Millions of Americans aren't saving enough for retirement, prompting Congress and even the President to propose ways to help workers save. But can the government really help us save more?

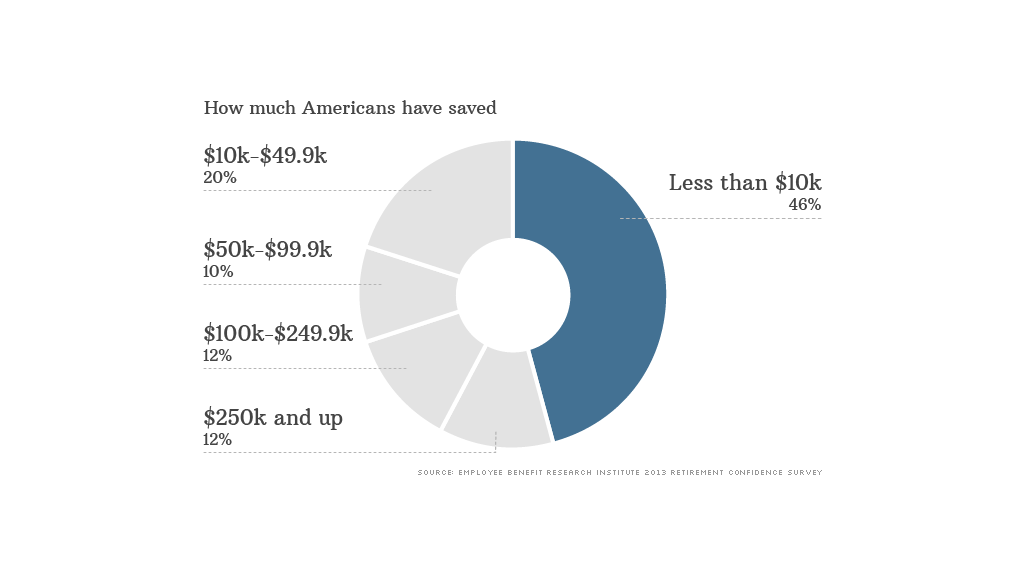

Last year, 46% of workers had less than $10,000 saved for retirement, according to a 2013 report from the Employee Benefit Research Institute. Meanwhile, around half of all workers and the majority of part-time workers didn't receive any retirement benefits at all from their employer, making it even more difficult for them to save.

President Obama's recently announced myRA plan may be a good start, but retirement savings advocates say it's far from a solution. Any meaningful change -- one that would get the millions of workers who aren't currently saving to automatically put away money through their employers and those who are saving to put away more -- would require Congressional approval, which has proven to be a major hurdle.

The President and other legislators have proposed plans that go much further than the myRA plan, including the creation of so-called "automatic IRA" accounts, but these plans will do little to boost the savings of workers who already have retirement plans.

Related: What you need to know about Obama's myRA retirement accounts

The recently created "myRA" accounts allow savers to invest up to $5,500 a year in government savings bonds, earning a return of around 2% to 3%, until their balance reaches $15,000. At that point, the account can be rolled over to a private sector Roth IRA, where the money can continue to grow tax-free.

While the accounts are seen as an important first step to getting non-savers in the practice of saving, some critics argue that the tax-free withdrawals allow them to raid their accounts before reaching retirement and that the modest returns won't stand up to inflation.

Either way, the accounts likely won't make much of a difference because workers won't be automatically enrolled, said Alicia Munnell, director of Boston College's Center for Retirement Research. "We've learned that nothing really works if you don't have automatic enrollment," she said.

But anything that requires employers to automatically enroll workers will require Congressional approval, she said. In the past, legislation that included auto enrollment for all workers has struggled to gain much traction.

Related: What Americans think about Obama's myRA retirement accounts

In 2006 lawmakers passed the Pension Protection Act, which included incentives for employers who offered 401(k) plans to begin automatically enrolling their workers in the plans. Proponents say the change has boosted workplace savings rates, but it did little to help those who worked at companies that didn't offer 401(k) plans.

Democractic Sen. Tom Harkin from Iowa this month proposed legislation that would mandate employers with more than 10 workers that don't offer retirement plans to automatically enroll them in a so-called "USA Retirement Fund" that would be overseen by the Department of Labor.

The privately-run funds would operate like pensions, both through the pooling of investments and lifetime retirement benefits, which would be based on a worker's total contributions and investment performance over time.

The proposal has received praise from unions and retirement advocacy groups, who say it could be a "significant leap forward." But the bill has concerning aspects, including its lack of investment choices for participants, according to the Investment Company Institute, an industry association.

Harkin's plan would also require significant changes for employers, including those who already offer 401(k) plans, making it a tough sell to many legislators, said Nevin Adams, EBRI's director of education and external relations.

There is one more possibility that is being floated around. In his State of the Union address, President Obama separately touted an automatic IRA proposal, which has been at the heart of past legislation that has failed to get past Congress.

The idea works like this: Businesses with more than 10 employees that do not offer a retirement plan would have to automatically deduct part of their workers' pay to be invested in an IRA with a set of investment options -- unless the employee opts out.

Related: Will you have enough to retire?

Employers would incur minimal costs, supporters say. They would not be required to provide matching contributions or be liable for the investments' performance. In 2011, a report by the nonprofit Urban Institute said that the auto IRA proposal was "one of the most promising ways" to help low and moderate-wage workers save.

The proposal would likely result in millions of additional retirement savers, said William Gale, director of the Retirement Security Project at the Brookings Institution, which jointly developed the automatic IRA proposal with the Heritage Foundation. Plus the accounts could provide higher investment returns than the myRA plan by allowing savers to invest in age-based investments, including stocks.

The idea continues to receive bipartisan support and legislation will likely be introduced again this year, Gale said. Past legislation has repeatedly failed to make it to a vote, but Gale said he is hopeful future attempts can gain more steam, amid the buzz surrounding Obama's myRA plan.

"I remain optimistic about its political prospects," he said. "It's not going to solve the whole problem, but it is an even bigger step than the myRA."