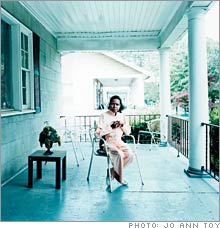

The big money in MedicaidA boom in HMOs for the neediest leads to litigation, controversy - and lots of profits, says Fortune's Bethany McLean.(Fortune Magazine) -- Joyce Hines of Baltimore is 45 years old and weighs just 87 pounds. Years of illness that began in the late 1990s with a bleeding ulcer left her jobless and dependent on Medicaid. She has an intravenous line that delivers both nutrition and medication, takes eight prescriptions and has 11 doctors. But this is a radical improvement from a few years ago, when she was down to 67 pounds and spent over a third of the year in the hospital. Today she lives mostly at home, thanks to a team of caregivers that includes a nurse, a social worker and a case manager. Hines credits Amerigroup (Charts), a publicly traded insurer that provides managed care for the Medicaid population. "No one seemed to know what was going on," she says. "But now we do."

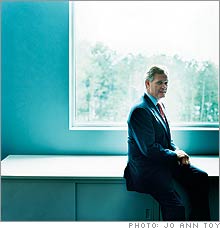

Amerigroup, for its part, says that its approach to someone like Hines - whom it features in its annual report this year - can save taxpayers money by reducing hospital stays and emergency room visits. And saving money is critical for Medicaid, the $330 billion program that covers more than 50 million of the poorest Americans, including the elderly, the disabled and children and their mothers. While Medicare gets most of the headlines, Medicaid - which funds over a third of all births in the U.S. and is paid for jointly by the states and the federal government - is just as apt to break the bank. On average, Medicaid now eats up the largest share of state budgets - around 22 percent, which is more than education - and is growing by 8 percent a year. States have been putting their Medicaid populations into managed-care plans since the early 1990s, but in the past few years they have awarded contracts to a brand-new crop of companies - principally Amerigroup and three others, WellCare (Charts), Centene (Charts) and Molina (Charts) - all of which focus on insuring Medicaid patients. While subsidiaries of multiline insurers like UnitedHealth (Charts, Fortune 500) and WellPoint (Charts, Fortune 500) are still the biggest players in Medicaid, the "pure plays," as they're called, have grown rapidly and now have 22 percent of the Medicaid managed-care market, up from 14 percent in 1999, according to Merrill Lynch analyst Doug Simpson. The four upstart companies now manage the care of about five million Medicaid patients, collect some $9 billion in annual premiums, and have a combined market capitalization of roughly $7 billion. Their remarkable growth - Amerigroup's revenues have risen at an annual rate of over 60 percent in the past decade - has been accompanied by generally stellar stock performance. Jeff McWaters, 50, Amerigroup's CEO, is a proselytizer for his industry. Amerigroup's new headquarters in Virginia Beach feature a picture of President Lyndon Johnson signing the 1965 legislation that created Medicare and Medicaid. "The greatest generation made housing affordable, built roads and sent a man to the moon," McWaters says. "The problem we have not figured out, and which is up to our generation to figure out, is this health-care problem." Any business that is supposed to deliver a public good while maximizing profits for its shareholders invites skepticism. These companies "need to operate in a way that is squeaky-clean," says Dan Mendelson, who oversaw Medicaid at the Office of Management and Budget in the Clinton administration and is now president of consultant Avalere Health. But a close look reveals some blemishes - and more profits than anyone imagined. A tricky business There's a long-standing joke in the industry that when you've seen one Medicaid health plan, you've seen one Medicaid health plan. Policies and reimbursements vary wildly from state to state, and the population that Medicaid serves is incredibly diverse. Medicaid has traditionally been a tricky business for insurers. In the late 1990s states slashed the premiums they pay, and large commercial players like Aetna began exiting the business. But in 1997 the federal government abolished the requirement that health plans serving Medicaid patients get 25 percent of their members from the private sector, setting the stage for Medicaid-only plans. Then states began to raise premiums again as they realized that they needed insurers to stay in business. In 2005 a federal budget resolution sought to cut billions from Medicaid, but even that is seen as positive for the managed-care industry, because it will push more states to try to save money. Both Amerigroup and Centene grew by acquiring smaller plans on the cheap. Venture capitalists saw opportunity too. In 2002, George Soros's Soros Private Equity (which has since been spun off and renamed TowerBrook Capital Partners) bought WellCare, a small Florida operation, and began to expand it. Molina, started in 1980 by a California emergency room doctor, also began to expand out of its home state, under the leadership of the founder's son, Dr. J. Mario Molina. By 2005 all four companies had gone public. Molina has struggled, in part because California has squeezed its insurers. Amerigroup and Centene both stumbled in 2005 and had to warn that profits wouldn't meet expectations, but their stocks have still trounced the S&P 500 since their IPO dates. WellCare, which also has a high-growth Medicare business, has been a Wall Street superstar: Its stock has more than quintupled since its IPO, to just over $90. Investors and executives have made a ton of money. In August 2006, TowerBrook cashed out of the last of its $70 million investment in WellCare, reaping a total of almost $900 million. Since WellCare's IPO, CEO Doug Farha has sold over $37 million of stock, according to Thomson Financial. He still owns shares worth almost $100 million and has collected $3.5 million in cash compensation over the past four years. McWaters has received $6.5 million in cash over that period. He owns almost $25 million in stock. Centene's CEO, Michael Neidorff, has also gotten $6.75 million in cash and big helpings of stock, including a grant worth $24.6 million in November 2004. |

Sponsors

|