Americans have a debt problem.

An estimated 1 in 3 adults with a credit history -- or 77 million people -- are so far behind on some of their debt payments that their account has been put "in collections."

That's a key finding from a new Urban Institute study.

It examined non-mortgage debt, including credit card bills, car loans, medical bills, child support payments and even parking tickets.

The debt in collections ranged from as little as $25 to a whopping $125,000. But the average amount owed was $5,200.

Related: Banks won't lend? Turn to these guys

Geographically, no area of the country is untouched.

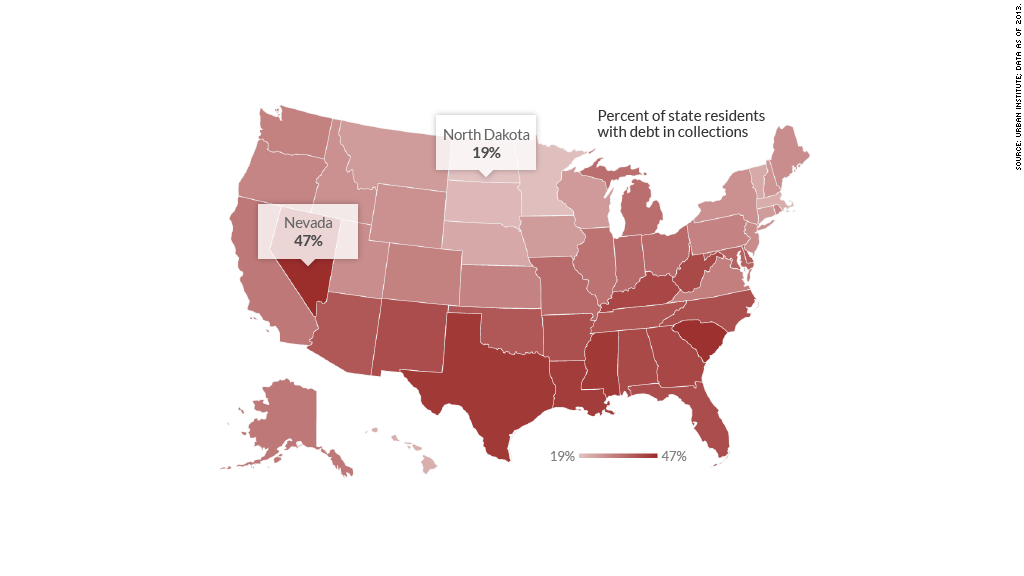

Among the states, Nevada had the highest percentage of residents with debt in collections -- 47% - as well as the highest average amount owed - $7,198. That was helped in part by the Las Vegas metro area, where 49% of residents had debt in collections.

By contrast, North Dakota had the lowest percentage of residents with debt in collections at just 19%, while the District of Columbia had the lowest average dollar amount owed per person at $3,547.

Regionally, the South had the highest percentage of people -- as high as 44% in some parts; while the Northeast had the lowest at less than 30%.

And among the 100 largest metropolitan areas, Minneapolis-St. Paul had the lowest percentage of residents with debt in collections at 20%, while McAllen, Texas claimed the highest percentage at 51%.

At least with credit cards, debt won't go into collections unless it's more than 6 months past due. But time frames can differ from place to place when talking about debt like parking tickets and medical bills.

Once it is categorized as in collections, however, it can follow one of three courses, according to the Urban Institute report. The creditor can charge it off and sell it to a debt buyer, put the account into default, or seek to collect what's owed through an in-house department or a third-party debt collector.

In any of those cases, however, the cost to the consumer is high and long-lasting.

"[It] can harm credit scores, which can tip employers' hiring decisions, restrict access to mortgages, and even increase insurance costs," said Caroline Ratcliffe, a senior fellow at the Urban Institute.

Related: 'Bad credit cost me a job'

Indeed, the case can stay on your credit report for up to 7 years even if you've paid off the debt. And it will lower your credit score for years - most dramatically when it first goes into collections status and then less so as time goes on, said a spokesman for the credit-score software company FICO.

Of course, you also do your credit score no favors when your payment is merely "past due" by 30 to 180 days. An estimated 5.3% of adults -- or 1 out of 20 with a credit file - were in this predicament in 2013, according to the Urban Institute report.

The study, conducted with Encore Capital Group, is based on a random sample of 7 million people's TransUnion credit files in 2013.