, homeowners -- who, by the way, have some responsibility here -- would have to agree to share any profits they earn from selling or refinancing their homes in the future. Through the magic of securitization, Fannie and Freddie could turn that future stream of income into needed cash today.

[Update 3/19: It's worth underlining the point that the ideas discussed above don't require, as a first order of business, a direct government subsidy. But from the news story I linked to, it certainly sounds like Dodd is willing to have Congress stump up some cash.] Nicole Gelinas at the conservative City Journal makes the case for government just butting out:

If the government, or its proxy, now steps in and purchases those mortgages, or otherwise systematically bails out borrowers, it will create a hazard for the future. The next generation of mortgage lenders won't take the high risk of subprime home loans seriously, because they'll expect that, in the event of another crisis, the government will step in and bail them out again. So they'll be even more eager to approve the risky subprime mortgages that are getting so many borrowers into trouble in the first place.

And what about all those afflicted borrowers? It’s a harsh but unavoidable truth that many of them are in trouble now because they borrowed overpriced houses that were way beyond their means. If a family didn’t do the hard work of saving for a down payment and buying a house on which it could afford to pay a normal 30-year mortgage, it's unfair for the government to bail it out—and its lender. Remember who would subsidize that bailout through federal taxes: the family down the street that rented for a few years while it saved up money, or that bought a smaller, older house within its means.

By the way, my family is "the family down the street" that kept on renting rather than overstretching our finances to buy in a market we can't afford. So I sympathize with that last point. But this kind of cool tit-for-tat analysis seems a little unmoored from everyday experience. For the sake of argument, let's set aside the issue of whether lenders were deceitful or predatory, or whether the government encouraged this kind of behavior. I know I'm going to get lots of comments about 25-year-old idiots with $45,000 salaries buying McMansions and giant plasma screens and fancy cars that they couldn't afford. But I suspect that many people who are in trouble now were mostly trying to buy into a safe, stable neighborhood with good schools. The real-life choice for many families in bubble markets isn't between a fancy McMansion and a modest older home. It's between a house in a school district that works, and a house in one that doesn't.

Still, who could really argue that the government should prop up unrealistic home prices? Clearly, the air has to come out of some of these markets. The question is: How quickly? If mortgage blow-ups are really a dire threat to the overall economy, perhaps even those who were prudent all these years could grudgingly accept a carefully limited government intervention. Forced into a choice, I'd rather keep my job than satisfy my sense of cosmic justice.

A preview of the coming national health care debate

It used to be that political advertising was mostly limited to the election season. But lately, during the 11 o'clock news, New Yorkers have been treated to a back-and-forth ad battle between liberal Democratic Gov. Eliot Spitzer and a coalition of hospitals and the big healthcare-workers union. Spitzer wants to reduce state health spending, especially Medicare payments to hospitals; he also wants to expand Medicaid coverage for the uninsured. Here's a sample of the ads. First the ad from the union and hospitals:

The New York Post is reporting today that the hospitals group has pulled out of the campaign. Here's the ad from the governor:

So... scrappy, compassionate nurses, or angelic sick kids. Which do you like better?

We're going to see more of this kind of thing all across the country, and eventually it's going to become a feature of the national debate. Whether we end up with a system of universal care, or plod along with the current "private" system in which the government pays for 45% to 60% of spending, or do something market-based, this country is going to have to figure out a way to control health care costs. If we move towards more, rather than less, government involvement in health care--and that's my prediction--voters will have to make some choices.

Should we hold down the salaries of hard-working nurses? Squeeze the incomes of expensively trained and dedicated doctors? Put pressure on the profits of the drug companies that develop all these great new treatments? Shut down hospitals in vulnerable communities? Raise taxes on Joe Citizen? Provide only spartan care to the young, the poor, and the aged? Every potential loser will have a sympathetic case to make. And every one of them will buy an ad, except for the young and the poor. Insurance companies will have a tougher time getting anyone to feel sorry for them, but they'll eat up plenty of air time to call for preserving "choice."

This is one of the most challenging debates we can have in a democracy. I'm hopeful that it will move beyond dueling 30-second ads. But they'll be a factor.

(By the way, the Albany Times-Union has been doing a better job than most at clearing through the noise in the New York debate. Click here and here for more detail on what's at stake.)

Real estate can only fall 10% to 20%, right? Right?

