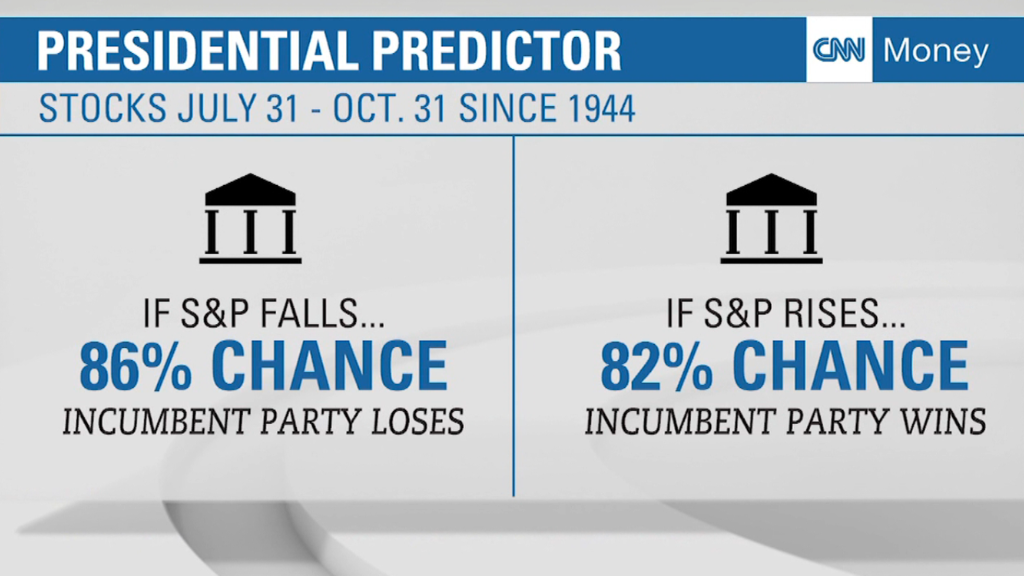

I'm afraid the stock market is going to crash after the election no matter who wins. So I'm thinking of keeping my savings in a CD for now and then possibly moving it back into the market sometime in the future. Do you think this is a good idea? --C.C., Florida

I'm not surprised that you're worried about the market as we enter the home stretch of the presidential election. After all, the prospect of a new administration with new policies naturally leads to greater uncertainty among investors and heightened concerns about how the economy and financial markets might react. That's likely why a recent Vanguard study found that stock-market volatility tends to rise in presidential election years.

What's more, when giant asset manager BlackRock polled 1,633 people earlier this year as part of its Investor Pulse survey, nearly three-quarters of those surveyed felt that volatility will increase regardless of which candidate wins the election. And a recent Edward Jones survey found that a third of Americans feel that the outcome of the election will have a negative effect on their retirement savings.

But as much as I understand your anxiety, I think you would be making a big mistake to invest based on what essentially amounts to a guess about what the market might do after November 8th.

Related: How can I grow my retirement savings without too much risk?

For one thing, while that Vanguard study shows that volatility typically rises leading up to a presidential election, it also noted that volatility tends to drop off significantly in the months afterward. There's no guarantee that the market will follow that pattern again.

Perhaps those people polled by BlackRock who expect an even jumpier market after the election will be right. Or maybe the concerns of the people surveyed by Edward Jones will turn out to be well founded and their retirement savings will fare poorly whether due to subpar returns or, as you fear, a substantial downturn after the election.

But the fact is that, election or no, there's always uncertainty about the path the financial markets will take. Sure, we can be pretty certain that at some point in the future we'll see some sort of setback just as we have many times in the past. Since 1929, we've had 20 bear markets with losses of 20% or more and 26 corrections with declines between 10% and 20%, according to this report on bear markets and corrections from Yardeni Research. But while we know such downturns are coming, we can't predict when they'll arrive.

So, while the notion that you're going to be able to move into cash or bonds before the market tanks and then jump back into stocks just as the market is ready to rebound may be enticing, it's also a fantasy. No one's timing is that good. More likely, you'll make the move to cash or bonds too soon and end up sitting in low-yielding cash or bonds while stock prices remain steady or even continue to rise.

And even if you do manage to get out of the market at the right time, there's still the question of when to get back in. Wait too long because you're not sure whether the market still has farther to fall, and you could miss out on the explosive early gains of a rally.

In short, while it's easy to know in retrospect when it made sense to exit and then re-enter the market, it's virtually impossible to pull off in real time.

Related: The problem with putting all your retirement savings in stocks

So rather than play what amounts to a guessing game, you're better off developing an investing strategy that will allow you to participate in market gains but avoid freaking out when stocks tumble.

Start by creating an appropriate cash reserve in a CD, money-market or savings account. If you're still working, that account should hold about three to six months' worth of living expenses. If you're retired, you probably want that reserve to have one to two years' worth of whatever living expenses aren't covered by Social Security and any pensions.

Whatever money remains, you then want to divvy up between stocks and bonds in a way that jibes with how long you intend to keep your money invested and your tolerance for risk. You can create such a stocks-bonds mix by going to a risk tolerance-asset allocation tool like the one Vanguard offers online.

Once you've arrived at a blend of stocks and bonds that's right for you, resist the urge to mess with it. Periodically rebalancing your portfolio or perhaps gradually shifting to a more conservative mix as you get older is okay. But don't pull money out of stocks and put it into bonds or cash because you're worried the market might tank, or do the opposite because you think stocks are going to surge. Such actions defeat the purpose of arriving at an appropriate asset allocation in the first place.

Resisting the urge to tinker with your portfolio can especially be a challenge in the time just before and after a presidential election. That's because investors are deluged with articles that suggest, or imply, that you should factor the election into your investing strategy. Some even recommend Clinton or Trump portfolios, or types of investments that are supposed to thrive depending on whether Hillary or The Donald ends up in the White House.

Read such stories for kicks if you like. But don't act on them. It might seem plausible to think you can predict which investments will do well under a particular administration. But that's an illusion. There's no guarantee that a president's proposals will make it into actual policies, and even if they do, it's difficult to know what affect, if any, they'll have on the financial markets.

Besides, lots of other factors outside the Washington beltway affect the performance of the market, specific industries and individual companies, including demographic trends, technological advances and globalization. The idea that someone is going to know which investments will excel based on what a presidential candidate claims he or she plans to do if elected to office is naive at best.

Related: How to tell if you're on track to a secure retirement

Bottom line: There are always going to be reasons to worry that the stock market might stumble, whether it's uncertainty stemming from a new occupant in the Oval Office, potential fallout from a major event like Brexit, the prospect of rising interest rates or simply the growing sense that, after seven and a half years of a bull run, stock prices are due for a correction or worse.

But the way to deal with that possibility is to create a disciplined investing strategy and stick to it, not to move your money around based on speculation and gut instinct.