CNN values your feedback

1. How relevant is this ad to you?

2. Did you encounter any technical issues?

Video player was slow to load content

Video content never loaded

Ad froze or did not finish loading

Video content did not start after ad

Audio on ad was too loud

Other issues

Ad never loaded

Ad prevented/slowed the page from loading

Content moved around while ad loaded

Ad was repetitive to ads I've seen previously

Other issues

Cancel

Submit

Thank You!

Your effort and contribution in providing this feedback is much appreciated.

Close

Ad Feedback

Close icon

Business

Markets

Tech

Media

Calculators

Videos

More

Markets

Tech

Media

Calculators

Videos

Watch

Listen

Live TV

Sign in

My Account

Settings

Topics You Follow

Sign Out

Your CNN account

Sign in to your CNN account

Sign in

My Account

Settings

Topics You Follow

Sign Out

Your CNN account

Sign in to your CNN account

Live TV

Listen

Watch

Edition

US

International

Arabic

Español

Edition

US

International

Arabic

Español

Markets

Tech

Media

Calculators

Videos

Follow CNN Business

US

Crime + Justice

Energy + Environment

Extreme Weather

Space + Science

World

Africa

Americas

Asia

Australia

China

Europe

India

Middle East

United Kingdom

Politics

SCOTUS

Congress

Facts First

2024 Elections

Business

Tech

Media

Calculators

Video

Markets

Pre-markets

After-Hours

Market Movers

Fear & Greed

World Markets

Investing

Markets Now

Before the Bell

Nightcap

Opinion

Political Op-Eds

Social Commentary

Health

Life, But Better

Fitness

Food

Sleep

Mindfulness

Relationships

Entertainment

Movies

Television

Celebrity

Tech

Innovate

Gadget

Foreseeable Future

Mission: Ahead

Upstarts

Work Transformed

Innovative Cities

Style

Arts

Design

Fashion

Architecture

Luxury

Beauty

Video

Travel

Destinations

Food & Drink

Stay

Videos

Sports

Pro Football

College Football

Basketball

Baseball

Soccer

Olympics

Hockey

Watch

Live TV

CNN Headlines

CNN Shorts

Shows A-Z

CNN10

CNN Max

CNN TV Schedules

Listen

CNN 5 Things

Chasing Life with Dr. Sanjay Gupta

The Assignment with Audie Cornish

One Thing

Tug of War

CNN Political Briefing

The Axe Files

All There Is with Anderson Cooper

All CNN Audio podcasts

CNN Underscored

Electronics

Fashion

Beauty

Health & Fitness

Home

Reviews

Deals

Money

Gifts

Travel

Outdoors

Pets

CNN Store

Coupons

Target

Kohl’s

Wayfair

Chewy

Shein

Weather

Climate

Storm Tracker

Wildfire Tracker

Video

Ukraine-Russia War

Israel-Hamas War

About CNN

Photos

Investigations

CNN Profiles

CNN Leadership

CNN Newsletters

Work for CNN

Markets

DOW

S&P 500

NASDAQ

Hot Stocks

Fear & Greed Index

-----

is driving the US market

Latest Market News

Following exchange with Caitlin Clark at news conference, columnist won’t cover Indiana Fever games

Disney just had its worst day in a year and a half

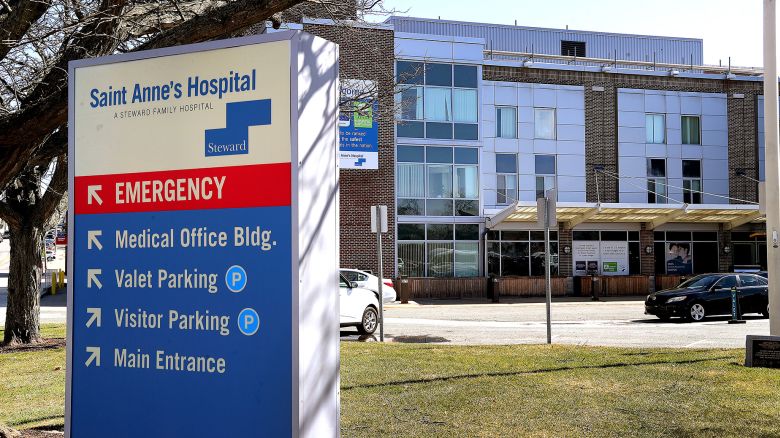

Bankrupt Steward Health puts its hospitals up for sale, discloses $9 billion in debt

Hot Stocks

Something isn't loading properly. Please check back later.

Ad Feedback

Gregory Shamus/Getty Images

Following exchange with Caitlin Clark at news conference, columnist won’t cover Indiana Fever games

Phil Barker/Future Publishing/Getty Images

Disney just had its worst day in a year and a half

John Tlumacki/The Boston Globe/Getty Images/FILE

Bankrupt Steward Health puts its hospitals up for sale, discloses $9 billion in debt

Cooper Neill/Getty Images/File

‘Draw a line in the sand, but don’t draw a swastika,’ Kraft foundation tells campus protesters

Al Drago/Bloomberg via Getty Images

Slaughterhouse cleaning company fined $649,000 for child workers

Charly Triballeau/AFP/Getty Images

Trump-appointed judges say they’ll boycott Columbia grads over university’s handling of protests

