NEW YORK (CNN/Money) -

A growing number of observers have come to believe that the best thing the Federal Reserve could do to ensure economic recovery is offer up a little more clarity on what, exactly, might prompt it to start raising rates again.

At this point it seems unlikely they're going to get their wish.

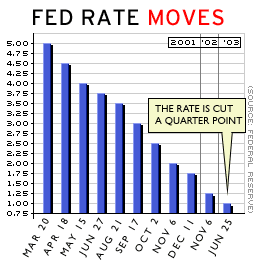

Economists and investors are all in agreement over what the Fed will do with rates when it meets Tuesday -- nothing -- but when it comes to what's going to happen later this year and next, confusion reigns. A few economists expect the Fed to drop its overnight funds rate a quarter point by the end of the year, some expect it to raise rates in mid or late 2004, others expect it to hold at the current 1 percent until 2005.

To judge from market prices, investors appear to expect much more aggressive action. Both fed funds and eurodollar futures contracts, which price off of Fed easing expectations, say the Fed will have raised rates by a quarter point by next spring and half a point by next summer.

As America's favorite defendant in a high-profile case might say, this is not a good thing -- particularly since the Fed feels (or at least has said it feels) that the risk of inflation dropping to unacceptably low levels is greater than the risk of inflation jumping higher for "the foreseeable future."

Inflation of the nation doesn't bother me

Unfortunately, complains Pimco managing director Paul McCulley, "the foreseeable future" seems rather amorphous. Does that mean until next month, next quarter, next year? What McCulley and others would like to see is for the Fed to clearly define what sorts of conditions would prompt it to raise rates.

"The essence of the problem is that the war against inflation is over," said McCulley. "Ever since 1979 the Fed was fighting a war against inflation, and you always knew which way you wanted the inflation rate to go over the long run -- down."

But now inflation is no longer the problem that it was in the past, and, as the Fed itself has indicated, the potential for inflation to drop too low has also become a risk for the economy.

McCulley has likened it to what would happen if 400-pound former Chicago Bears lineman William "The Refrigerator" Perry went on a diet. For a long time, the Fridge wouldn't have to worry about what his ideal weight was.

"But there does have to be a point," said McCulley, "where the doctor says, 'Fridge, you gotta go back to eating.'"

The economy's ideal weight is "price stability" -- a rate of inflation which is neither too high nor too low. Where that is, exactly, is the subject of plenty of debate, but what people really want to know now is where the Fed thinks it is.

"The Fed truly wants to get inflation somewhat higher -- back into the comfort zone," said Morgan Stanley chief U.S. economist Richard Berner. "Why not say where that comfort zone is?"

In doing so, thinks Berner, the Fed would shore up much of the worry that has washed up into the Treasury market recently. Since hitting a 45-year low of 3.11 percent on June 13, the yield on the 10-year Treasury has backed up more than a full percentage point. Higher Treasury yields have fed through to both mortgages and corporate bonds, limiting the ability of both households and businesses to raise capital.

Berner thinks that the economy will be able to withstand the headwinds higher rates have created, but he also believes they'll limit growth, making the economy more vulnerable to shock.

But cry as they may, the Fed's critics acknowledge the central bank is unlikely to change its ways. The problem with adopting specific guidelines for price stability or, taking it a step further, coming up with an inflation target, is that it would take away some of the Fed's policymaking flexibility. And the Fed, particularly under the stewardship of Alan Greenspan, has always fought to maintain its flexibility.

"The problem with retaining your flexibility is you also create uncertainty," said Goldman Sachs chief U.S. economist Bill Dudley. "I'd be very pleased if the Fed took some new initiatives, but I'm not expecting it."

|