Tens of millions of Americans received little financial benefit from the soaring stock market of 2013.

The country's wealthiest families typically have hundreds of thousands of dollars in stocks. Yet middle- and lower-class households typically have relatively small investments — if they have anything at all — leaving most Americans with little skin in the stock market game.

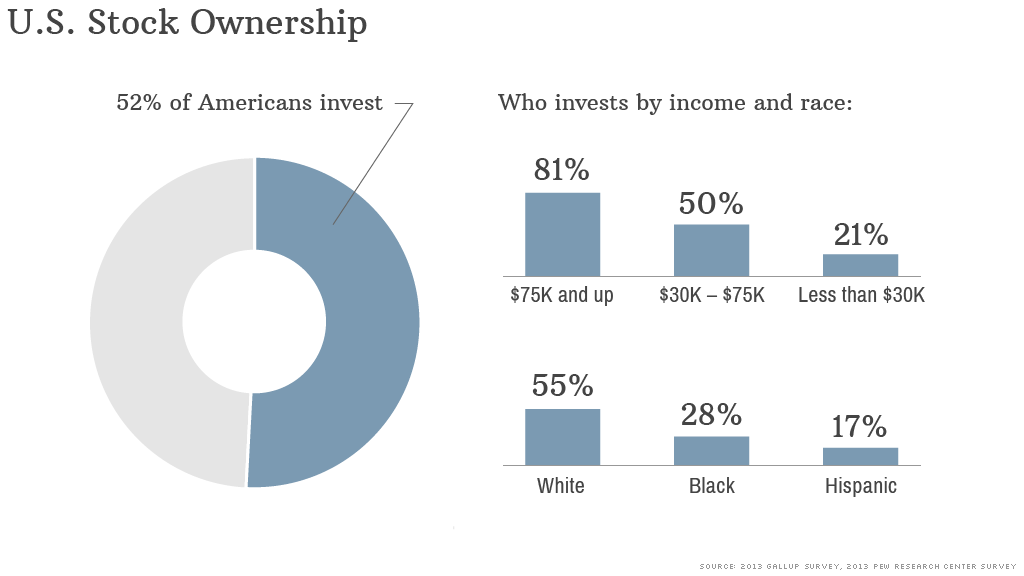

In 2013, an annual Gallup survey found that stock ownership, even in retirement accounts, had reached a record low of 52%, down from 62% five years prior.

"Although the stock market is on a tear, creating new wealth for millions currently invested in it, nearly half of U.S. adults are on the sidelines," Gallup said on its website. "That may be particularly irksome to the middle-income and young middle-aged Americans who were previously invested."

Some non-investors may indirectly benefit from an up market. For example, a pension recipient may be less likely to face benefit cuts thanks to strong returns by a pension fund. And proponents of the so-called "wealth effect" say that a soaring stock market encourages wealthy consumers to spend more, which stimulates the economy.

But overall, the effects of the bull market have likely been minimal for non-investors.

"It just doesn't have an impact for the vast majority of people," said Heidi Shierholz, an economist at the Economic Policy Institute.

Related: Many middle-class Americans plan to work until they die

Some consumers may be staying out of stocks because they fear another market crash. But in many cases, low- and middle-income Americans simply don't have any extra money to invest, she said.

More than 80% of households earning more than $75,000 a year are invested in stocks, compared to just 21% of households making less than $30,000 a year, according to the Gallup survey. Meanwhile, only 50% of those earning between $30,000 and $74,999 own stocks.

A 2013 Pew Research Center survey found that those with college degrees are significantly more likely to have money in the stock market (77%), compared to those with at most a high school diploma (25%).

Minorities are also less likely to invest: Only 17% of Hispanics and 28% of blacks have stock market investments, compared to 55% of white respondents, according to the Pew survey.

Related: The Myth of the American dream

And even of those Americans invested in the stock market, typical households have a very modest amount, said Richard Fry, a senior economist at the Pew Research Center.

In 2010, the median value of family stock investments was a mere $29,000, according to the Federal Reserve Survey of Consumer Finances, the most recent available year for that survey. Meanwhile, the top 10% of families had a median investment value of roughly $268,000.

Those figures are likely up significantly thanks to the strong market returns of the past few years. Retirement savers of all incomes have seen balances more than double in the past five years, according to an exclusive analysis of 1.4 million accounts by Fidelity Investments.

Fidelity 401(k) participants earning less than $50,000 a year had an average account balance of nearly $115,000 at the end of September, up from $45,100 at the end of 2008, Fidelity said.

The wealthiest 401(k) savers (making $150,000 a year and up) had an average balance of more than $350,000 in September, up from $145,300 at the end of 2008.

Still, economists like Fry and Shierholz say that rising home prices and an improving job market have far greater effects on most Americans than a roaring stock market.

"For the typical American household, most of their nest egg is sitting in their home..." Fry said. "They like to build their nest egg, but their sense of well-being hinges on their income."