|

What lies ahead for Fed?

|

|

January 31, 2000: 5:21 p.m. ET

As the economy bounds into record books, will a tap on the brakes keep the good times rolling?

By Staff Writer M. Corey Goldman

|

NEW YORK (CNNfn) - As the U.S. economy leaps and bounds its way into a record 107-months of uninterrupted growth, members of the Federal Reserve's policy-setting team meet Tuesday to decide whether the economy needs a gentle tap on the brakes or a quick downshift.

More so than in any other decade, the U.S. economy is on a prosperity tear. Annual growth is above 4 percent. Unemployment is at a generation low. Prices for goods and services are stable and, thanks to technology and global competition, falling in many instances. Record stock market gains and rising real estate values in 1999 have given consumers more room than ever to live well and indulge. In short, the economy is good.

At the same time -- literally -- the central bank is considering taking away the punch bowl, raising short-term interest rates to discourage consumers and businesses from borrowing -- and spending -- too much money. The Fed's Open Market Committee meets on Tuesday and Wednesday. A decision on interest rates is expected Wednesday afternoon.

What do you think the Fed will do? Take our poll.

According to a CNNfn.com poll of 15 major banks and brokerages, the unanimous opinion is the Fed will opt for the gentle tap on the brakes for now.

"The Fed wants the economy to keep churning out steady, consistent growth for as long as possible -- that's their No. 1 objective," said Doug Porter, a senior economist with brokerage Nesbitt Burns Inc. "They have made it very clear that they don't want to snuff out the expansion."

No slowing down

Most economists agree that the buoyant economy is in no danger of being snuffed out in the next few months, even as the tech-heavy Nasdaq stock exchange nears a correction phase and other equity markets gyrate wildly. A recession, according to textbook economic theory, is two consecutive quarters where an economy contracts, rather than grows.

What could lead to the end of the expansion and the beginning of a recession is if the Fed and Chairman Alan Greenspan do nothing to curb the cost of borrowing for consumers and businesses -- something they can do by raising or lowering a target interest rate they enforce called the Fed funds rate.

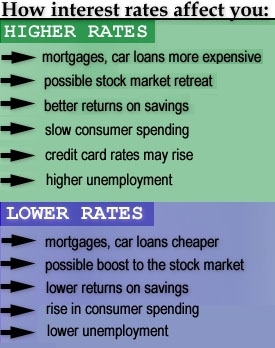

The Fed funds rate is the target rate banks lend money to each other overnight. It sets the trend for lending rates on everything from personal lines of credit to auto loans to credit card interest. The rate was last lifted Nov. 16 by a quarter-point to 5.5 percent, the third increase of 1999. The Fed funds rate is the target rate banks lend money to each other overnight. It sets the trend for lending rates on everything from personal lines of credit to auto loans to credit card interest. The rate was last lifted Nov. 16 by a quarter-point to 5.5 percent, the third increase of 1999.

To be sure, there's no steadfast rule that says the Fed's policy setting arm, the Federal Open Market Committee, is required to raise rates in quarter point intervals, or that they have to do it at the conclusion of a Fed meeting. The Fed meets eight times a year at its Washington headquarters.

Of particular note this time around is how the Fed outlines the risks to the economy. Earlier this year the central bank said it would no longer disclose which way it was leaning on interest rates - known as the Fed's bias. Instead, the central bank will comment on the risks of heightened inflation pressures or economic weakness in the foreseeable future.

One lump or two?

And some economists aren't ruling out a half-point increase in interest rates at the conclusion of Wednesday's meeting, firing a warning shot to financial markets that it is very concerned about the rapid pace of growth. On Friday, the Labor Department reported that they economy grew at a 5.8 percent pace in the fourth quarter, its strongest showing of the year.

"If I had to say there was a risk, it would be that they'll move 50 basis points -- I wouldn't rule that out completely," Porter said. Because the Fed hasn't raised or lowered interest rates in anything but quarter-point intervals since 1995, "many people find it difficult to stick to that kind of prediction."

Still others, including Daiwa Securities Chief Economist Michael Moran are predicting that rates will continue to rise beyond next week's meeting. Moran told CNNfn that he's expecting the Fed funds rate to rise to 6-1/2 percent by the end of the year. (369KB WAV) (369K AIFF)

"If you look at the momentum that the economy has had coming into the year 2000 and if you look at the very small effect that tightening has had so far on the economy I think there is a distinct possibility that we could see four tightening moves, all a quarter of a percentage point," Moran said.

Still no inflation

Much of that momentum has come from voracious U.S. consumers who, despite three rate increases from the Fed, haven't learned to keep their wallets and checkbooks in their pockets. Earlier Monday the Commerce Department reported that Americans' spending rose almost twice as fast as incomes in December, while personal savings fell to an all-time low.

Of course, one of the main missing ingredients in the Fed's battle against inflation is -- inflation. With the exception things like oil and natural gas, prices for computers, wireless phones, DVD players and other products have actually declined. Higher productivity and fierce competition have kept retailers from raising prices, but still allowed them to produce profits.

Some evidence of inflation did surface last week after the government reported that fourth-quarter labor costs and prices both rose at a stronger-than-expected pace. Those numbers suggested that the robust U.S. job market just may be starting to spur employers to dish out higher salaries and benefits, putting cash in consumers' wallets.

"If inflation is around the corner, the Fed doesn't want to meet it -- it wants to kill it before it gets around the corner," said Richard Babson, president of Babson-United Investment Advisors in Boston. "The Fed wants to make sure that there are no significant cost pressures in the economy."

Getting out of debt

Whether the economy needs to be tinkered with to slow it down, or whether gains in technology and productivity can allow growth to continue without fueling an increase in prices is the great debate, both on Wall Street and Main Street. That aside, one threat to the U.S. economic expansion does seem clear: growing debt levels.

Private-sector debt, according to the Commerce Department, is at the highest levels since the mid-80s. While it's not the same as 1987, when the stock market crash led to a savings and loans debt crisis, it could potentially wreak havoc on the economy if people and business are suddenly forced to repay loans with money they no longer have, Babson said.

Speaking Monday at the World Economic Forum in Davos, Switzerland, Securities and Exchange Commission Chairman Arthur Levitt expressed his views about rising debt levels among Americans. (324KB WAV) (324KB AIFF) U.S. Treasury Secretary Lawrence Summers expressed his own feelings on the subject Saturday, suggesting a heightened level of national savings was needed to further prolong the current expansion.

That's why the Fed is taking steps now to slow things down, likely raising the Fed funds rate in steady, quarter point increments to avoid causing a significant reaction either within the economy or within financial markets.

"I don't think you will see the Fed jumping to interest rates," George Soros

Chairman, Soros Fund Management, told CNNfn in Davos. "Most likely they will raise in quarter percent installments, wait a little bit and then raise it again."

|

|

|

|

|

|

Federal Reserve

|

Note: Pages will open in a new browser window

External sites are not endorsed by CNNmoney

|

|

|

|

|

|