The new tax plan, enacted by one party over the other's strenuous objections, has started the United States on an economic experiment.

How much of the massive corporate tax cut will trickle down to workers and consumers? And how much of it will flow up to shareholders and other owners of companies?

There's no definitive answer. But there is a red-hot debate.

When asked on NBC News about his claim that companies will use the tax savings to help workers, House Speaker Paul Ryan cited a National Association of Manufacturers survey in which nearly 54% of respondents said they would hire more people on account of the tax cut. Another corporate group, the Business Roundtable, recently polled its member CEOs and found that only 43% are planning to hire in the next six months.

But some conservatives offer up another argument: Even if tax reform channels more money into the hands of investors, those gains will then be reinvested into other businesses.

"If a large, mature corporation returns capital to society, that is capital that can go to young, entrepreneurial folks," said White House Council of Economic Advisers chairman Kevin Hassett, at the Brookings Institution in December. "So I don't think that we should pillory firms if they increase their dividends."

The theory: If one company thinks the best use of its excess cash is to raise dividends or buy back stocks, shareholders could put that money to work again by recirculating it to other companies that need capital to expand or develop new products. And companies should be motivated to invest more, because cutting taxes increases the return on capital, thus increasing the bang for an investor's buck.

Related: Why now's not the time for expensive tax cuts

"If you lower the price of something, you get more of it," said economist John Cochrane, a senior fellow at Stanford University's right-leaning Hoover Institution. "That's pretty basic. We can argue how much more, but otherwise we're into the land of prove-the-moon-isn't-made-of-green-cheese arguments."

But that's the big unknown. How much more corporate investment can you get by cutting taxes? And is it worth sacrificing the tax revenue, which the government needs to provide services, to do it?

The research is most conclusive on what doesn't work: Temporary tax holidays, such as the one Congress granted in 2003 to companies that brought cash back from overseas. Companies that took advantage of the break repatriated $362 billion, but subsequent studies found no statistically significant impact on U.S. investment or hiring as a result.

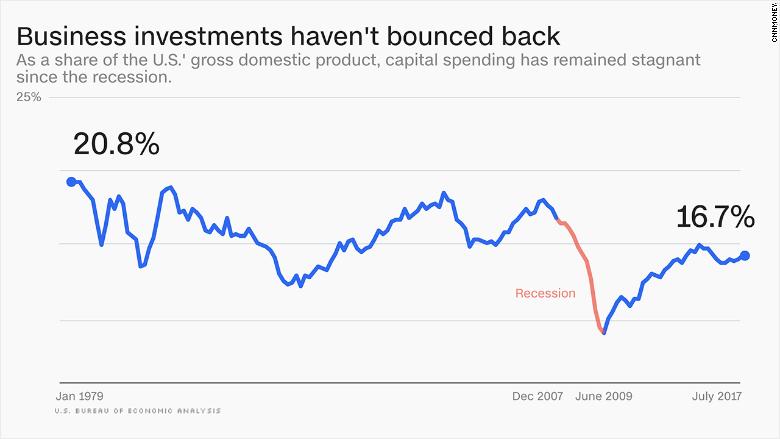

Hassett has argued that making tax cuts permanent will have a greater impact on the country's long-term competitiveness, since businesses can plan for the future. But recent research points to another complication. Corporate investment has remained depressed following the recession, despite robust profits and healthy cash reserves.

Economists aren't sure exactly why that is, but two explanations have emerged: Increasing monopoly power and weaker demand from corporations and consumers for goods and services.

On the first, a recent paper by two New York University scholars finds that industry consolidation through mergers and high barriers to entry — caused by large companies that stymie competition, as well as government regulations that startups have a tougher time navigating — are the main culprits behind low levels of investment.

Related: Will companies spend tax savings to create jobs?

On the second, Federal Deposit Insurance Corporation data shows that by and large, businesses aren't having trouble accessing capital — they just haven't been asking for it.

"We haven't seen anything in our analysis of the data to suggest that there's a supply issue on the credit side," FDIC Chairman Martin Gruenberg said in November. "The issue is really one of demand."

For that reason, some economists argue that simply giving shareholders more money won't boost investment very much at all.

J.W. Mason, an assistant professor at the City University of New York and a fellow at the left-leaning Roosevelt Institute, has calculated that in 2014, shareholder payouts amounted to $1.2 trillion, while investments by shareholders through initial public offerings and venture capital came to only about $200 billion.

In other words, bigger shareholder returns overall don't necessarily drive investment in new businesses.

"You don't usually hear businesses say 'We invest more because our shareholders are wealthier,'" Mason said. "You invest more because you see more opportunities for investment."

Mason says the best way for the federal government to increase investment is to spend money directly on infrastructure projects rather than tax cuts. That way, all of the money would go toward new jobs and capital spending, rather than being at the whim of shareholders who would decide whether to reinvest it at all.