You've probably read this before: Even when housing prices slump, they don't fall all that much, at least compared to stocks and other risky investments. I've passed on this bit of "wisdom" myself. And it it's not a totally ridiculous thing to say: Even in the big California bust of the mid-1990s, prices in the L.A.-Orange County metro area fell only 20% peak to trough in the region's worst five years. That's no Nasdaq. But, well, there's a bit more to it than that....

Below is a chart I made from data in a 2005 FDIC report. It shows the worst peak-to-trough five-year nominal performance for housing prices in several markets. Sorry--the labels are a bit hard to read. (Try clicking on the chart to open it in a new window.) The blue cities are in California, the green ones are in New England. In red, dropping by as much as 40%, are "oil patch" towns, which cracked in the late 1980s right along with oil prices.

It's easy enough to dismiss the evidence from the oil patch, if you want to. Prices there were forced down by an unusual, and very local, economic shock. The economies of L.A. and Boston are better diversified. Then again, if the oil boom-and-bust of the 1980s was an anomaly, what should we call the easy-credit-driven housing inflation of the early 2000s? Liar loans, interest-onlys, option ARMs, and aggressive subprime lending have changed the rules. History wouldn't seem to be a very reliable guide right now.

One reason real estate prices tend to be less volatile than stocks is what housing economist Karl Case calls "downward stickiness." When prices fall, many people just decide to stay in their houses rather than cut their price low enough to make an easy sale. But that also means there's a lot human pain behind a housing decline of "just" 10%. People get stuck in their houses, and that can change their lives. There's a good story in today's USA Today about workers who can't relocate to find better jobs:

Forty-six percent of companies say recruiting employees is becoming more difficult as the housing market turns tepid, according to a 2006 survey by Prudential Relocation.

Three in 10 of those who turned down a relocation did so because of housing and mortgage concerns, according to a 2006 survey by Atlas World Group. That decision can come at a price: More than half of companies had an employee decline a relocation, and 35% of employers say turning down a move hinders an employee's career.

It's been a startling change for companies that must move employees because of corporate growth or local talent shortages. At Petco's corporate headquarters in San Diego, job candidates today want to know about relocating. The company is also doing more to supplement temporary-housing costs for employees who are transferring.

The silver lining here, I guess, is that companies are complaining about real-estate job lock, and they're shelling out a little bit to help entice reluctant workers. That means the job market is still reasonably tight, which should help the economy. If it holds. If.

Update 3/15: For the record, the chart has been corrected since the initial post. (I added "5-year" to the label.)

Update 3/16: Lots of good points in the comments below about the true cost of real estate losses. They should be drilled into the head of every Realtor.

A few things worth expanding upon:

I only have data for nominal (that is, before inflation) losses on real estate. Losses after accounting for inflation are much, much more common: The FDIC report found that since 1978, some 142 metro areas have seen real losses of over 15% over a five year period. That's compared to just the 21 cities in the chart with 15% or greater nominal declines.

Even a nominal loss of 20% looks pretty small compared to nearly 60% (also nominal) for the Nasdaq in the five years after the crash. And while some houses in the LA market may have fallen more like 40%, some Nasdaq stocks went to zero.

The big difference, though, is that most people have a lot more in their house than they do in the Nasdaq. And most people aren't diversified in real estate, whereas that's very easy to do with stocks. Bottom line: It's difficult to make apples-to-apples comparisons of the returns on real estate to the returns on stocks. In real life--that is, in the lives of non-professionals with a limited ability to diversify and a primary goal of purchasing shelter--equities and housing are very different assets. Beware of people in the real-estate industry who use simple average-returns comparisons to convince you that a house is an easy money machine.

Finally, leverage adds to the risk of real estate. But don't forget about imputed rent. You have to live somewhere. The fact that some of your investment pays for a necessary consumption good dampens your risk exposure.

Or feel free to send a letter to the editor about this story.

CNNMoney.com Comment Policy: CNNMoney.com encourages you to add a comment to this discussion. You may not post any unlawful, threatening, libelous, defamatory, obscene, pornographic or other material that would violate the law. Please note that CNNMoney.com makes reasonable efforts to review all comments prior to posting and CNNMoney.com may edit comments for clarity or to keep out questionable or off-topic material. All comments should be relevant to the post and remain respectful of other authors and commenters. By submitting your comment, you hereby give CNNMoney.com the right, but not the obligation, to post, air, edit, exhibit, telecast, cablecast, webcast, re-use, publish, reproduce, use, license, print, distribute or otherwise use your comment(s) and accompanying personal identifying information via all forms of media now known or hereafter devised, worldwide, in perpetuity. CNNMoney.com Privacy Statement.