1. Yuan pressure: China's yuan has fallen more than 3% against the dollar in the past two weeks as tensions between the world's two biggest economies have worsened.

The currency's decline continued on Thursday, with losses hitting 0.5%.

investors worry that new trade barriers could inflict significant damage on China's economy, which is already showing signs of slowing down. Interest rate hikes in the United States are also making dollar assets more appealing.

Chinese authorities are aware that if the yuan falls too much, it may fuel further tensions with President Donald Trump, who could renew accusations that Beijing is manipulating the currency.

Chinese stocks have also come under pressure in recent weeks. The main stock index in Shanghai shed 1% on Thursday, diving deeper into bear market territory.

2. EU summit: Immigration and Brexit will be high on the agenda when the leaders of EU nations meet Thursday in Brussels.

The bloc is expected to heap pressure on British Prime Minister Theresa May to speed up progress in the divorce negotiations. Businesses are increasingly worried about the possibility of Britain crashing out of the European Union without an agreement on trade.

3. Disney win: The US Justice Department has reached a settlement with Disney (DIS) that will allow the company to purchase most of 21st Century Fox (FOX) assets.

As part of the settlement, Disney will have to sell off 22 of Fox's regional sports networks. The settlement still has to be approved by a federal judge, and Fox shareholders also have to vote in favor of the deal.

All eyes are now on Comcast, which has tried to gatecrash the deal. The cable and media giant has not yet responded to the latest Disney offer for Fox.

Fox shares added 1.9% on Wednesday, while Disney closed 0.3% lower. Comcast (CMCSA) dropped 1.5%.

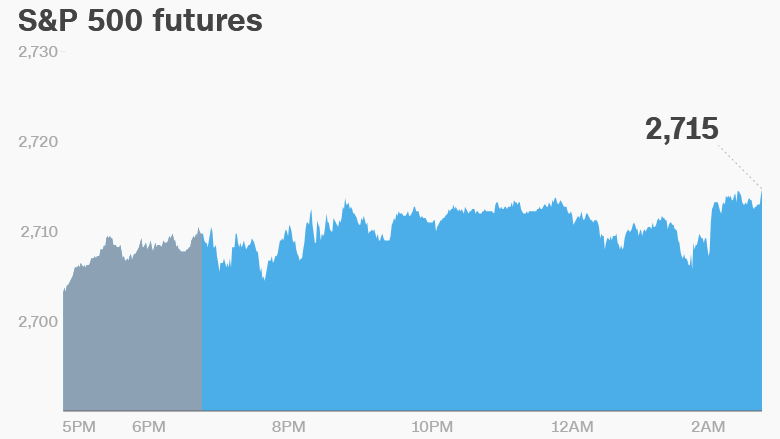

4. Global market overview: US stock futures were higher.

European markets were mixed, following the trend set in Asia.

The Dow slumped 0.7% on Wednesday, while the S&P 500 shed 0.9%. The Nasdaq dropped 1.5%.

US crude futures dipped 0.2% to trade at $72.60 per barrel. Crude prices had risen by as much as 6.4% this week because of concerns over a supply crunch.

Before the Bell newsletter: Key market news. In your inbox. Subscribe now!

5. Companies and economics: McCormick (MKC) and Walgreens Boots Alliance (WBA) will release earnings before the open. Nike (NKE) will follow after the close.

BP (BP) announced it is buying Chargemaster, the largest electric vehicle charging company in the United Kingdom. The £130 million ($170 million) deal is the oil giant's latest venture into electric vehicle sector.

H&M (HNNMY) reported disappointing first half results, revealing its after-tax profits fell by 28% compared to the same period last year. The company said it was a "tough" first half.

Shares in the fashion company were flat on Thursday, but they've fallen 20% this year.

German inflation data will be published at 8:00 a.m. ET. The third estimate of the first quarter US GDP will be released at 8:30 a.m. ET.

Markets Now newsletter: Get a global markets snapshot in your inbox every afternoon. Sign up now!

6. Coming this week:

Thursday — Nike (NKE), Walgreens Boots Alliance earnings; Foxconn (TPE) breaks ground in Wisconsin; Stress test results

Friday — University of Michigan sentiment report