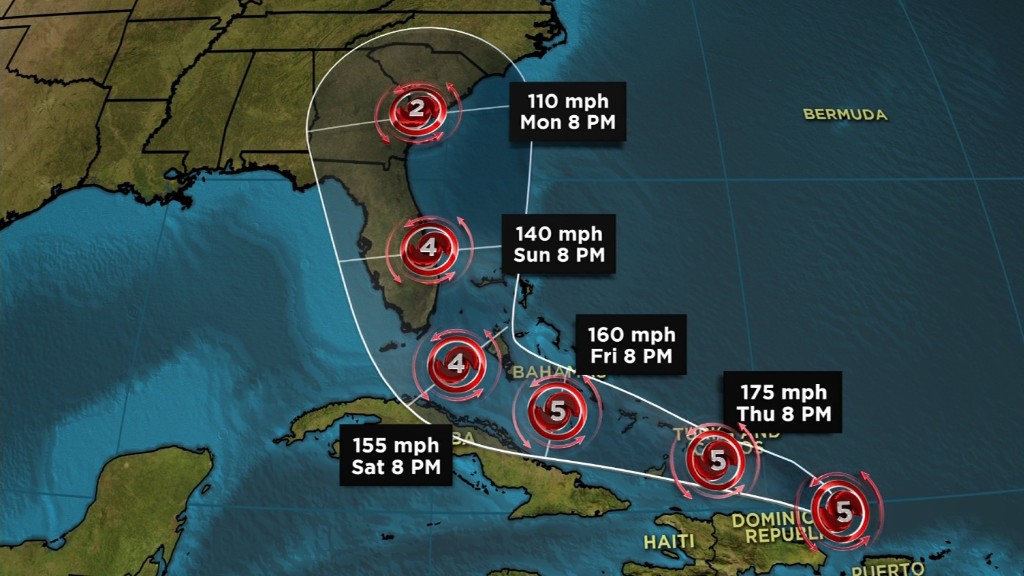

The skies have finally cleared from Harvey, but Hurricane Irma is wreaking havoc in the Caribbean and quickly heading toward Florida. Meanwhile, two other hurricanes are brewing in the Atlantic basin.

You may not be in the path of a storm now, but extreme weather events are becoming more common -- and you could one day end up facing down a powerful storm.

Once you've taken steps to ensure your family and home will stay as safe as possible, here's what you can do to protect your finances.

Secure access to important documents

If you've worked with a financial planner, you likely have access to an electronic vault. Michael Resnick, a certified financial planner with GCG Financial in Illinois, recommends uploading copies of your financial statements, insurance documents, tax returns and other important documents in addition to passports and driver's license, to that vault.

If you don't have access to a secure online storage space through a financial service, you can still put copies of your files online.

Related: What Harvey victims can do right now to protect their finances

Certified financial planner and owner of Compass Wealth Management Leslie Beck recommended scanning or taking photos of important documents and uploading them to the cloud. "Making a copy on a password-protected jump drive that you take with you is also a good idea," she added.

You can also store physical copies of your documents in a safe deposit box at your bank.

Take photos of your home

Shoot video and take photos of the interior and exterior of your home and upload those to the cloud as well. Pre-storm photos will be useful in filing an insurance claim if your property is damaged.

Interior photos can also be used to make an inventory of your belongings. Mychal Eagleson, a certified financial planner and president and founder of An Exceptional Life Financial, said an inventory "should include the date of purchase, original cost, serial number, a picture, and original receipt," for each item. You can refer to this list when filing an insurance claim.

Review your insurance policy

Though it may be too late to change the terms of your insurance policy, it's a good idea to review your coverage and know what you're owed. Make sure you have your insurer's contact information and the details of your particular plan.

Byrke Sestok, a certified financial planner and co-founder of Rightirement Wealth Partners in New York, recommended asking your insurer to clarify responsibilities -- like boarding up your home and securing loose items -- ahead of the storm.

Related: Tips for filing insurance claims after Harvey

Even if you don't expect to be impacted by a storm imminently, it's a good idea to review your insurance policy and see if you'd like to increase coverage. "A good insurance agent should take the time to go through your policies with you and explain the level of coverage in each area and why it's important to be at that level," said Eagleson. Keep in mind that homeowners insurance typically does not include flood insurance.

Set your bills to autopay

Setting up automatic bill payments before the storm hits means you won't have to worry about missing payments if you're unable to get home or access your bank.

"You do not want late payment fees or service termination if you have no way to get to the post office to mail checks," said Sestok, "or if power is out and you cannot pay online."

Missed or late payments to creditors could lead to fees or affect your credit score down the line.

Set up an emergency fund

Financial experts recommend keeping enough money to cover three to six months' worth of expenses in your savings account. While that's something everyone should aim for, having the money in place and easily accessible could be a lifeline in an emergency situation.

If you expect to evacuate because of a storm you should also hold on to some cash in case banks go offline, ATMs run out of money or electronic payment systems fail. Eagleson recommended keeping about $500 with you -- enough to cover basic needs, but not enough to deal a financial blow if it's lost or stolen.