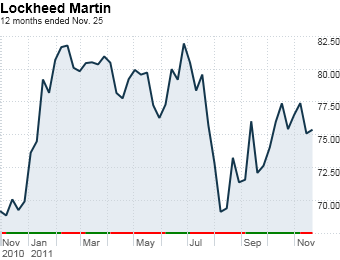

We all know the bad news for defense contractors: Planned military pullouts from Iraq and Afghanistan, compounded by the failure of the congressional Super Committee, which could trigger hundreds of billions in defense cuts over the next decade. No surprise that Lockheed Martin trades at a depressed 9.9 P/E. But the military has allies, and deep cuts seem unlikely in an election year. Even if they occur, spending would shrink only to 2007 levels, and "war" spending, which comes from a separate budget, would be immune.

For Lockheed, the impact would be tempered by a $73 billion order backlog. Analysts expect 2% earnings growth in 2012 and 10% in 2013. Investors are "losing sight of how durable the business is and the fact that you're getting the majority of the cash flow returned to you," says Katrina Mead, a manager of the MFS Value and Large Cap Value funds. Lockheed is on pace to return more than 90% of its $4.2 billion in 2011 cash flow as dividends or share buybacks. The yield is 5.1%, and Lockheed hasn't cut its dividend in 12 years. So even if the stock goes nowhere, you'll receive a handsome reward.

Markets up. Markets down. Turmoil in Europe. You can't even trust bonds. What's an investor to do? Our man's solution: simple and boring.