The economy has been quiet for months now. Maybe ... too quiet.

Although most economists forecast smooth sailing for 2018, many are saying another downturn looms on the horizon. The only question is the cause — and whether it will feel like we've hit some mild headwinds, or we've run full-steam into a glacier.

"Keeping the economy on a sustainable path may become more challenging," said New York Federal Reserve Bank president William Dudley in a speech last week. "There are some significant storm clouds over the longer term."

What's lurking in those clouds? Dudley and others have identified two main threats: Rising consumer debt, and possible missteps by the Federal Reserve.

First, let's take a look at the debt threat.

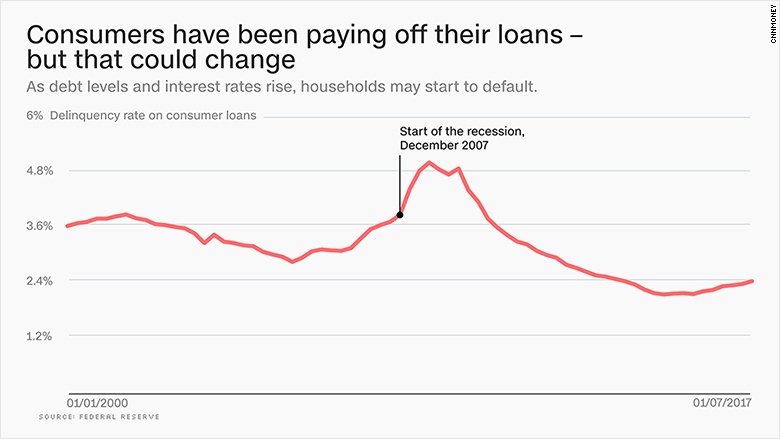

Ten years ago, a boom in lending fueled by fraudulent mortgage practices helped bring about the Great Recession. Consumers then rapidly shed their debts, either through foreclosures or bankruptcies, and very tight credit made it more difficult to borrow following the recession.

But student loans, mortgages, auto loans, credit card balances and other forms of debt have been on the rise again since early 2013, and grew to nearly $13 trillion in total this past quarter — about 2% more than their previous high in the third quarter of 2008. Debt payments as a percentage of household disposable income have also started to increase, as has the delinquency rate for consumer loans -- even though post-financial crisis regulations strengthened underwriting standards.

"The vulnerability I'm focused on when it comes to 2019, 2020 is household balance sheets," said Steven Friedman, senior economist at BNP Paribas Asset Management. "You're seeing a bottoming out of the improvement."

Related: Dow 26,000: The stock market is a runaway freight train

Families tend to take on more debt if they see their personal financial circumstances getting better, and expect that to continue in the future. With unemployment near record lows, wages have shown strong growth over the past two years.

That brings us to the second looming threat: The possibility that the economy might improve too much. In a research note published this week, economists at Goldman Sachs developed a model that uses a combination of indicators to forecast recession risk across developed economies. By their calculations, the risk of a recession starts to escalate in two to three years due to a shortage of workers, which may push up wages to the point where prices for goods and services start to spin out of control.

The Federal Reserve could then respond by hiking interest rates suddenly, which could make those household debts more expensive, leading some people to default. An abrupt rate hike could also destabilize the already-overvalued stock market.

"Historically, monetary policy has been a main cause of U.S. recessions," said Alan Auerbach, an economist at the University of California-Berkeley. "If rates are increased too quickly — something I don't currently anticipate to happen — this could occur again."

Related: What Americans can learn from cities with super-low unemployment

Although Fed chair nominee Jay Powell has said he would continue the gradual pace of interest rate hikes set by his predecessor Janet Yellen, President Donald Trump has three empty board seats to fill, which analysts say could change the Fed's stance.

Meanwhile, higher interest rates could also result from increased government borrowing, with the extra $1 trillion that the recently-passed tax cut measure is expected to add to the federal debt.

And those are just the relatively predictable risk factors. Recessions are born from a combination of underlying economic weakness and external shocks — which could take the form of a collapse in European housing markets, a nuclear crisis on the Korean Peninsula, a sudden spike in energy prices, a trade war, or something nobody sees coming yet.

"If there's a sufficiently strong signal to households, or lenders tighten up, it could all come to a head fairly quickly," said James Galbraith, a professor of government at the University of Texas' LBJ School of Public Affairs, who has studied business cycles. "Whatever will happen will probably not be something we've talked about."