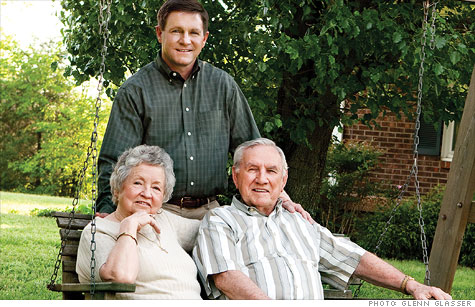

Russ Hendricks has used online banking as a way to help his parents, Helen and Harry, manage their bills.

(Money Magazine) -- Face it. Mom and Dad are getting up there. And their finances aren't getting any simpler. Some of life's trickiest money tasks -- managing a large but basically fixed nest egg, figuring out how to spend it down while never running out -- are in the hands of people who at some point may not be up to doing the work by themselves.

The normal wear and tear of aging can mean worsening eyesight, fatigue, and enormous life changes (such as caring for an ailing spouse) that make it harder to deal with reviewing bank statements or tracking a portfolio.

And as your parents get older, they are also at risk for difficulties with reasoning or memory, which recent studies have found can show up first in their financial skills.

"Neuroscience research suggests people beginning to suffer cognitive impairment make significantly more financial errors than those who aren't," says Robert Roush, associate professor of geriatrics at Baylor College of Medicine. All of this means you have a tough new job to add on top of planning your own retirement and getting the kids through school: helping your parents manage their money.

It's a delicate art. You're used to Mom and Dad being the authority on most things, especially money. So are they. You can't demand out of the blue that they show you their checkbook.

But if your folks are over 70, you and your siblings should start getting them comfortable with the idea that you can help.

"If you don't take action, you can end up paying unnecessary costs or handling things differently from the way your parents would have wanted," says Andrew Lo, a professor at the Massachusetts Institute of Technology. Lo is well-known on Wall Street as a leading expert on number-crunching hedge fund strategies, but he still had to negotiate with his own mother to help with her money. He's been urging financial advisers to be more aware of aging problems.

This story is the first in a three-part series on protecting your parents. It will show you what researchers are learning about how seniors handle finances, and identify some simple things you can do starting even before your parents have serious problems. The goal is to help them without taking over their lives.

You'll find a guide to gadgets and services that will help your folks stay independent for as long as possible.

Finally, a feature in the August issue will help you defend Mom and Dad against the people hawking inappropriate -- or worse -- financial products.

To get started, it helps to know more about how your parents' lives have been changing as they age. That can help you decide when and how you should step in.

WHAT TO WATCH OUT FOR

Old age brings enormous changes -- not all of them physical -- that could leave your parents feeling overwhelmed by the work of running their money.

In many marriages -- especially in your parents' generation -- husbands and wives split up financial duties. When one of your parents dies or becomes seriously ill, the other will very likely be handling unfamiliar problems, whether it's picking mutual funds or making sure the utility and cable bills are sent out on time. Anyone in that situation, young or old, could benefit from extra help or advice.

Even normal aging can bring gradual changes in mental function. Those changes may not affect the ability to make sound financial decisions, but if Dad takes longer to work with numbers than he used to, he may become less diligent about checking his account statements.

General health issues can also make things harder.

Russ Hendricks of Watertown, Tenn., helps his mom, Helen, 77, manage the bill paying. She's been spending a lot of time caring for his dad, Harry, 81, who has trouble walking. And she recently had back surgery.

"I find time gets away from me really fast these days," says Helen. "With my surgery, I'm still having to rest in between chores."

Russ noticed a problem when Helen said she had trouble balancing the checkbook. "My mom isn't forgetting things, but she gets overwhelmed," he says.

Other possible red flags: increased complaints about having to fill out forms from an insurer or brokerage, trouble reading fine print, or a general rise in stress about paying bills.

About half of people in their eighties suffer from significant cognitive impairment. That includes Alzheimer's but also other issues. This mental deterioration often takes families by surprise.

"Older people may be able to answer questions and respond well in social situations, but people end up shocked when they finally look at their finances," says Beth Kallmyer of the Alzheimer's Association.

So what should you be on the lookout for? A recent paper in the Journal of the American Medical Association lists warning signs. Your parent might have forgotten to pay utility bills or rent, or could be having trouble making change or writing checks.

Or they may complain that money is missing from their bank account or that someone is stealing from them. Of course, your parents may never get to that point -- and it's best to start the process of helping well before they do.

WHAT TO DO WHEN THEY SIMPLY NEED A HAND

Get involved in small ways while your parents are still healthy. You can let them know you are available for advice, and make routine tasks easier for them. All of this will make it easier to step in when bigger issues arise later.

It won't be easy to get your parents to open up about their finances.

"For many older Americans, who grew up during the Depression and World War II, money has always been a taboo subject," says Miriam Zucker, a geriatric-care manager and social worker in New Rochelle, N.Y.

So don't expect to have one big talk that settles it all. Get the conversation rolling by asking how they've prepared their financial accounts in case of an emergency. Where do they keep their accounts and insurance? Where would you find the paperwork? Who has the passwords?

Those shouldn't be touchy questions -- you aren't asking them if they are having trouble remembering the bills, just whether they've made the contingency plans everyone (you included) ought to have.

