Prices aren't going up very much. Should we celebrate?

Not really. Inflation that's too low could be a bad sign for the U.S. economy, and some Federal Reserve officials are starting to get concerned.

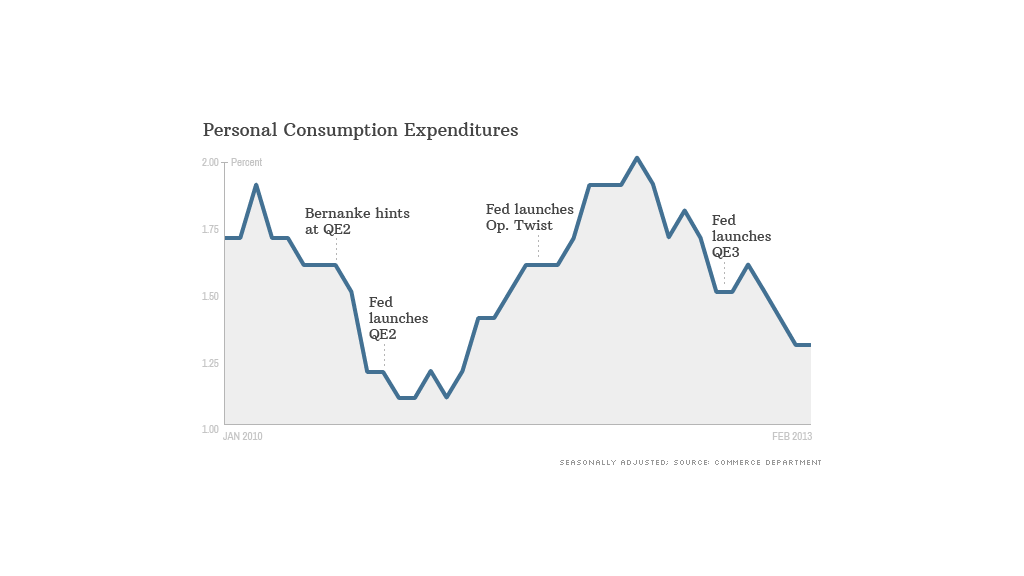

Speaking to reporters on Wednesday, St. Louis Fed President James Bullard pointed to the Fed's preferred measure of inflation -- personal consumption expenditures, minus food and energy -- which recently has shown that prices are up 1.3% over a year ago.

"That's pretty low," Bullard said at a Levy Economics Institute event. "I'm getting concerned about that, and I think that gives the FOMC some room to maneuver on its monetary policy."

The Fed typically aims to keep inflation around 2% a year. Inflation at that level is considered healthy, coinciding with solid economic growth, a growing job market and gradually rising wages.

"Economic history has shown that economies perform best with slightly higher levels of inflation, such as 2% to 3%," said Bernard Baumohl, chief global economist for the Economic Outlook Group. "Low and dormant inflation translates into a dormant economy."

Why is low inflation bad? There are a few key reasons.

First, when companies don't have any leeway to raise prices, they're more apt to cut costs, which could mean a cutback in hiring. Second, if inflation remains so low, consumers are not as motivated to rush out and spend, Baumohl said.

Third, when inflation is low, it doesn't offer a large buffer against deflation if an economic shock occurs. Deflation -- when prices fall -- often freezes up spending, because who wants to go out and buy an item now, if they expect it to be cheaper in six months?

Related: The geeky debt fix that might work

And fourth, low inflation often comes along with lower wage and revenue growth.

Even with the recent low inflation data, Bullard's comments Wednesday came as a bit of a surprise to Fed watchers. For one, most Fed criticism lately has focused on how the central bank's unprecedented push to stimulate the U.S. economy could eventually lead to rapid inflation or asset bubbles. Fed policies are already cited as a key reason why stocks have recently hovered near five-year highs.

Second, Bullard is known for leaning slightly hawkish. Just minutes before he met with reporters Wednesday, he gave a speech arguing that the Fed's stimulative policies probably won't solve the job market's problems.

"I found Bullard's comments yesterday the most interesting in some time," said Ellen Zentner, senior economist for Nomura. "It suggests that other hawks could follow suit if lower inflation persists."

The Fed has kept its key short-term interest rate near zero since 2008. When that wasn't enough to boost the U.S. economy, it launched several bond-buying sprees, known as quantitative easing, in an attempt to lower long-term interest rates.

The Fed is now running its third such round of asset purchases, buying $85 billion in Treasuries and mortgage-backed securities each month.

The program remains highly controversial, and most of the conversation lately has been speculation about when the Fed will start tapering off, and eventually ending, those bond buys.

But on Wednesday, Bullard went so far as to say that if the inflation rate falls further, the Fed may have to think about increasing its monthly asset purchases, rather than winding them down anytime soon.

His colleague, Minneapolis Fed President Narayana Kocherlakota, backed that sentiment Thursday.

Kocherlakota is considered a Fed dove and has long favored stimulus, but if inflation was to fall even further, he said "that would make me in favor of even more accommodation," he told reporters.

Bullard is a voting member on the Fed's policymaking committee this year, but Kocherlakota is not. Even so, if low inflation persists, expect to hear more Fed officials discuss the issue in the months ahead.