Denise Townley was "incensed" when her her mother's credit card company contacted her only 13 days after her mom passed away.

NEW YORK (CNNMoney) -- Nobody wants to remember a deceased family member by the debt they left behind, but many creditors certainly make it difficult to forget.

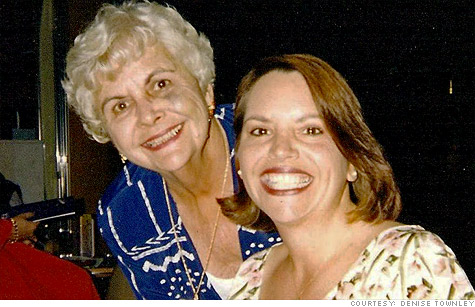

Denise Townley was appalled when she received a letter from her mother's credit card issuer less than two weeks after her mother passed away.

"We have recently learned that [your mother], a valued Discover Card customer, has passed away. Please accept our sincere apologies," stated the letter from Discover, which Townley sent to CNNMoney.

It then offered her or another family member the "opportunity" to assume the balance on her mother's credit card and offered a special introductory APR of 0% for the first six months (the APR would increase to 13.24% after that). If Townley wasn't interested in taking over the account, then the bank wished to discuss how the estate planned to pay off her mother's credit card balance.

Confused and concerned that she was on the hook for her mother's debt, Townley called Discover. When she asked a probate specialist there how they knew her mother had passed away, she was told that Social Security furnished the information.

"I find this not only ethically abhorrent, but also irresponsible and insensitive on both parties' parts," said Townley.

But while it may be "ethically abhorrent," it's not illegal. Banks are within their rights to seek payment for debts owed by a deceased borrower, and the estate is liable for the debt if it has enough money.

"We understand that settling the affairs of loved ones is difficult," a Discover spokesman said. When contacting family members about the unpaid debts of deceased card members, Discover states upfront that payments on behalf of a deceased relative are voluntary, not required, he added.

Financial institutions typically receive notice of a person's passing from the Social Security Administration within a month or two, according to a recent review of the agency conducted by the Social Security Administration's Office of the Inspector General. Yet, in some cases, banks find out even earlier than that.

Because it's likely the deceased carried multiple debts, creditors often race to be the first to collect money from the next of kin or the estate before it has all dried up, said Gerri Detweiler, a debt specialist at credit card research and comparison site Credit.com.

"The longer a creditor waits to get paid, the less their chance of getting paid," she said. "And unfortunately, they may find that it's easiest to elicit payment when bereaved relatives are still trying to sort everything out."

During her husband's wake, Deborah Crabtree said she had set up an answering machine and put it on speaker phone so that loved ones could leave their condolences, according to the complaint she filed against Bank of America.

But instead of hearing only the voices of friends and family come through the speakers, she said a debt collector from Bank of America Home Loan Servicing called every 15 minutes and left harassing messages about the debts her husband had left behind that everyone in the house could hear.

Even after the wake, Crabtree said Bank of America collectors called her as many as 48 times a day -- and even threatened to foreclose on her home, according to a lawsuit she filed last month against the bank.

Crabtree, who lives in Honolulu, said she had told the bank that she would pay the debt as soon as she received her husband's life insurance check. However, the agents told her that since the calls were computer-generated they couldn't stop them until the debt was paid.

Crabtree's lawsuit claims that Bank of America violated state debt collection laws. Her lawyer, Gary Shigemura, said the bank has not yet responded in court.

For its part, Bank of America declined to comment on the particular case, but a spokeswoman said that in general, the bank informs family members when they aren't responsible for the debt of a deceased relative.

The Federal Trade Commission recently declined to impose a "cooling off" period after a death, during which creditors wouldn't be allowed to go after a debt.

The FTC said it was unnecessary, since its rules under the Fair Debt Collection Practices Act already prohibit third-party debt collectors from collecting debts at "inconvenient times" and harassing customers.

Yet, the FTC only governs third-party debt collectors, not the banks -- which are regulated by individual states. And while many of the states have laws similar to the FTC's, the terms "harassment" and "inconvenient times" can be interpreted very differently by consumers and creditors, said Detweiler.

Often mourners don't have enough time to grieve their loss, let alone assess the debts owed by the deceased -- and whether or not they're on the hook to pay for it.

Some debt collectors make family members feel responsible for debt owed by the deceased by asking them questions about whether they were the one who paid for the funeral or took care of other business related to the person's death, said Detweiler.

"They don't necessarily state that you are liable for the debt, but they blur the lines to make you feel like somehow you are responsible for it, even if it's just a moral responsibility," she said.

Most people won't have to pay for their deceased family member's debts unless they co-signed on the loan or it is a debt from a joint account. However, those who live in community property states, where property and assets acquired during a marriage are considered jointly owned, are liable for the debt, said Detweiler.

"If you don't think there's a reason you should be legally liable, you'll need to look at money in the estate -- but don't start payments until you figure out whether there's enough money in there to pay it," she said.

As the executor of the estate, you can request the credit card balance of the deceased's account. Under a provision of the new CARD Act, the issuer has 30 days to provide the balances and can't charge any penalty fees or interest if you or the estate pays off the balance within 30 days after it provides that information.

If the estate doesn't have enough money in it to pay the debt, the creditor is often out of luck. ![]()

Carlos Rodriguez is trying to rid himself of $15,000 in credit card debt, while paying his mortgage and saving for his son's college education.

Susan Carson and Laura DeLallo make $225,000 and have half a million in retirement savings, but their sprawling portfolios is proving hard to manage.

| Overnight Avg Rate | Latest | Change | Last Week |

|---|---|---|---|

| 30 yr fixed | 3.80% | 3.88% | |

| 15 yr fixed | 3.20% | 3.23% | |

| 5/1 ARM | 3.84% | 3.88% | |

| 30 yr refi | 3.82% | 3.93% | |

| 15 yr refi | 3.20% | 3.23% |

Today's featured rates: