U.S. savings bonds, a graduation gift staple for nearly a century, are on the verge of extinction.

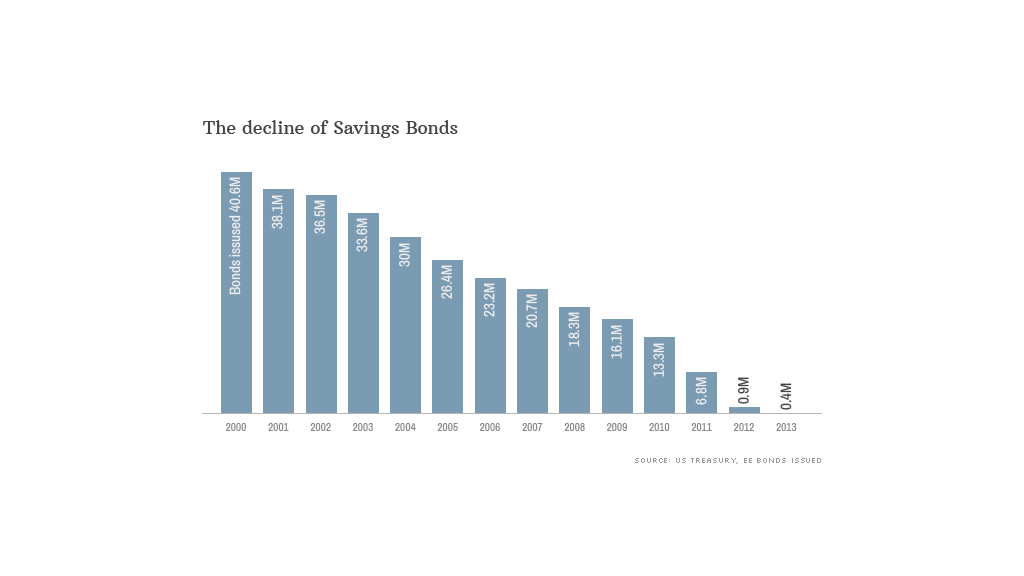

Americans bought over 40 million of the most popular savings bonds in 2000. Last year, the U.S. sold a mere 400,000 of them.

They were often given to students, newly married couples or anyone having a birthday. It was akin to gifting cash, but better. The bond certificate looked extra official, and it encouraged young people to save for the future -- whether for further study, a car or a house.

Savings bonds offer some interest each year -- much like money held in a bank's savings account -- but if you hold the bond to the end of the 10 to 30 year duration, you often make more money due to various adjustment procedures. It's akin to a bonus payment.

But these bonds are going the way of the landline telephone, and there are several reasons why.

For starters, savings bonds, which have been around since the 1930s, are no longer an attractive investment.

Related: Investors chase higher yields in scary places

"The interest rates are so low these days that people just don't even get involved in them anymore," says Jim Moore, a Wells Fargo financial advisor based in St. Louis.

The fixed-rate "EE" bond offers a mere 0.5% interest rate for the next 20 years, barely better than putting money under a mattress. Bonds issued at the end of last year were yielding an even more lousy 0.1% rate.

Moore recommends buying a good quality, high paying dividend stock or exploring other savings options instead. Many parents and grandparents utilize 529 savings plans for colleges that are run at the state level. Investment growth in a 529 plan is tax deferred, and any money taken from the 529 to pay for college isn't taxed at the federal level.

Related: Tax-savvy college savings options

But it's the Internet that really killed off demand for savings bonds.

You can no longer buy a paper savings bond. On January 1, 2012, the government stopped sales of over-the-counter paper bonds and forced people to buy them online via TreasuryDirect.

That's when the big plummet occurred. The goal was to save money, but in the process, the government made it harder for potential buyers.

Many older Americans were raised on ads to be patriotic and buy these bonds to help the country (and yourself). There were slogans such as "Back Your Future." The savings bonds were sold in many places, including local banks and brokerages.

Now you have to go online and fill out cumbersome forms with your taxpayer ID number, the intended recipient's Social Security number, your bank account and other information. It's even more complex if you try to gift a savings bond to someone under 18.

Related: Fewer students have jobs on graduation day

Kate Warne, investment strategist for Edward Jones, says the only time she hears about savings bonds these days is from clients telling her how hard the website is to navigate.

"The complaint I get is 'I have trouble. What should I do instead?'" Warne says.

Those formal looking certificates that made such lovely accompaniments to graduation degrees are history. The only way to get one now is to ask for your federal tax refund to be returned to you as savings bonds.

Even that is convoluted. The bonds are only issued in $50 increments, so unless your refund is perfectly divisible by 50, you get savings bonds plus a check for the difference. It's a small program according to the Treasury Department.

The government has no plans to revive paper savings bond sales. There is a mock certificate people can print out online to wrap up in a box and give as a gift. But that just doesn't have the same appeal.