|

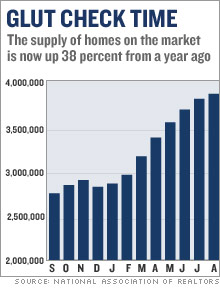

Home prices: 1st drop in 11 years Sales slow, prices hit by second biggest year-over-year drop on record; surge of homes for sale seen keeping prices weak. NEW YORK (CNNMoney.com) -- Home sales slowed and a key measure of prices fell for the first time in 11 years last month, spurred by the biggest glut of new homes on the market in more than a decade, an industry group said Monday. The National Association of Realtors report on existing home sales showed that the median home price in August was $225,000, down 1.7 percent from a year earlier.

It was the first year-over-year decline in median prices since April 1995, when that measure slipped only 0.1 percent. And it was the biggest year-over-year drop since the record 2.1 percent decline recorded in November 1990, when the nation was in recession. While month-over-month declines in prices are not uncommon, year-over-year decreases in prices are a more serious sign of a slumping housing market. Even in other recessions, home prices generally have risen year-over-year on a national basis. The median price is the point at which half the homes sell for more and half sell for less. The decline in home prices follows a period of record sales and very strong sales gains up through the end of 2005. The average price of a home in 2004 was up 9.3 percent from the previous year, and last year the full-year price average was up 12.4 percent. The downward pressure on prices came from the record inventory of homes on the market in August. The group said there were 3.9 million homes on the market, up 38 percent from a year earlier. That gave the market a 7.5-month supply of homes, also up sharply from the 4.7-month supply available in August 2005, and the average 4.3-month supply throughout 2004. The last time the group estimated a 7.5 month supply was April 1993. The report also showed the pace of sales essentially leveling off, slipping to an annual pace of 6.30 million in August from a revised July reading of a 6.33 million rate. While that's down just a bit from July, the pace of sales is down 12.6 percent from a year earlier. Economists surveyed by Briefing.com had forecast that sales would slow to a 6.20 million pace in August. The group's report also showed the average price, which is typically higher than the median price, slipped 1.5 percent from a year ago to $271,000 in August. David Lereah, the trade group's chief economist, said the relatively small drop in sales in August suggested that housing has cooled to a more sustainable pace, although he conceded the weakness in prices is likely to continue. "We do expect an adjustment in home prices to last several months as we work through a buildup in the inventory of homes on the market," he said in the group's statement. Mortgage rates have come down in recent weeks, with the average 30-year fixed rate mortgage now at 6.4 percent, according to mortgage financing firm Freddie Mac (Charts). That's down from 6.79 percent in early July. The drop in rates, which reduces the cost of home ownership, won't necessarily show up in existing home sales figures for several months, though. But some in the industry say lower mortgage rates won't be enough to revive the sales market, which hit its ninth record in 10 years in 2005. Sellers also will have to start reducing prices to get sales back on track. "In some areas home sellers are not making sufficient adjustments in their listing price, so their homes are staying on the market and contributing to the buildup in inventory," said Thomas Stevens, a realtor in Vienna, Va., and the president of the trade group. Existing home sales is not the only portion of the real estate market to show weakness. New home sales and prices for new homes have fallen sharply as well, with many of the nation's leading builders, including KB Home (Charts), Lennar (Charts), Toll Brothers (Charts) and Hovnanian (Charts), lowering guidance on home sales in recent weeks, reporting lower prices and excess supply of homes on the markets. The government report on new home sales in August is due Wednesday. While that's a fraction of the overall market, the new home sales report is closely watched as a leading indicator of the market since it's based on sales when contracts are signed, not on closings, which are often months later. More home markets 'extremely' overvalued |

|