They may also have an easier time talking if you keep them in their familiar parental role, says Zucker.

Ask Dad for advice on how best to invest the money you put in his granddaughter's college savings account. Or tell Mom you are revising your will and you're wondering how they'd handle it.

You could very well get good advice, and conversation will flow naturally from there. And by talking about your investments and estate, you've also basically told them that you are doing okay financially. That will make it easier for them to turn to you.

Another way to reassure them they are still the parents is to say you've been worried and they could make you feel better if you knew more about their plans.

"You're asking them to do you a favor," says Jake Harwood, an expert on communication and aging at the University of Arizona.

Try citing something called the 40/70 rule, suggests Paul Hogan, head of a senior-care agency called Home Instead. The idea is that families should talk money when the parents turn 70 or the kids turn 40.

Russ Hendricks says online banking has been an important tool for helping to manage his parents' finances.

"I said, 'Mom, I use electronic banking, and it makes my life so much easier. Let me help you do this,' " he says.

Russ adds that there was an important side benefit for her: "She asked me to help her learn to use a laptop so that she can learn about the Internet and stay more connected."

Working with your parents to set up their accounts will also give you a glimpse at the state of their finances.

Financial advisers and planners can be a huge help, in part because having a neutral third party can defuse family tensions. But don't count on this person to sound the alarm if your parents are having trouble.

A survey of advisers by Fidelity found that 84% had worked with clients they suspected were suffering from Alzheimer's, but just half felt comfortable raising the subject.

Ask your parents if you can come along next time they meet their adviser. Watch to see if Mom and Dad are following along with the conversation. And just as important, check that they aren't being taken advantage of.

You should be concerned if the adviser is frequently pushing new financial products, especially if there are upfront loads and commissions attached. And make sure your parents aren't taking on too much risk.

Even an aggressive rule of thumb says that a stock position should equal 110 minus your age. So if your 75-year-old mom is over 35% in stocks, at least ask questions.

WHEN IT'S TIME TO HELP THEM MAKE DECISIONS

If you haven't already discussed the issues with your siblings, now's the time to make sure they know what's going on -- perhaps they can even share the burden.

That strategy has worked well for Diane Huff of Charlotte, N.C.

She manages the day-to-day finances of her mother, Ollie, who lives in an assisted-living center nearby. Meanwhile, her brother, Jim, in Florida, manages Ollie's investment portfolio.

"I just told Jim I can't do it all," says Diane.

Even if it's not necessary for everyone to pitch in, keep your siblings informed about what's going on -- you don't want to risk misunderstandings or bad feelings.

Taking a more active role in your mom and dad's finances may make them nervous or even resentful. Or they may simply need time to build trust in your abilities, as well as accept the idea of letting some responsibilities go.

So try to keep your involvement low-key -- perhaps using it as an opportunity to socialize. Offer to have a bill-paying and savings review date once or twice a month. After you square away the bills, go out for coffee or a meal.

"That makes the process more like an excuse to get together and have some fun," says Jim Ludwick, a financial planner in Odenton, Md.

With increased forgetfulness, your mom and dad may be at greater risk of making a major money misstep. They may also be targets for scams. So put some tripwires in place that will alert you if there are problems.

Ask your parent to have you listed to receive automatic notification if he or she misses a utility payment. And consider getting them to give you access to their bank accounts. Then you'll be able to see their daily cash-flow information.

One caveat: Check with the bank about what kind of account your parent has. Be sure you or your siblings are sharing a so-called convenience account, not becoming a joint owner with right of survivorship.

That might run afoul of your parents' estate plan, since you would inherit any leftover assets. It could also put your parents on the hook for the debts of anyone listed on the account, says Patricia Sitchler, an elder-law attorney in San Antonio.

In other words, if your brother is a joint owner and can't pay his credit card balance, creditors could have a claim on the money in Mom's account.

As you become more and more involved in helping Mom and Dad out, you can all too easily forget to treat them as the adults they are. Whether they've moved into your house or you've taken over management of their household budget, it's important to give them as much financial independence as they can handle.

Staying involved and active is essential to older people's well-being, says Laura Carstensen, director of the Stanford Center on Longevity.

That means getting out and socializing with friends, which can be difficult for them to do if they don't have control over some money. Even if you and your siblings eventually have to manage most of their finances, make sure your parents have access to cash and perhaps credit cards, with modest limits, for as long as possible.

Marion Peterson, 80, of Downers Grove, Ill., has moved in with her daughter, Gail Dunlap, and her family. That means she doesn't worry about paying for a lot of basic costs, such as utilities. But she still has her own bank account, and pays her own credit card, Medicare, and insurance bills. If she has questions, she can turn to Gail.

"I forget sometimes, and it helps to have someone else look at things with me," says Marion. That balance of support and freedom can help your parents live a better life -- one without money worries.

ADDITIONAL REPORTING BY Walecia Konrad and Beth Braverman. ![]()

| Overnight Avg Rate | Latest | Change | Last Week |

|---|---|---|---|

| 30 yr fixed | 3.80% | 3.88% | |

| 15 yr fixed | 3.20% | 3.23% | |

| 5/1 ARM | 3.84% | 3.88% | |

| 30 yr refi | 3.82% | 3.93% | |

| 15 yr refi | 3.20% | 3.23% |

Today's featured rates: