|

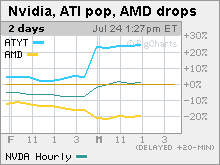

AMD-ATI deal boosts shares of Nvidia Speculation about a possible partnership between Nvidia and Intel has driven the shares up nearly 10%. NEW YORK (CNNMoney.com) -- Regardless of what the market makes of the impending nuptials of PC chipmaker Advanced Micro Devices and graphics chip maker ATI Technologies, one clear winner in the match-up appears to be Nvidia, at least as far as traders are concerned. Shares of Nvidia (up $1.66 to $19.43, Charts), one of the largest makers of graphics chips for computers and other consumer electronics - and the number one competitor to ATI (up $3.00 to $19.56, Charts) - were up nearly 10 percent in mid-day trading. AMD (down $0.90 to $17.36, Charts) said today that it will spend $5.4 billion to acquire ATI in a cash and stock deal that is expected to close in the fourth quarter.

Analysts and investors say that the spike in Nvidia's shares could be attributed in part to speculation that Nvidia is in talks with Intel (up $0.28 to $17.43, Charts), the number one maker of chips for PCs, to supply graphics chips to the company. But people in the business are divided on whether today's news means that Nvidia and Intel will reach an agreement, or whether such a partnership would take the shape of an out-and-out acquisition. And still others are not convinced that today's news is beneficial to Nvidia at all. N-convenient side effect David Wu, an analyst at Global Crown Capital, said the news of ATI's sale to AMD could be bad news for Nvidia in the short term. That's because Nvidia has done brisk business selling chipsets, or the pairs of chips that surround microprocessors, to AMD, particularly for AMD's popular Opteron server chips. Those ties may have to be severed in light of the deal, according to Wu. "AMD has been very good to Nvidia and Nvidia has been very good to AMD," Wu said. "If you were to look at Nvidia's chip set business, it's 20 percent of total revenues, and 90 percent of that is for the AMD platform. They built a very successful premium brand image on the AMD side of the business and very little on Intel." Eric Ross, an analyst with ThinkEquity Partners, agrees that today's news is bad for Nvidia because of its ties to AMD. "They've seen their biggest growth in revenues specifically because of the partnership with AMD and that just goes away (with the sale)," said Ross. Ross also believes Intel will have to come up with its own strategy for making high-end graphics processors. Intel currently makes graphic processors, but these are designed for low-end machines, unlike the souped-up processors that Nvidia and ATI make for demanding, graphics-heavy applications such as gaming. But he's not convinced that buying Nvidia is on Intel's mind. "It's possible, but it's less likely than you'd think," said Ross. That's in part because of Intel's well-documented problems of losing market share and slowing growth, which have caused the chip maker to put up several consecutive quarters of weak performance. That led to a broad restructuring at the company, which is still taking place. Analysts agree that while today's news means Intel will likely need to come up with its own approach to high end graphics processors, buying Nvidia outright is not necessarily the answer. "Intel will not change course and buy Nvidia," said Hans Mosesmann, senior vice president and semiconductor analyst at Moors & Cabot. "They're on a mission to reduce cost, become more focused, and get in tune with their core competencies." Nvidia + Intel? Maybe, maybe not But unlike Ross, Mosesmann does not believe AMD's plans to buy ATI necessarily spells bad news for Nvidia. Mosesmann estimates that chipset sales account for roughly 15 to 16 percent of Nvidia's total sales, and that about half of those chipsets are going to AMD's Opteron server chips. Mosesmann acknowledges that estimates of the percentage of Nvidia's total sales that come from chipsets vary, and that some analysts think the number is a bit higher than he does. "ATI doesn't do chipsets for servers, so that business is not going away," said Mosesmann. "The chipset business that could be lost is maybe in the mid- to high-single digits [of Nvidia's revenues] at best." Jane Snorek, senior research analyst with FAF Advisors, is among those convinced that Intel would not buy Nvidia, in part because she thinks the shareholder backlash would be severe. "If Intel bought Nvidia, I think that would be the end of (Intel president and CEO Paul) Otellini," said Snorek, whose firm does not own any chip stocks in the funds she advises. "AMD paid a 25 percent premium on ATI and they missed their numbers, and the stock's been hammered. There's no way [Intel] could afford" to take that risk, she said. But she does believe Nvidia may well strike a deal with Intel, and one that could benefit both companies in the long run. "If Nvidia feels threatened by this AMD/ATI partnership, it could form a partnership with Intel, which could really use a reliable partner on the high end of graphics chips," said Snorek. Kevin Landis, chief investment officer of Firsthand Funds, which runs mutual funds specializing in tech stocks, agreed that a partnership between Intel and Nvidia in which the latter supplied high-end chips to the former could make sense. But he's not so sure that Intel buying Nvidia is necessarily out of the question. "The issue with Intel is not on the balance sheet, it's on the income statement," said Landis, whose funds own small positions in Intel and AMD but not in Nvidia or ATI. "It's lack of growth, issues with profit margins, and competitiveness. The balance sheet is so darn strong, most shareholders would say whatever you need to do to get growing again, do it." Landis noted that with Nvidia currently sporting a market cap of roughly $7 billion, the purchase would be less costly for Intel, with a market cap of roughly $101 billion, than it was for AMD to buy ATI. AMD's market cap is about $8.5 billion, while ATI's is about $5 billion. "Intel has disappointed people with lack of growth or not always having a best of breed product," he said. "But say what you will, they continue to make a lot of money, and they could spend quite a bit more on Nvidia then AMD spent on ATI and they wouldn't feel it nearly as much." Ross of ThinkEquity Partners does not own shares of AMD, ATI, Intel or Nvidia but his firm makes a market in shares of Intel and Nvidia. Mosesmann of Moor's and Cabot does not own shares of the companies he mentioned, and his firm does not have banking ties to the companies. Wu owns shares of ATI and Intel, but his firm does not have banking ties to the company. Related: AMD to buy ATI for $5.4 billion |

|