|

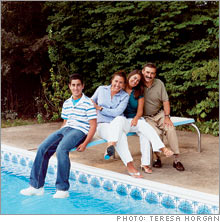

| Temprano's family was stunned by her decision to become a teacher. But they're making the sacrifices needed to support her. |

|

|

|

|

|

|

|

NEW YORK (MONEY Magazine) -

When she was a sales executive at IBM, Susana Temprano used to wake up at 6:30 a.m., drive into midtown Manhattan from her home in River Vale, N.J., blaze through e-mails and conference calls, meet with customers and, after work, entertain clients in New York City's finest restaurants. Counting bonuses and commissions, her income topped $200,000 a year.

Nowadays, Temprano rises at 5 a.m. and drives to gritty upper Manhattan, far from the city's office towers and swank restaurants. She arrives at Public School 18, where she teaches math in English and Spanish to 90 middle schoolers. She lunches at her desk, tutors kids after school, stays up until midnight grading papers and by Friday is so tired she sometimes falls asleep at the dinner table. Now in her second year as a teacher, she makes less than $40,000.

But Temprano, 43, has no regrets. "I didn't think I was using all my skills," she says of her 20-year career at IBM. "It had become just a job. Now I sing on my way to work."

Making a dream a reality

Like Temprano, a lot of us these days dream of fleeing the corporate rodent regatta and finding a career worth singing about. According to a Conference Board survey in February, only 50 percent of workers say they're satisfied with their jobs, down from 60 percent in 1995.

Unlike Temprano, however, few actually act on their dreams. Of 14,000 job changers surveyed last year by career transition consultant Right Management, only 5 percent started over in a new field. Of those who did, many wound up in teaching and nursing, where there's a shortage of people to fill the jobs.

"Education made a big difference in my life," says Temprano, the daughter of Spanish immigrants. "Becoming a teacher was a way to give back."

Still, for many executive refugees, such a move means an almost unthinkable pay cut. To make it work requires rethinking your entire financial life, from daily expenses to retirement.

When Temprano announced her plans two years ago, reactions ranged from incredulity (her office) to shock (her family). One colleague took her out for a two-hour lunch to try to talk her out of it. No way.

"They could have given me $1 million and I wouldn't have stayed," Temprano says.

Family support

Her family had even more to lose than her employer. When their two kids (Raquel, 18, and Robert, 15) were young, Temprano and her husband, Al Fernandez, now 50, decided that she would climb the corporate ladder while he took a job that left more time for family. He makes about $40,000 a year delivering bread and pastries to bakeshops and supermarkets in the early morning, allowing him time to pick up the kids from school, attend their games and help with homework.

But with the main breadwinner downshifting to a public school teacher's salary, the family faced a wrenching change in their financial outlook.

Raquel, now a sophomore at American University in Washington, D.C., was entering her senior year of high school at the time. "I was worried about how I was going to afford college," she recalls.

Fernandez blanched at the financial challenge also but says he "saw how miserable she was at IBM." Besides, Temprano had no intention of putting her career choice to a family vote.

"At the end of the day, it was my decision," she says. "I didn't even pose it to them as a question."

In June 2003 she left IBM; in December she was accepted into the New York City Teaching Fellows program, which helps career changers earn their teaching credentials. The fellowship covers all but $4,000 of the cost of a master's degree in math education, which Temprano continues to pursue in night classes three times a week.

As Temprano embarked on her new career, the family pulled together behind her. Al boosted his income by taking on more customers along his delivery route. This past summer, Raquel worked 40 hours a week at a clothing store in the local mall.

But the hardest sacrifice has been adjusting to a less affluent life. Although Temprano paid off their $160,000 mortgage with IBM stock and her commission checks shortly after leaving IBM, it's a scramble to make ends meet. Real estate taxes and upkeep still come to more than $15,000 a year, and as free cash dried up, the couple let their $900-a-year homeowners policy lapse.

Virtually all of the $70,000 that had been put aside for the kids' education went to pay for Raquel's first year at college and Robert's freshman year at a private Catholic high school. (The family did not qualify for financial aid, in part because Temprano's income from IBM the previous year was still a factor.)

Robert now goes to public school, and Temprano shops the clearance racks instead of at Saks. From time to time, frustration surfaces. When Robert learned last summer that his parents wouldn't buy him the iPod he wanted, he asked Temprano if she'd go back to IBM.

No one really wants her to give up the career she loves, of course, but Temprano does worry about the future on a household income a third of what it used to be.

"I love my job enough to teach till I'm 90," she says. "But I don't want to have to work till then."

The advice

The financial planners MONEY consulted say that Susana Temprano and Al Fernandez need to find ways not only to stretch their income to make ends meet but also to put money aside for their future. That does not mean they can skimp on financial necessities, however. They should reinstate their homeowners insurance immediately.

"Their home is their most valuable asset," says Stacy Francis, a financial planner at Francis Financial in New York City, "and they can't have it wiped out in a fire or accident."

Another immediate need: to create an emergency fund by opening a home-equity line of credit. Rates are rising but still relatively low at 6.6 percent.

"The goal is not to use it," Francis says. "But if a sudden expense comes up, it's better than running up credit-card debt."

Francis also believes that Raquel should fight for financial aid if she is turned down again.

"In about two-thirds of cases, disputing a denial of financial aid can result in more money," she says. Raquel should apply for low-interest student loans and, given her 3.4 grade point average so far, merit scholarships.

When it comes to retirement, the couple may be in better shape than today's cash flow might indicate, due to the pension Temprano is due from IBM and, eventually, from teaching. Fernandez has no retirement savings but should set up a SEP to set aside tax-deferred money. When he retires, he can sell his delivery route for about $50,000. Also, once Robert is grown, the couple could sell their home, recently valued at $800,000.

Temprano says the satisfactions of teaching make the sacrifices worthwhile. Last June, students flooded her with phone calls and thank-you notes, including a three-pager from one eighth-grader.

She can't take that appreciation to the bank, of course. But it keeps her singing on the way to work.

Look before you leap

Like a high-wire act, career change calls for steady nerves, a step-by-step approach and a safety net. Before making a move, consider:

Your mind-set

"Too many people change careers to run away from a problem in their job or personal life," says Anita Attridge, a career coach for the Five O'Clock Club, a Manhattan networking group. Perhaps you're just restless or bored. Consider asking for a new assignment or applying your established skills in a different industry.

Your finances

You'll need a cushion, be it a spouse's income, a severance package or savings. Ideally, you should have 12 to 18 months' living expenses in the bank. To make the transition easier, "downsize your spending before you make a switch," says Robert Otterbourg, author of "Switching Careers: Career Changers Tell How and Why They Did It."

Your skills

Put your toe in the water. Interested in being a chef? Work part time in a restaurant. A nurse? Volunteer in a hospital. Join a professional association and network with people in the field.

Your prospects

It's easier to switch if there's a shortage of workers in the field you want to enter. Teachers, auditors, pharmacists and nurses are in demand. Check out the Occupational Outlook Handbook on the Bureau of Labor Statistics Web site (www.bls.gov/oco). It details salaries, training programs and job prospects in a wide variety of professions.

|