Real tax reform remains a very big IF. But ... if ... Congress and the Trump administration slash rates and overhaul the tax code, most itemized deductions taxpayers can claim on their tax returns would probably go away.

Why? Because both the White House and House Republicans have proposed getting rid of them except those for mortgage interest and charitable contributions.

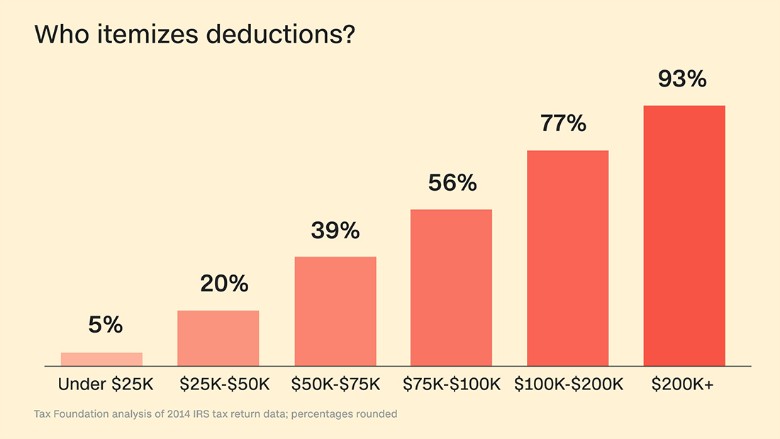

Such a change would affect the 30% of federal tax filers who today choose to itemize because their deductions combined exceed the value of their standard deduction (currently, $6,300 for single filers and $12,600 for joint filers).

The vast majority of households making more than $200,000 itemize. And high-income filers get the most value from itemized deductions.

Nevertheless, there's a notable number of itemizers farther down the income scale as well. The Tax Foundation found that itemizers include: 39% of those with adjusted gross incomes between $50,000 and $75,000; 56% of those with AGIs of $75,000 to $100,000, and close to 77% of filers making between $100,000 and $200,000.

Any tax reform the current Congress might pass could entail a big cut in rates and a larger standard deduction. Details are still not set.

Treasury Secretary Steven Mnuchin has said eliminating most itemized deductions would help ensure the rich don't get much, if any, of a net tax cut. But killing itemized deductions would affect a lot of filers in the middle and upper-middle income ranges, too.

Here are some key deductions that could get the ax.

State and local tax deduction

Itemizers are allowed to write off their state and local income taxes or general sales taxes, plus their property taxes. This is largest itemized deduction for all itemizers, who typically live in high-tax states such as New York and California.

There is, however, resistance to getting rid of this deduction from lawmakers in states most affected by it.

Medical expenses

Today you may deduct the amount of your medical expenses that exceed 10% of your adjusted gross income. That's a tough threshold for most people to meet in any given year. The Joint Committee on Taxation estimates that just 4% of households claim it and their average savings from it amount to less than $1,500 per return.

While tax reform proposals would get rid of this deduction, Republican bills in the House and Senate to repeal-and-replace Obamacare would preserve it and lower the threshold for eligibility.

Investment interest

While interest payments on personal debt (such as credit cards and car loans) are not deductible, interest paid on loans for income-producing investments is.

So getting rid of that deduction would affect anyone who, for instance, buys stocks on margin, according to Steven Rosenthal, a senior fellow at the Tax Policy Center.

Those who would not be affected are those who pay interest on loans to support their businesses. That would still be deductible as a business expense on Schedule C.

Miscellaneous expenses

This is a catch-all category that includes tax preparation fees and unreimbursed employee expenses such as union dues, travel for work or job-related courses. Also: expenses for income-generating hobbies and gambling losses, among others.

So, for instance, today you may be able to deduct the cost of that business trip your employer failed to cover. That option would disappear and you'd have to fight your boss for reimbursement.

But there's a catch to such deductions: Specific rules govern whether any given expense is eligible. And you can only deduct some of the eligible miscellaneous expenses to the extent that, combined, they exceed 2% of your AGI.

Others, such as gambling losses or casualty and theft losses from income-producing properties, are not subject to the 2% threshold.