NEW YORK (CNN/Money) -

Stocks soared Friday, with the major indexes carving out new multimonth highs, as investors looked beyond the week's mixed data in a show of confidence that corporate profits and the economy are heading toward recovery.

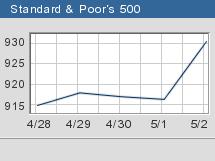

The Nasdaq composite (up 30.32 to 1502.88, Charts), the Dow Jones industrial average (up 128.43 to 8582.68, Charts), and the S&P 500 index (up 13.78 to 930.08, Charts) all closed sharply higher, with the Nasdaq taking the lead.

The Nasdaq closed at its highest point since June of 2002, and has surged 35 percent since hitting its multiyear lows of October 9.

The Dow and the S&P closed the session at their best levels since mid-January.

For the full week, the Nasdaq and the S&P 500 posted gains for the third time in a row, rising 4.7 percent and 3.5 percent, respectively. The Dow recovered from its declines last week, closing up 3.3 percent higher over the last five sessions.

"I love it. This is a market you've got to buy," said Michael Carty, principal at New Millennium Advisors. "You have a record amount of cash sitting on the sidelines wanting to go to work. A lot of the uncertainty facing the market even just six weeks ago has been resolved, such as worries about the cost of rebuilding Iraq and higher energy prices and corporate profits."

Increased interest in the U.S. dollar, particularly versus the yen after weeks of selling, paced the rally Friday, as did a bailing out of low-yielding Treasurys and commodities. Of the 30 issues that make up the Dow industrials, 28 rose.

A worse-than-expected unemployment report in the morning was tempered by the fact that employers cut fewer jobs from their payrolls than had been forecast. A separate report showing strong monthly factory orders added to the mix.

Also bolstering sentiment: the perception that first-quarter profit reports have been better than forecast.

Next week is fairly light on big-name corporate reports, with the exception of Cisco Systems (CSCO: up $0.15 to $15.27, Research, Estimates). The networker is forecast to have earned 14 cents, up from 11 cents a year earlier.

Other companies expected to report include Gillette (G: up $0.35 to $30.40, Research, Estimates), Prudential (PRU: up $0.72 to $32.38, Research, Estimates), EDS (EDS: up $0.67 to $19.04, Research, Estimates), News Corp. (NWS: up $0.36 to $28.68, Research, Estimates), and nVidia (NVDA: up $1.48 to $15.90, Research, Estimates).

On Monday, investors will get the Institute for Supply Management's reading on the services sector of the economy. The April reading is expected to rise to 50 from 47.9 last month and will be looked at closely after the ISM's reading on manufacturing Thursday showed more contraction.

The Federal Open Markets Committee has its rate-setting meeting on Tuesday. Expectations are that the central bank will leave rates unchanged at 1.25 percent.

Airlines rise

Hopes for a recovery in the much-maligned airline sector certainly added to the good cheer Friday, after Merrill Lynch issued a note implying that the worst may be over for the industry and that the bankruptcy threat has diminished for most carriers. Shares of AMR Corp. (AMR: up $0.66 to $5.47, Research, Estimates), the parent of American Airlines, shot up 13 percent and were among the NYSE's most active. Additionally, Merrill Lynch raised its rating from "neutral" to "buy" on Continental (CAL: up $1.94 to $11.80, Research, Estimates) and Delta (DAL: up $1.75 to $14.75, Research, Estimates), among other companies.

In what was perhaps the highlight of the week's economic reports, the Labor Department said the economy lost 48,000 jobs and the unemployment rate climbed to 6 percent in April from 5.8 percent in March. Many on Wall Street had expected bleak news. Although it was bleaker than most had bet on, few were spooked by the numbers. Some found comfort in the fact that the number of jobs lost in April was actually smaller than the expected 53,000 forecast.

Investors found comfort in a better-than-expected March report on factory orders released in the first half hour of trade. The government's report showed that orders for manufactured goods rose 2.2 percent, when economists surveyed by Reuters only expected a rise of 1.2 percent.

In addition, the nearly-completed corporate reporting period has been better than expected with more than 80 percent of the S&P 500 having already released their results; more than two-thirds of them topped estimates.

Companies have been able to generate earnings by not hiring and not buying new equipment, rather than by showing real revenue growth, said John Davidson, president and CEO of PartnersRe Asset Management. But Davidson noted that, largely, investors seem happy with the results.

"I think people are looking beyond the unemployment report and into the future," Davidson said. "The current economic environment is certainly weak, but maybe there's the assumption that it will get better."

The only things going against an extended rally, said New Millennium's Michael Carty, is that a recovery is still just at the very beginning, and traditionally, summer is not a time of big gains.

Techs take off

Strong results from chipmaker and NYSE stock Cypress Semiconductor (CY: up $1.12 to $10.60, Research, Estimates) boosted the stock almost 12 percent and gave a lift to a variety of communication chip makers, which fueled a Nasdaq rise, as did strength in biotech and networking.

Among other heavy hitters, Sun Microsystems (SUNW: Research, Estimates) rallied 12 percent and led the Nasdaq's most active list, boosted also by vague takeover rumors. Intel (INTC: up $0.50 to $19.05, Research, Estimates) and Applied Materials (AMAT: up $0.40 to $15.15, Research, Estimates) both rose 2.7 percent.

Boeing (BA: up $1.51 to $28.62, Research, Estimates) gained nearly 5.5 percent and was among the Dow's best performers after the aircraft maker said its plan to lease 767 commercial jets to the U.S. Air Force as refueling tankers could bring in up to $2.8 billion in support revenue over the life of the proposed lease.

Priceline.com (PCLN: up $0.77 to $3.14, Research, Estimates) shares rallied more than 32 percent and were among the Nasdaq's most active. Late Thursday, the firm reported first-quarter results of breakeven per share, down from a year earlier but better than the one cent per share loss analysts were forecasting, as a result of a stronger hotel business despite the travel slowdown resulting from the war in Iraq and SARS.

The firm also said it would be profitable in the second quarter and that it that it will ask for shareholder approval to conduct a reverse stock split of all outstanding shares.

Market breadth was positive, with more than two stocks rising for every one that fell on the Nasdaq and by more than 3 to 1 on the New York Stock Exchange. Volume was relatively thin, with 1.52 billion shares trading on the NYSE and 1.82 billion shares changing hands on the Nasdaq.

The dollar recovered from recent losses, trading higher versus the yen and edging up against the euro after touching new four-year lows against the European currency earlier in the week.

U.S. Treasury bonds took a step back. The 10-year note lost 22/32 of a point in price, its yield rising to 3.92 percent.

Oil advanced. Light sweet crude futures fell 30 cents to $25.67 a barrel in New York. Gold fell $1.10 to $341.30 an ounce in New York.

European stock markets closed mixed. Stocks in Tokyo rose for the third day in a row.

|