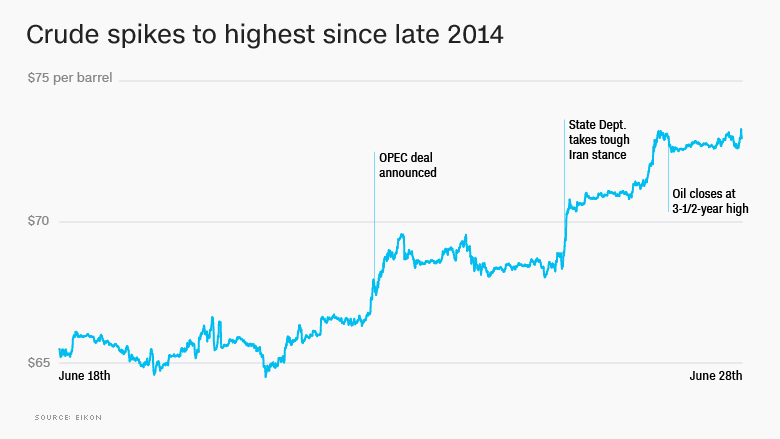

The oil market is on fire once again. On Thursday, crude spiked above $74 a barrel for the first time since late 2014.

The 13% surge over the past week has been driven by a confluence of bullish factors that will make American drivers cringe when they fill up their gas tanks.

• Saudi Arabia agreed last week to go all in with production. Investors are betting the OPEC leader has little room to respond to a future crisis.

• A major oil producer in Canada suffered a power outage, disrupting the flow of crude to the United States.

• And President Trump stepped up his crackdown on Iran, the world's fifth biggest oil producer. The State Department is now insisting that other countries stop importing Iranian oil -- or face sanctions from Washington.

The end result: US crude jumped another 1.5% on Thursday and topped $74 a barrel.

"You can't tweet about high oil prices and then apply sanctions on Iran and not expect prices to go higher," said Ben Cook, portfolio manager at BP Capital Fund Advisors. "The oil has to come from somewhere."

It's been a wild stretch for crude. Oil prices rose sharply through the spring, as production collapsed in crisis-riddled Venezuela and traders anticipated Trump's withdrawal of the United States from the Iran nuclear deal. But crude hit a wall in late May after Saudi Arabia vowed to pump more.

Related: Growing pains ripple across America's biggest oilfield

Saudi Arabia to the rescue?

OPEC and Russia reached a complicated agreement last Friday in Vienna. The group agreed to pump more oil -- but perhaps not as much as some had expected. Prices spiked after the agreement was released.

Over the weekend, Saudi Arabia sought to clear up the confusion. The leader of OPEC plans to pump a record-high 11 million barrels of oil per day in July, according to reports.

Such a bold promise from Saudi Arabia would normally hurt prices, but oil bulls saw a silver lining.

"Saudi Arabia is opening the floodgates," said Bob McNally, a former White House official who is now president of consulting firm Rapidan Energy Group. "That means there is no spare capacity in the oil market at a time when geopolitical tensions are high."

Consider that oil output has been plunging in two other OPEC members: Libya and Venezuela.

Related: India may ignore US demand to halt Iran oil imports

Limits to North American growth

The United States is already producing record amounts of oil, thanks to the booming Permian Basin of West Texas. However, that growth has its limits. The Permian Basin is grappling with shortages of talent, pipeline and supplies.

The massive supply glut that had been pressuring oil prices is gone. The Energy Department said on Wednesday that strong demand sent crude oil inventories plunging by 9.9 million barrels last week -- about four times what analysts anticipated.

Canada, another oil power, is grappling with problems of its own. A power outage last week shut down the Syncrude facility in Alberta, sidelining up to 360,000 barrels per day at the major Tar Sands producer. Suncor Energy (SU), which controls the facility, expects production to be shuttered through at least July, Reuters reported.

A Suncor spokesperson confirmed that Syncrude is not shipping any crude at this time and the facility is conducting a "comprehensive assessment" to determine when it can get back online.

Iran jitters deepen

Meanwhile, the Trump administration has caught the oil markets off guard with its aggressive stance on Iran. The State Department said on Tuesday it expects all countries to eliminate Iranian oil imports.

"We view this as one of our top national security priorities," the official told reporters on a conference call.

That's signals a shift from the Obama administration, which offered waivers to some countries when it imposed Iranian sanctions.

"This is hyper-bullish," said Mike Wittner, global head of oil research at Societe Generale. "The simple reality," he said, is that there's not enough space capacity in the world to immediately replace all of Iran's oil exports.

Of course, it's not clear if all of Iran's customers will go along with Washington's demands given their insatiable thirst for crude.

An official from India's petroleum minister suggested in an interview with CNNMoney that India may ignore the US demand. And China may not wish to do Trump any favors in the midst of a trade spat.

Still, it's clear that Trump's tough stance on Iran is coming at a difficult time. While gasoline prices have descended over the past month, they're still sitting at $2.84 a gallon, according to AAA. That's 27% higher than the same point last year.

"The Trump administration's stated desire to zero out Iranian exports creates a problem in terms of high pump prices for American consumers that Saudi Arabia cannot fix," said McNally.