Thumbs up for Netflix service...but not the stock

Netflix is a great company ... but with concerns about competition and users switching to lower priced plans, the stock looks too expensive.

NEW YORK (CNNMoney.com) - Most customers rave about online DVD rental service Netflix. But the stock is getting mixed reviews on Wall Street. It's tough to find another well-known company where analysts' opinions are all over the map. According to Thomson/First Call, nine analysts rate Netflix a "Buy", seven have it a "Hold" and four have even slapped one of those four-letter dirty words -- "Sell" -- on Netflix.

Netflix bulls point to strong revenue and subscriber growth. The company reported last month that it added 687,000 new customers in the first quarter, helping to boost sales by 47 percent from a year ago. Netflix now has 4.9 million subscribers and the company expects that at least 6.3 million people will be receiving its little red envelopes in the mail by the end of this year. But Netflix (Research) bears argue that the company's future looks about as promising as Ben Affleck's film career. The increased availability of video on demand services on major cable systems could hurt Netflix. In addition, more studios are beginning to rent and sell downloads of movies over the Internet. Netflix "hatahs" also point to the stock's sky-high valuation: shares trade at about 54 times 2006 earnings estimates. Competitive concerns may be overdone

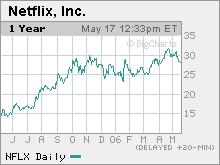

The Netflix bulls still appear to have the upper hand though. The stock has nearly doubled during the past year. But Netflix's stock has cooled a bit lately. Shares have pulled back about 8 percent since last month's earnings report. So what's next for the stock ... a feel-good Hollywood happy ending or a tear-jerker of a decline? It's tough to say. Despite concerns about competition and the stock's rich price tag, many are still confident about Netflix's ability to keep growing its subscriber base. In a recent research note, Cowen & Co. analyst Jim Friedland said that "it will take several years before 'download-ready' mass market consumer electronics are widely adopted," and that he expects "the availability of popular content for digital video subscription platforms to be restricted over the next five-plus years." What's more, it's not as if Netflix is ignoring the potential in video downloads. The company has already said it plans to be a player in this market. And following last month's earnings report, Netflix announced that it was going to sell 3.5 million shares at $30 a share in a secondary offering. Tony Wible, an analyst with Citigroup, wrote in a report that Netflix doesn't necessarily have a pressing need for the $105 million it will raise from the offering since the company already has $228 million in cash and no debt. So he believes that Netflix is probably selling more stock in order to help finance the roll-out of its own video download service. Wible said he's skeptical about how big the online market will actually be, he said that a Netflix download service would probably be cheered by Wall Street. "An online distribution business would qualm investor concerns about Netflix potentially losing market share to download services," Wible wrote, adding that downloads could help Netflix lower fulfillment costs as well as bring on some new subscribers. Great service...expensive stock

Still, investors probably need to be wary. Even people who think the company is doing a fantastic job can't ignore how expensive the stock is. "At this particular valuation, you have to question the coming competition and the fundamental change in the business. Valuation combined with competitive risks make me more neutral on the stock at this price," said Chad Bartley, an analyst with Pacific Crest Securities. Other analysts said that they are concerned about how Netflix has continued to introduce lower price plans, such as its popular $9.99 a month subscription to rent one movie at a time, to keep subscribers. Even though the company has said that gross margins have improved because of this cheaper plan, several analysts worry about the possibility of declining revenue if more and more users switch from pricier plans like the $17.99 month offering that allows subscribers to keep three movies at any given time to the $9.99 plan. "I think Netflix has a phenomenal product. The company is very unique and has dominant market share but I'm worried about the fact they are going downstream with pricing," said Frank Gristina, an analyst with Avondale Partners. "I wonder if they've saturated the $18 a month market." Full disclosure, I'm a happy Netflix subscriber. But I switched last year from the 3 movies a month plan to the $9.99 monthly plan because I simply wasn't watching enough movies to justify the more expensive subscription. And if there are more subscribers like me out there, that could be more problematic for Netflix than emerging competition since it would eventually lead to slower growth in both sales and profits. "For the business Netflix has, they are executing brilliantly. My only knock on the stock is I don't think the business opportunity is as big as others think," said Michael Pachter, an analyst with Wedbush Morgan Securities who has a "Sell" rating on the company. "I don't think these guys are technically obsolete but they are much like a health club. They offer you a valuable service but that they only are valuable if you use it," he added. Finally, it's worth noting that short-sellers, investors who bet that a stock will go down, are also aggressively targeting Netflix. More than a quarter of the company's available shares were being held short as of mid-April. So don't get me wrong. Netflix is a great company that appears to realize what it has to do to stay on top. But given all the concerns facing the company right now, it looks like it's time to press pause on the stock after the heady run of the past year. ----------------- For a look at how the Netflix envelope has evolved over the years, click here. For FORTUNE's coverage of the future of Hollywood, click here.

A member of Cowen's research team has a long position in Netflix's stock but the firm has not done banking for the company. Other analysts quoted in this story do not own shares of Netflix and their firms have not performed investment banking for the company. |

| ||||||||||||||||||||||||||||