|

Your home as a tax shelter

|

|

May 19, 1999: 7:14 a.m. ET

Whether buying or selling, deductions ease homeowning's financial burden

|

NEW YORK (CNNfn) - You buy a home to protect you and your family from snow and rain, but it can protect you from some of your taxes as well -- as long as you know all the ins and outs.

And whether you're buying or selling your home, you can make sure you're getting all the tax benefits you can.

If you're buying a house for the first time, the Internal Revenue Service gives you a little extra help to get over the bumps, provided you qualify.

Chief among them is the mortgage interest credit. This is offered to first-time home buyers with income below the median income for the area where they're moving.

Start out by getting a mortgage credit certificate (MCC) from your state or local government. The agency will usually only give you one if you're in the process of getting a new mortgage for the purchase of your home.

This form will give you your "certified indebtedness amount," which will tell you how much interest on your loan is eligible for the credit.

Once you have that figure, you can begin your computations according to the IRS formula.

Assume that you have a mortgage loan of $100,000 and you are told your certified indebtedness is $80,000, or 80 percent of your overall mortgage.

If you paid $8,000 in interest during the year, you would multiply $8,000 by .80 to get a mortgage interest credit of $6,400. As usual, the IRS rules have many restrictions, so make sure you get all the details before you apply for this credit.

When you are dealing with any kind of mortgage interest deductions, you must itemize your return using IRS Schedule A (Form 1040). In addition, to claim the mortgage interest credit you will need Form 8396, which you can download online.

Housewarming deduction

Perhaps no tax break is more beloved to U.S. homeowners than the home mortgage interest deduction. The deduction is not without its detractors, who refer to it as "middle class welfare," but homeowners are well advised to make the most of it.

Essentially, the home mortgage interest deduction cuts you a break on paying for your home, according to Barbara Raasch, partner at Ernst & Young.

"If you borrow from a bank to buy a house and it is less than $1 million, you can deduct the interest," said Raasch.

Remember you will need to itemize your deductions using Schedule A (Form 1040) in order to get this deduction.

The deduction works like this. First, you can only deduct the interest if your mortgage is a secured debt -- meaning, among other things, that if you default, the sale of your home would cover the debt.

The second specification is that your home must be "qualified." This means that it must be your primary residence or a second home, which could be a mobile home or even a boat, as long as it has sleeping, cooking and toilet facilities.

In addition, you can take the deduction even if your home doesn't completely exist yet. According to the IRS, you can treat a home under construction as a qualified home for as much as 24 months.

You can rent out your second home and still claim the deduction, but you have to live in it part of the year to do so. Fortunately, this time is nominal, just more than 14 days or 10 percent of the number of days per year the home is rented out.

Since points can be a major part of the purchase of a home, the IRS has taken this into account as well.

Points, charges paid by a borrower when getting a mortgage, are treated a little differently than the interest paid on a the same mortgage.

If the points are used for the mortgage for your primary residence, they are fully deductible in the year they are paid.

But Raasch said a second home is a little different.

"Those points are amortized over the entire term of the note," said Raasch, who explained that if the mortgage has a term of 30 years, you could only deduct 1/30 of the points each year.

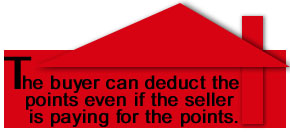

Interestingly enough, it doesn't matter who pays for the points, according to Robert Mason, a certified financial planner at Financial Planning Resources Inc. in Chandler, Ariz.

"Even if the seller pays for the points, those points are tax deductible to the buyer, said Mason.

"The IRS relented on this because the buyer is really paying those points in an indirect way since most sellers, if they're going to pay points, reflect that in a higher asking price."

You won't necessarily need to keep track of the interest you've paid over the year -- although it's a good idea -- to know how much you can deduct.

By Jan. 31 of the following year, you should receive a Form 1098 from your mortgage holder.

Similar to the W-2 form you receive from your employer outlining what you paid in taxes the previous year, Form 1098 will tell you the total interest you have paid and, if you purchased a home during the year, it will tell you what points are deductible.

You'll take the figure from Form 1098 and enter it on line 10 of your Schedule A, deducting it from your overall tax burden.

After the move

After you've moved into your new home, other deductions are available to you, according to Raasch of Ernst & Young.

If you borrow to acquire something for your house, such as furniture, the interest on that loan is deductible as well, up to a total loan limit of $100,000.

Additionally, if you have a mortgage secured by a qualified home you can treat it just like it was used to buy the home, even if you use the loan for home improvements.

In this way, you can still deduct the interest and points using Form 1040 Schedule A.

There are restrictions. The home improvements must qualify as "substantial improvements" in order to get the deductions.

The IRS defines a substantial improvement as one which adds to the value of your home, prolongs its usefulness or adapts your home to new uses.

The distinctions can be quite finite. Simply repainting the exterior of your home is not a substantial improvement by itself, but if it is done as part of an overall renovation, you can include these costs.

Finally, when it comes time to sell your house you can escape some taxation as well.

The IRS lets you exclude the gain you make from the sale of your house from taxes up to a point. If you are single you can exclude a profit of up to $250,000 or $500,000 if you are married and filing jointly.

To get the full effect of this break, you must have lived in your home for two of the past five years. But even if you haven't, you can get a partial exclusion of some of your home profits.

All of these homeowners' tax breaks come with restrictions, some of which are quite complex, so make sure you understand all the rules before you use these deductions and credits on your tax form.

-- by staff writer Randall J. Schultz

|

|

|

|

|

|

|