Jaap Arriens/NurPhoto via Getty Images

TikTok sues to block prospective US app ban

Justin Sullivan/Getty Images

Panera is dropping Charged Lemonade, the subject of multiple wrongful death lawsuits

David Dee Delgado/Reuters

Columbia’s student journalists produced New York magazine’s cover story. Here’s how they did it

Mario Tama/Getty Images/File

Apple unveils new iPad Pro with ‘outrageously powerful’ AI-powered chip

The new Swiss Army Knife will be missing a key feature

Fender benders mean serious high-tech repairs now

It’s a presidential election year. Here’s what that could mean for your 401(k)

The alleged architect of a multibillion-dollar fraud that shook Wall Street heads to trial

Europe risks losing its biggest oil companies to America

Americans have spent their savings. Economists worry about what comes next

UBS makes first profit since Credit Suisse rescue

Elizabeth Holmes shaves more time off her sentence

Nintendo says Switch successor will be unveiled by March 2025

Kremlin critic Kara-Murza wins Pulitzer Prize for columns written from prison cell

FAA opens new probe into Boeing, this time involving 787 Dreamliner inspections

When grief and AI collide: These people are communicating with the dead

Warren Buffett compares AI to nuclear weapons in stark warning

Ad Feedback

Quote Search

Market Movers

ACTIVES

GAINERS

LOSERS

$ Price

% Change

Ad Feedback

What to Watch

•

Video

1:49

Video

‘SNL’ takes on the college campus protests

1:49

•

Video

3:02

Video

CARE CEO fights global poverty

3:02

•

Video

3:03

Video

Is ‘giving back’ in your work ethic?

3:03

•

Video

5:10

Video

Riding South Africa’s EV boom

5:10

Ad Feedback

In Case You Missed It

Justin Sullivan/Getty Images/File

What to expect in Friday’s jobs report

Peloton cuts jobs and is looking for a new CEO after its turnaround plan spins out

Sell in May and go away? Think again

ABC News president Kim Godwin in hot water as Disney-appointed boss conducts review

Al Drago/Bloomberg/Getty Images

Key takeaways from the latest Fed meeting

Americans were paid an additional $235 billion in interest in 2023, thanks to the Fed

Former Google workers fired for protesting Israel deal file complaint claiming protected speech

Binance founder is sentenced to 4 months in prison on money-laundering violations

Ad Feedback

Ad Feedback

More from Video

•

Video

2:32

Natalia V. Osipova

This glass could turn skyscrapers into power generators

2:32

•

Video

8:10

Coastal life and ranches: A different side to Abu Dhabi

8:10

•

Video

4:54

Weaving the future of South Africa’s wool industry

4:54

•

Video

2:30

CNN

‘If you can afford to buy, you always buy,’ says Suze Orman

2:30

•

Video

2:37

John General, CNN

Salad restaurant shows CNN why it scans its employees’ hands

2:37

Success

mapodile/E+/Getty Images

How to make high interest rates work for your hard-earned savings

Michael Nagle/Bloomberg/Getty Images

The average Wall Street bonus dipped 2% last year, to $176,500

PeopleImages/iStockphoto/Getty Images

The average tax refund is over $3,000. Here are 7 ways to put it to good use

FS Productions/Tetra images RF/Getty Images

March 12 marks Equal Pay Day this year

Tech

Bing Guan/Bloomberg/Getty Images

FTC investigating TikTok over privacy and security

Philip Pacheco/Bloomberg via Getty Images

Apple announces its annual developers conference is set for June 10

Kirsty Wigglesworth/Pool/Reuters/FILE

Judge’s stern rebuke of Elon Musk’s X gives researchers fresh hope

Michael Kappeler/dpa/picture-alliance/Sipa

3 ways Apple’s monopoly lawsuit could change the iPhone experience for fans

Media

Michael M. Santiago/Getty Images

NBC cut ties with Ronna McDaniel after extraordinary pressure, but its problems aren’t over

Mandel Ngan/AFP/Getty Images

NBC News ousts Ronna McDaniel after network’s anchors launch unprecedented on-air rebellion

Melina Mara/The Washington Post/Getty Images

NBC News boss Cesar Conde faces backlash from his network’s anchors over ‘inexplicable’ decision to hire ex-RNC chair Ronna McDaniel

Mike Segar/Reuters

NBC hires former RNC chair Ronna McDaniel, who has demonized the press and refused to acknowledge Biden was fairly elected

Un

derscored Money

Kyodo News Stills/Getty Images

10 great ways to travel for free with 75,000 Chase Ultimate Rewards points

Getty Images/iStockphoto

Bilt’s May Rent Day promotion: Redeem points toward rent, get free home decor

Delta Air Lines

Your ultimate guide to the American Express Membership Rewards program

iStock

It’s back: Targeted Amex card holders can get up to 30% off at Amazon

Sum Vivas

Digital humans: the relatable face of artificial intelligence?

Top soccer clubs are using an AI-powered app to scout future stars

Why lab-grown diamond sales are surging

The Chevrolet Corvette is officially going electric

Joel Saget/AFP/Getty Images

OpenAI’s wild week. How the Sam Altman story unfolded

Sam Altman returns to OpenAI in a bizarre reversal of fortunes

Opinion: The drama around Sam Altman is an urgent warning

Microsoft stock hits all-time high after hiring former OpenAI CEO Sam Altman

Paid Partner Content